Period: 13 – 19 March 2021

Top news story: I do not know whether it is economic news that the President of the United States is playing along in response to the clearly provocative question of whether or not Putin is murderer. However, one comment of this is definitely a significant economic event:

«The Biden statement on Putin is inadmissible to a head of State. It is not a statement to be assented and swallowed» — Turkish President Recep Tayyip Erdoğan said.

But Putin’s answer he called excellent. According to the head of the Turkish state, the Russian leader «did all the necessary».

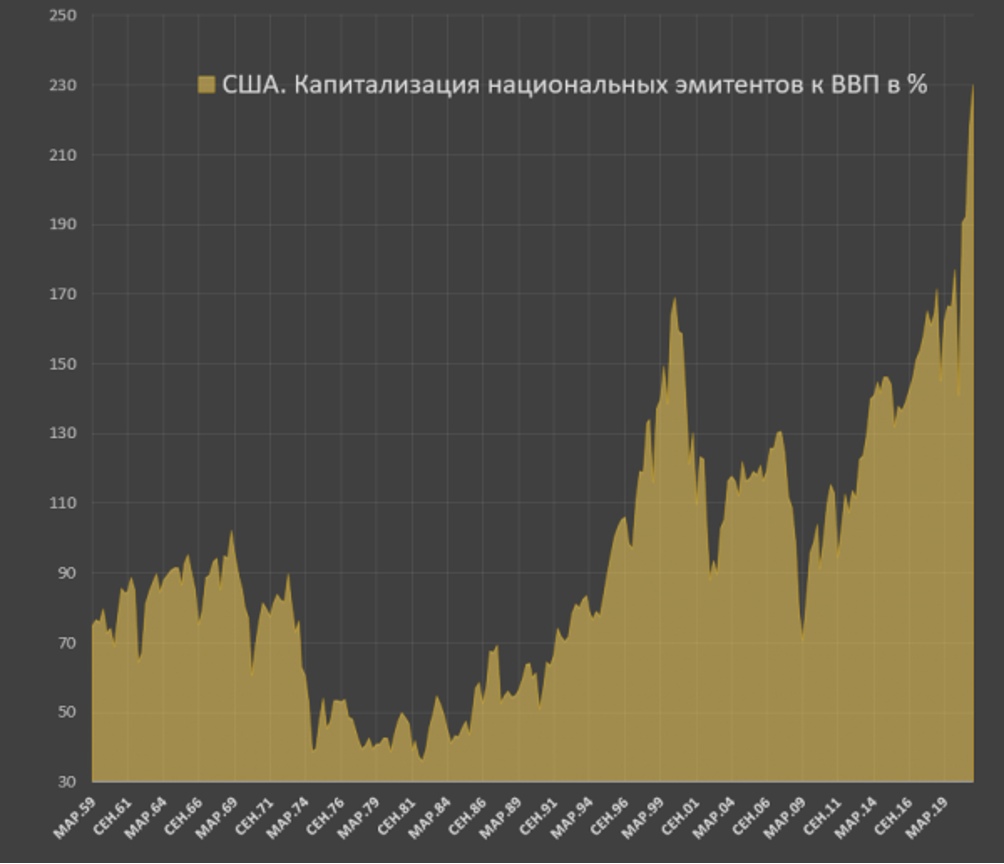

Why do I think this comment is economic? And why the main event of the week? The reason is that the emission simulation of an economy, according to IMF leaders, is becoming a normal practice from something out of the ordinary. And has already achieved outstanding results (source – spydell.livejournal.com):

Let us remind that in the book «Sunset Dollar Empire and the end of the «Pax Americana», published by A. Kobyakov and M. Khazin in 2003, detailed how such policies inevitably lead to a structural crisis, which, in turn, leads to the collapse of the world dollar (Bretton Woods) system. And the big question here is which countries are going into which currency zones.

The results of the research of M. Khazin (which are also described in the above-mentioned book) suggest that Turkey should enter the Eurasian – ruble – currency zone. But economic expediency is one thing, and reality is another. Erdoğan’s talk clearly shows that he is taking this scenario very seriously, and Putin’s position appeals to him much more than Biden’s. And in the face of rapidly increasing instability in global financial markets, such statements carry much weight, as they clearly point to the direction in which the situation will evolve.

Macroeconomics

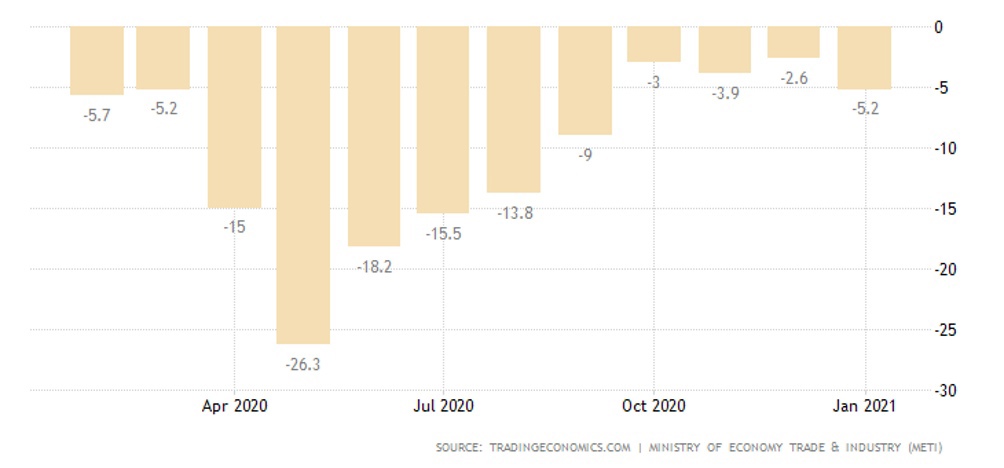

The decline in Japanese industrial output in January accelerated to a four-month peak of -5,2% per year:

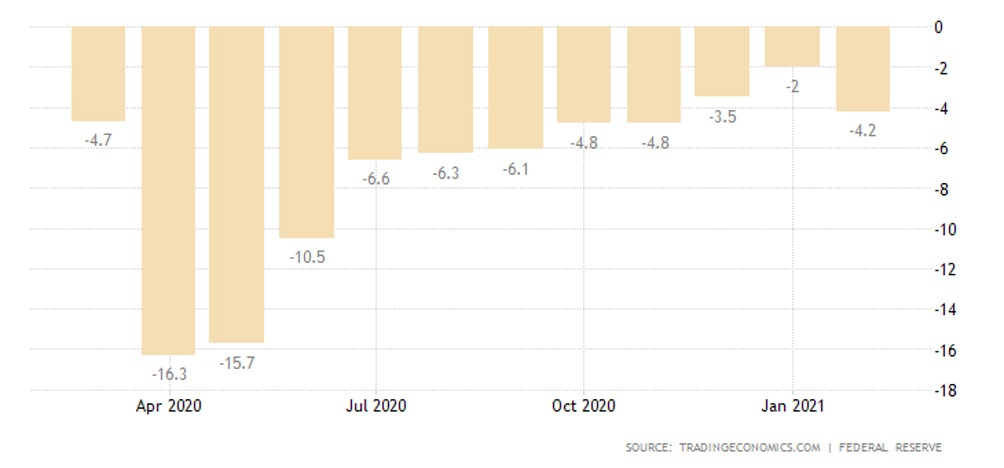

The US is also down: – 2,2% per month (lowest since April 2020) and -4,2% per year – 18th consecutive loss, i.e. the decline started six months before the pandemic:

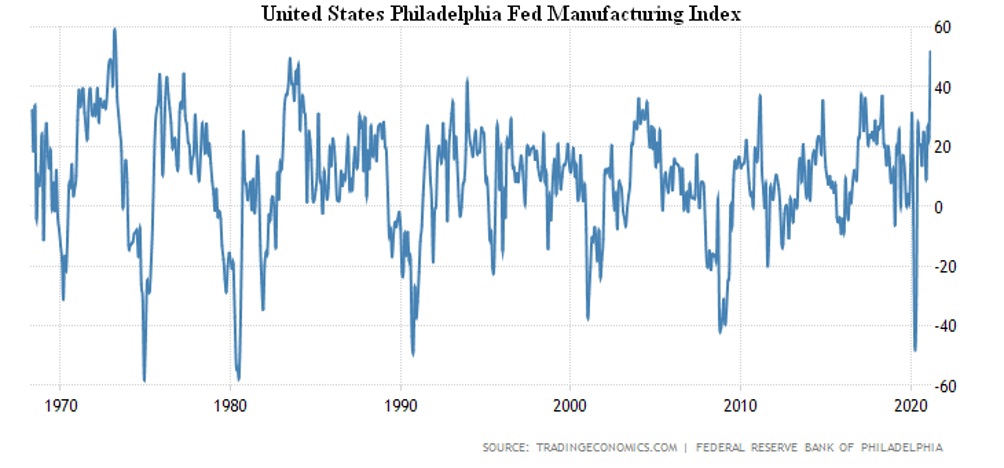

However, the Philadelphia Fed Manufacturing Index showed a peak growth of almost half a century:

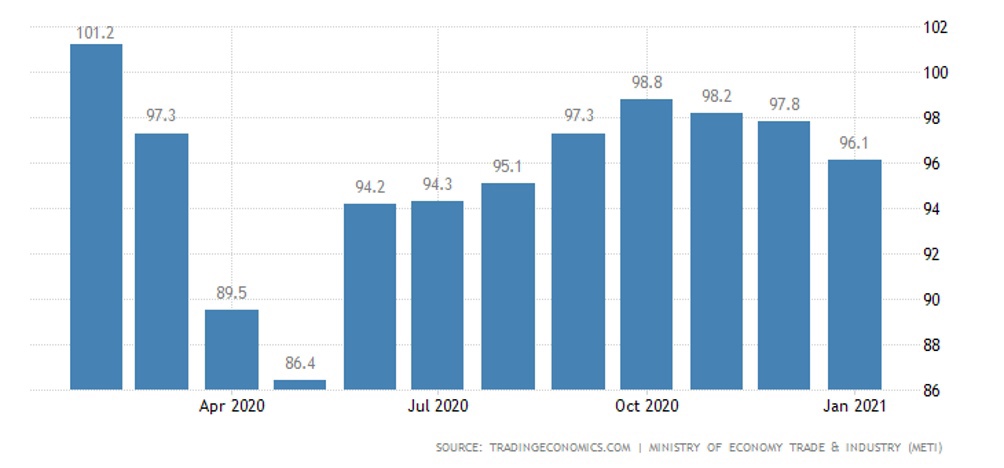

Japan’s service sector activity in January was the lowest in five months:

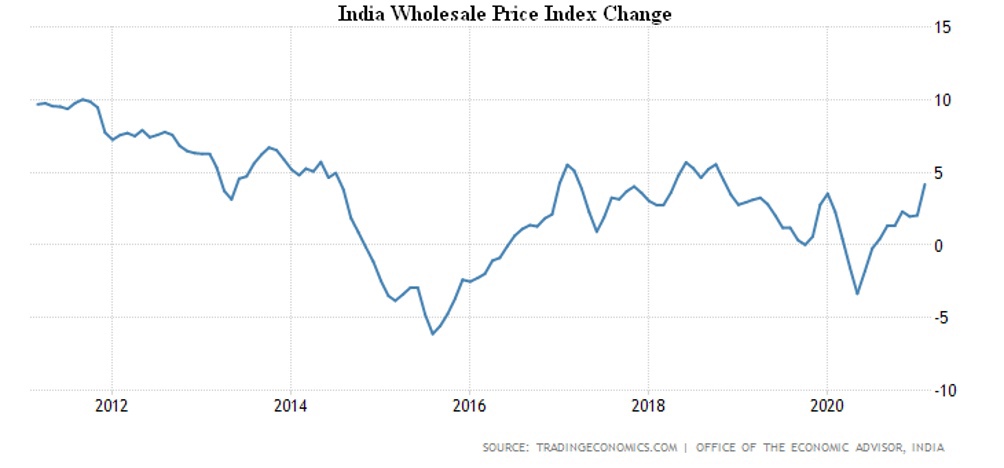

Wholesale prices in India rose by 4,2% per year in February, the highest since November 2018:

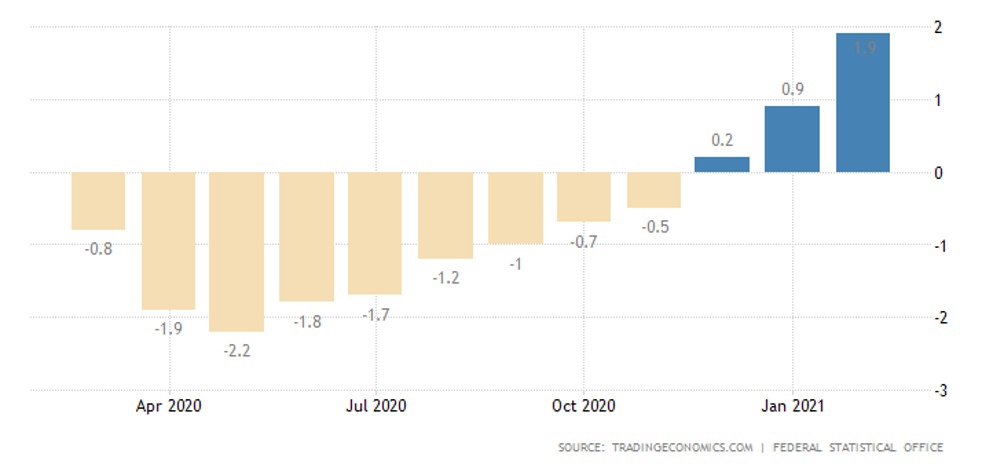

The same situation with wholesale prices in Germany (+ 2,3% per year – the highest since December 2018). A PPI (Producer Price Index) in Germany has peaked since May 2019 (+1,9% per year):

And in Russia PPI 10,7% per year – the peak since April 2019.

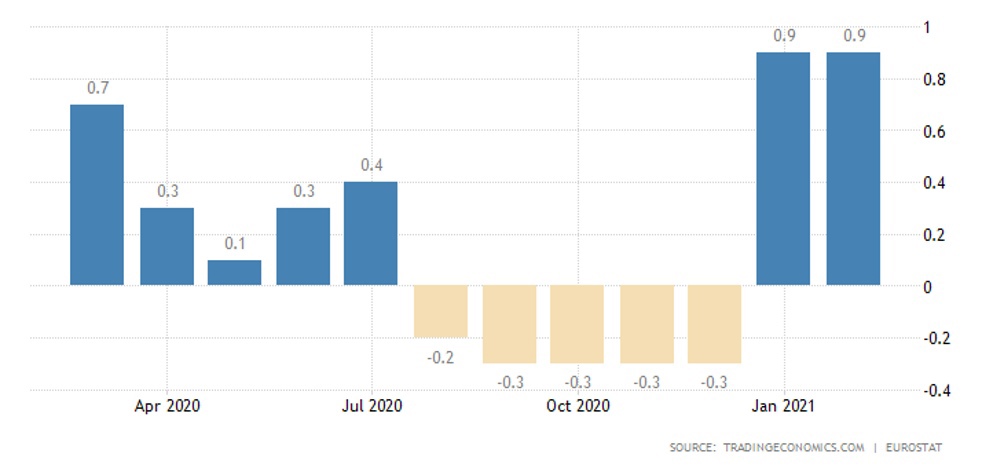

CPI (Consumer Price Index) in Italy in February (+0,6% per year) peaked from June 2019. A similar picture across the Euro Area:

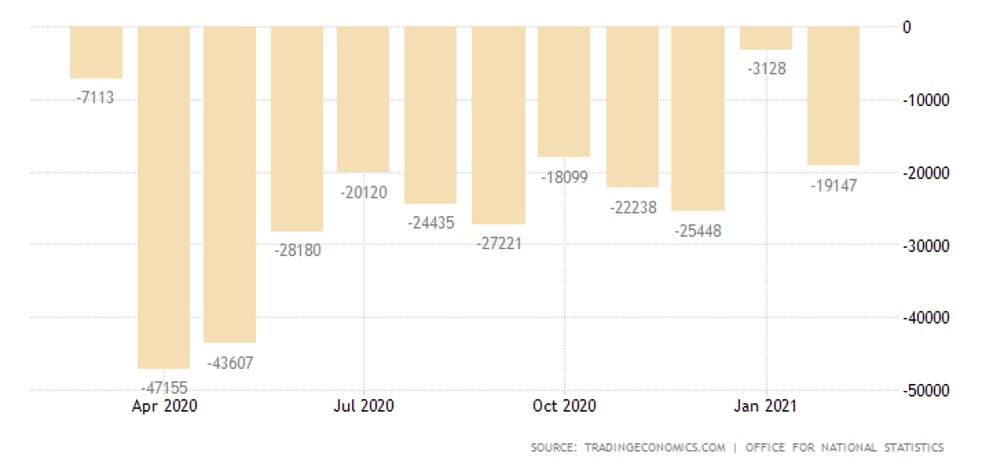

Britain’s fiscal deficit rose again in February (tax revenues -3% per year, but spending increased by a quarter), in general, over the past 12 months, it is a record for all 28 years of observation:

Credit in Indonesia is falling at a rate (-2,15% per year) close to an 18-year high.

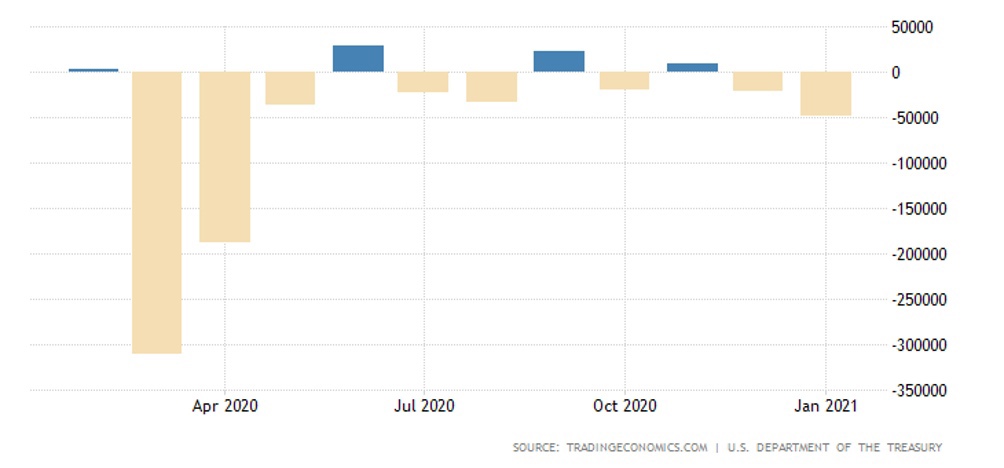

Foreigners are rapidly withdrawing from US government bonds:

And their yield has peaked since January 2020:

And not only in the US: in Germany, 30-year bonds also have a 14-month peak:

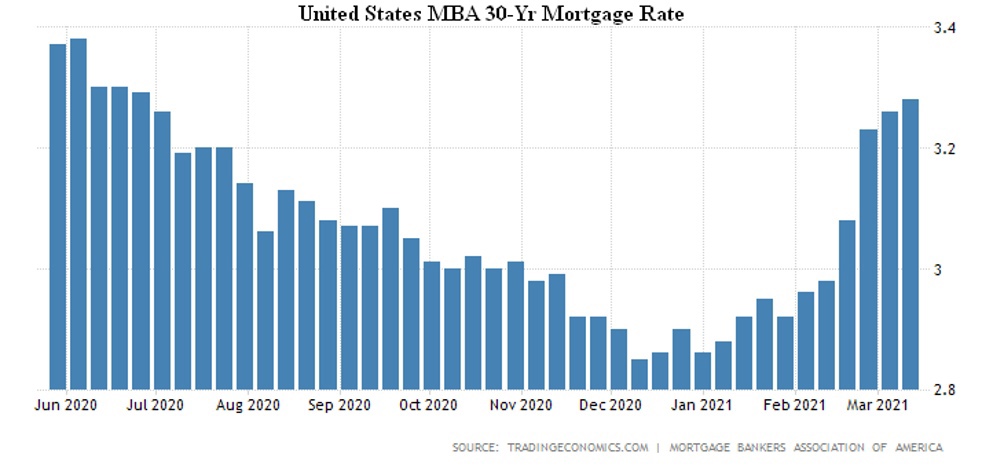

Same US mortgage situation: the rate of a 30-year loan with a fixed interest rate is the maximum in 9 months:

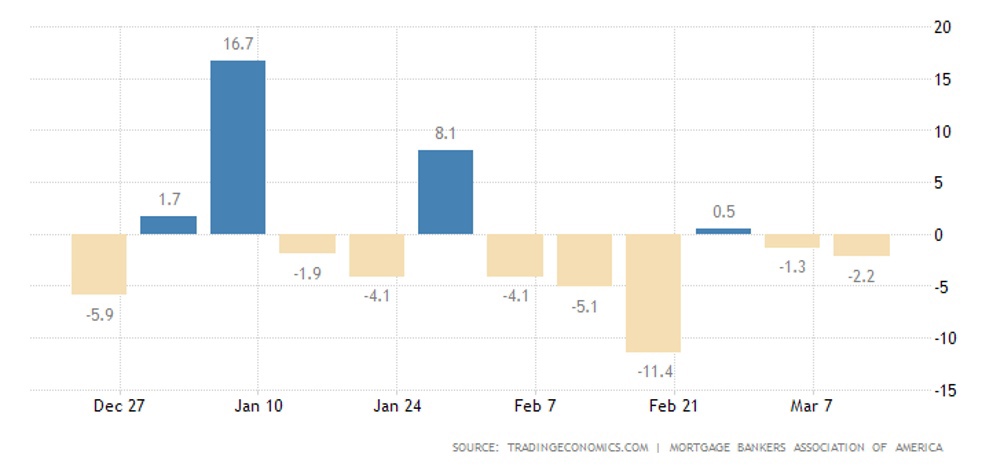

Therefore, the number of mortgage applications continues to decrease:

As a result, the number of new buildings fell from a 14-year peak to a half-year trough, and dwelling approvals fell from a 15-year high to a 3-month low.

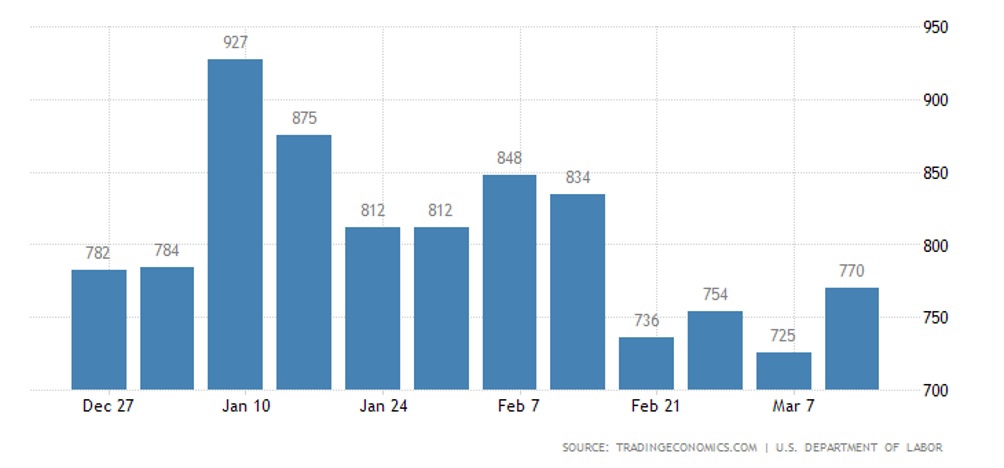

Initial jobless claims in the United States at the monthly peak:

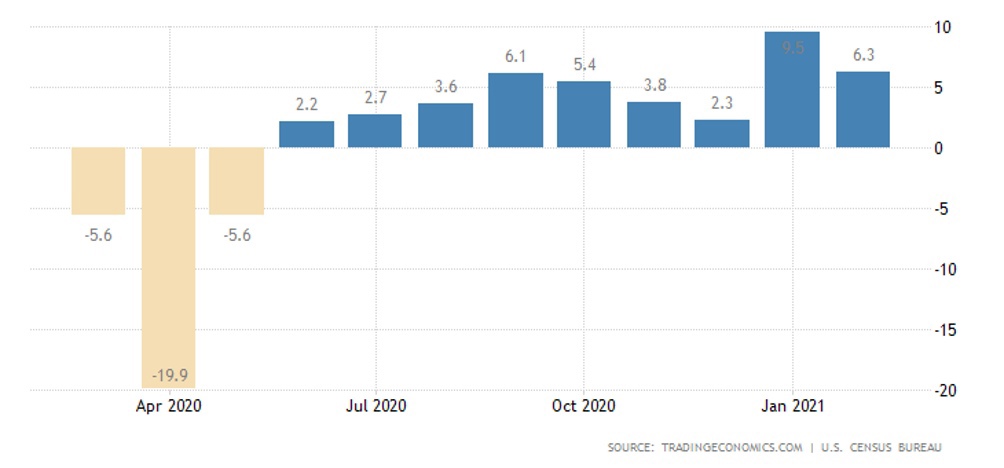

US retail sagged 3,0% per month in February (trough since April) after a surge in January due to December incentives:

But the annual growth is still strong (+ 6,3%), although in January (+ 9,5%) there was a peak since the spring of 2000:

The Fed has kept rates unchanged, promised to keep them at zero for a long time, extended stimulus, increasing GDP and CPI projections.

The Central Bank of England is following the same trajectory.

The Central Bank of Indonesia also left everything unchanged, the Bank of Japan made minor adjustments to the parameters of monetary policy, but no more.

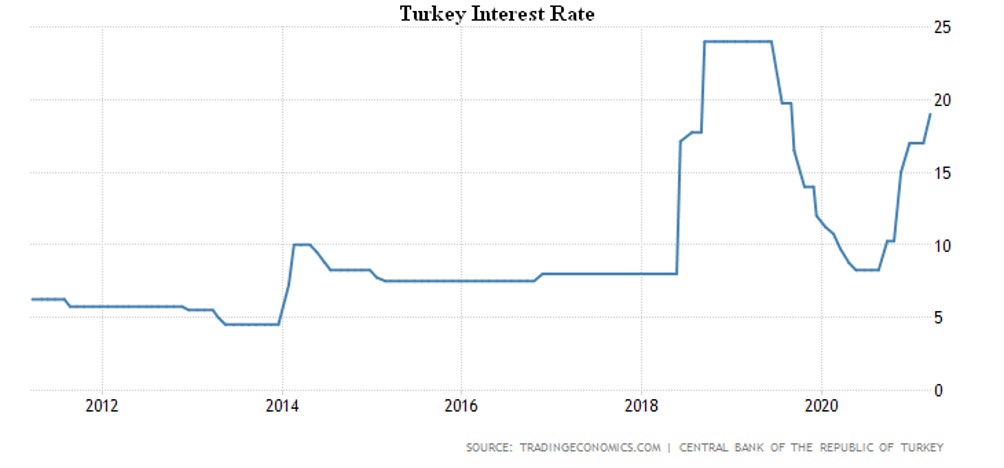

And the Central Bank of Turkey is even tougher: + 2,0% to 19,0% – the maximum since August 2019 and is already approaching a 17-year peak:

But the Bank of Russia has already started to tighten – the rate of 0,25% to 4,50%, complains about inflation.

The Central Bank of Brazil had already set the rate at 0,75% to 2,75%, which was justified by the increase in commodity prices.

Summary: As we anticipated in the previous review, the global recession has continued. The positive retail performance in the US, as well as the Philadelphia index, should not be misleading: it comes at a time when household savings have fallen slightly against a backdrop of compensatory growth and huge emission incentives. Today, savings have resumed growth, and the effectiveness of stimulus measures has fallen sharply.

In general, the picture becomes clear: an inflationary wave begins that cannot be stopped with so much already accumulated and continuing emissions. Moreover, it is also impossible to stem the inflationary surge by raising the rate – as the US Federal Reserve has demonstrated – because of the huge amount of accumulated debt.

However, price increases devalue the real disposable income of households, and compensation is always a one-time measure that does not compensate for job losses. Also, it breeds social parasites that also fail to heal the economy. Thus, even formal retail sales growth may be a fiction, as it is counted in nominal dollars and does not take into account hidden inflation, which sooner or later will reveal itself.

In any case, if emissions are stopped, the fall in aggregate demand will come to the surface, and attempts to offset it by emissions (with savings rising) will inevitably trigger a new inflationary wave. And there is no good way out of this situation, because the world economy is in the grip of a severe structural crisis – a mismatch between household spending and the real income that the economy can generate.

Nor will it be possible to correct structural imbalances with hard and fast methods, as this will inevitably lead to a substantial decline in the quality of life of the population – about 1,5-2 times stronger than in the crisis of 1930-32 in the United States. The political authorities in no country are in a position to allow this to happen, and they are continuing their policy of treating individual symptoms, only aggravating the main disease.

We wish our readers a good weekend and a productive work week!