Period: 17 – 23 October 2020

Top news story: The headline news this week, despite the second (final) round of Donald Trump and Joseph Biden’s debate, is all about the economy. Indeed, the debate has become somewhat irrelevant. It is clear that almost all participants in the elections have made their decision. Also, efforts to rig elections through vote-by-mail should not be overlooked.

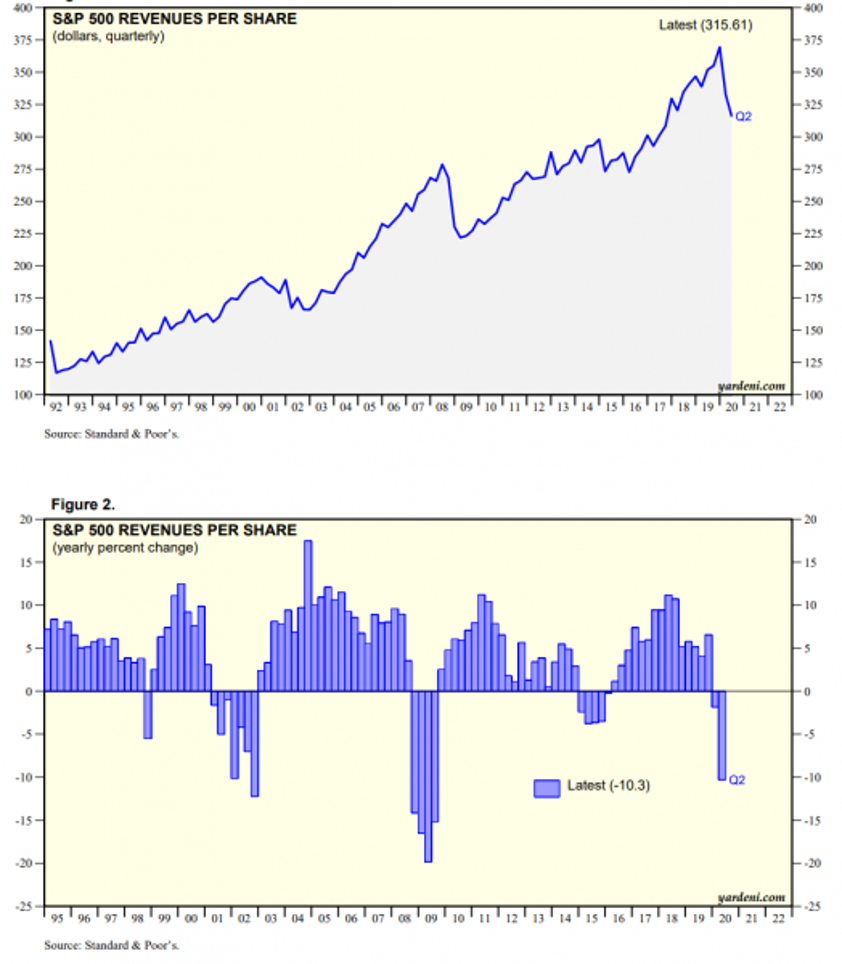

So, the big news is that earnings per share of S & P500 companies for the second quarter of 2020 fell 10,3% – that’s half of what it was in the 2008-2009 crisis. This is the second quarter in a row when the annual rate of income change is in the negative. There have been three negative episodes in the last 30 years: in 2001-2003 out of 7 quarters in a row, in 2008-2009 out of 4 quarters in a row, and in 2015 also out of 4 quarters. However, the worst crisis in 2008-2009 was in both absolute and relative terms.

Gross national product

So what is the difference between the 2008 and 2020 crisis? At least for now? Financial markets collapsed in 2008, but not in the current (as yet?) Among other things, demand support through public injections is now significantly larger than at that time. That is, in fact, the downturn retains its potential, just a slightly different scenario, primarily due to the COVID-19 pandemic.

This situation allows us to make some predictions that a collapse is inevitable. And if we look at the many comments from executives (we cited some in reviews, for example, on gold prices next year), we see that they are already taking this into account. Here is another example…

This year’s most successful investor in anticipation of a bond market collapse

It could happen before or after the elections, predicts the hedge fund manager and founder of Saba Capital, which became the most successful asset management company of this year, earning 80% of the profits.

The above graph shows the dynamics of the US Stock Market Volatility Index VIX (white) as well as the dynamics of the CDX Credit Default Swap Index (blue).

«Never in my 22-year career have I seen such a discrepancy between the favorable debt market and the nervous stock market, — reported in yesterday’s interview with Bloomberg the founder of Saba Capital ($3.3 billion under management) Boaz Weinstein. His flagship fund earned 80% this year, which was the best return of all hedge funds monitored by HSBC. — This can lead to incredible movement before or after 3 November»

The expert notes that the VIX volatility index stubbornly refuses to decline and is currently twice the pre-crisis levels, indicating a nervous mood in the stock market. While the debt market is showing remarkable complacency: the CDX credit default swap benchmark index is almost back to the beginning of the year (see the graph at the beginning of the article). Boaz Weinstein does not bet on stocks and bonds based on fundamental indicators, such as cash flow or earnings. Instead, he enquired about the ratios of financial assets, trying to identify those that for some reason differed significantly from similar ones. He then makes a bet to correct these imbalances. It was for this reason that he drew attention to the discrepancy between VIX and CDX, which had been running in tandem for years, after which VIX began to grow in August and CDX continued to decline. The heightened level of expected volatility in the stock market is easily explained, given the uncertainty surrounding the outcome of the US election, the continuing dynamics of the COVID-19 pandemic, and the prospects for economic recovery. Given low rates and rising defaults, we see calm in the debt market as unnatural.

The expert said that he is betting on the reduction of some bonds, but refrained from any specifics. According to him, he expects a sharp fall in the debt market that will be triggered by events other than the retreat of the FED. For example, the second wave of COVID-19 will prove far more damaging than people expect, and the results of the US presidential election will be challenged.

«These are all ‘known unknowns’, but there may be ‘unknown unknowns’ that will have an equally significant impact on the market» — the investor concluded.

It should be noted that the uncertainty surrounding the elections has not disappeared at all, this time not ending on 3 November, but likely to last for at least two weeks.

Macroeconomics

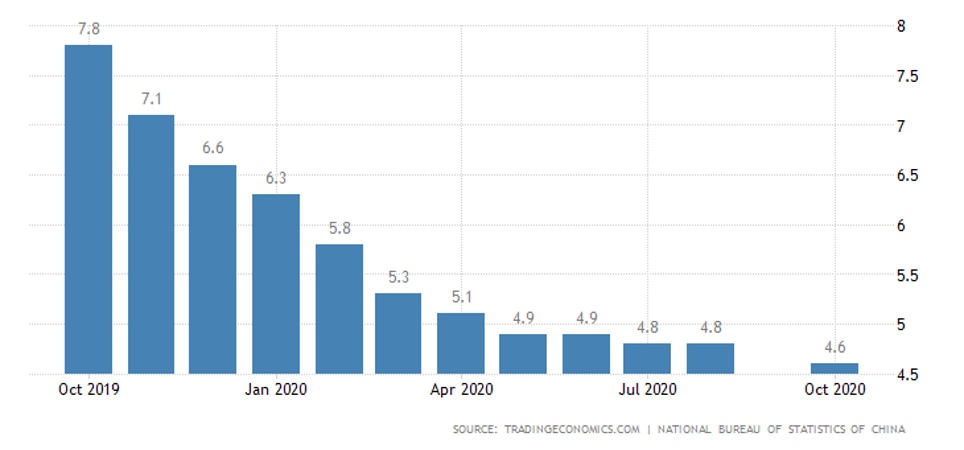

China’s GDP in the third quarter grew by 2.7% per quarter and 4.9% per year – less than expected, but not bad. It should be noted that, as with the GDP of China and the US, it is very difficult to separate real growth from the transfer of part of the economy’s emissions support to the corresponding balance sheet items. Given the scale of this support in these economies (up to 25% of GDP), it is very difficult to deal with their GDP. In the US, at least, accumulated debt has grown significantly faster than GDP since 2008, raising some suspicions…

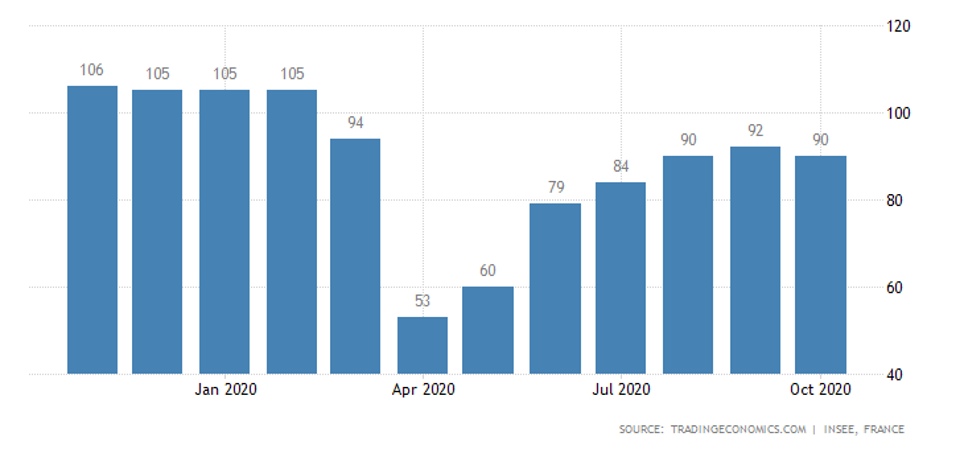

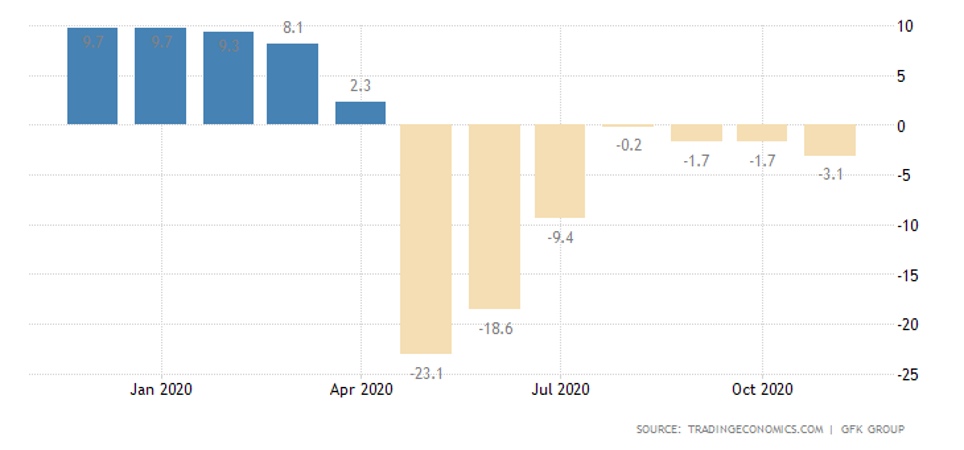

French business became pessimistic:

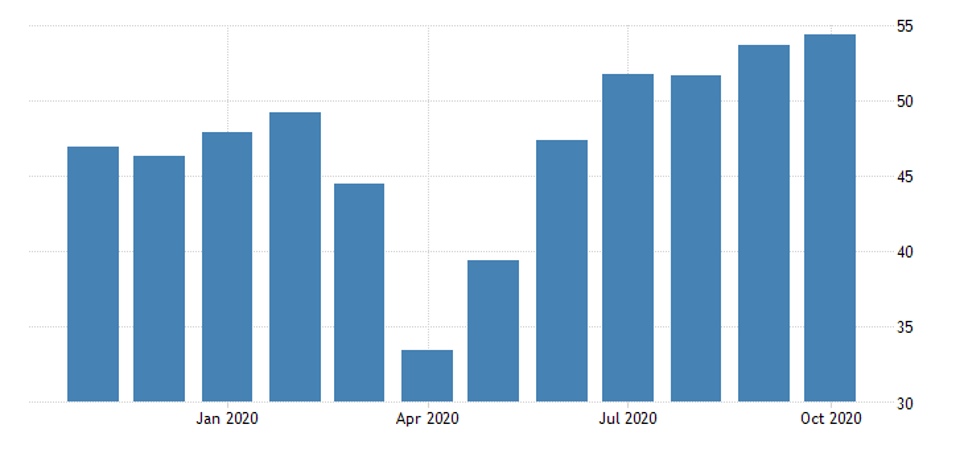

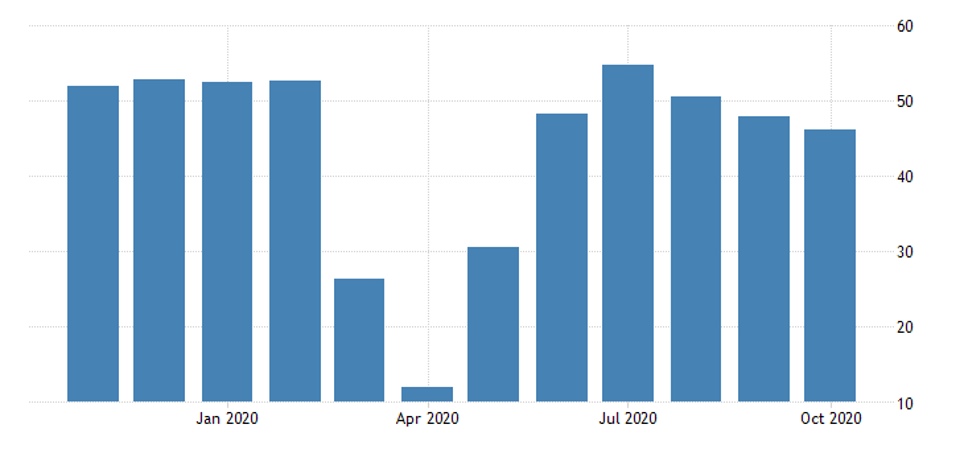

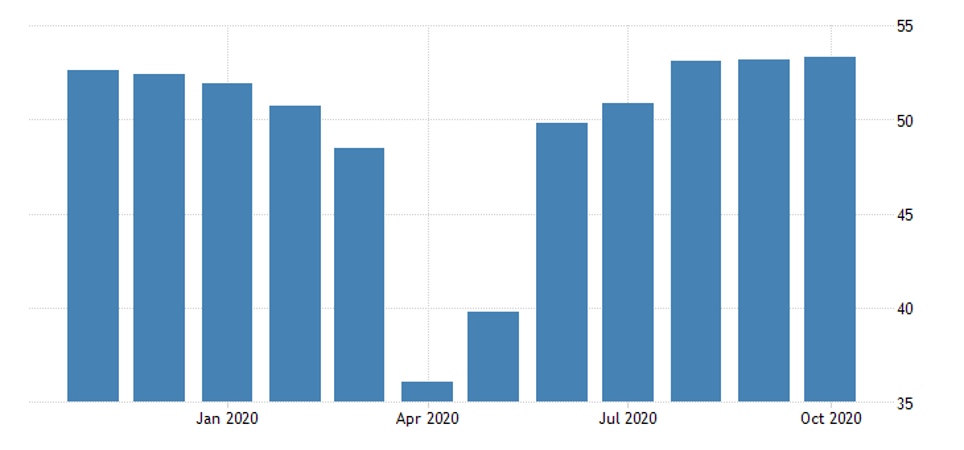

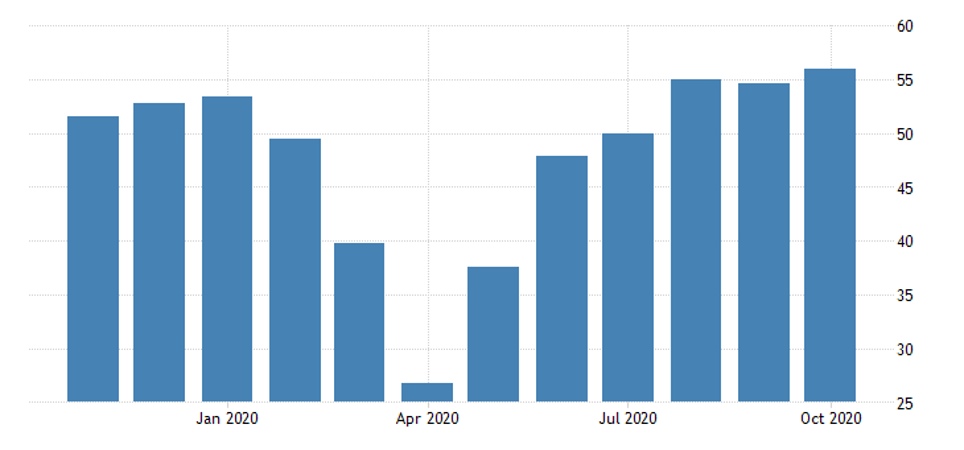

Preliminary estimates of the October PMI gave a similar picture worldwide: recovery of production, in services again deteriorating. This is the case in Japan, Britain, France, Germany, the Euro Area as a whole:

And only in the US did production get a little worse:

And the service sector continues to strengthen:

Japan’s CPI is 0,0% per year – the lowest in four years, declining trends continue. Housing prices in 70 largest cities in China increased by 4,6% per year – the lowest since February 2016:

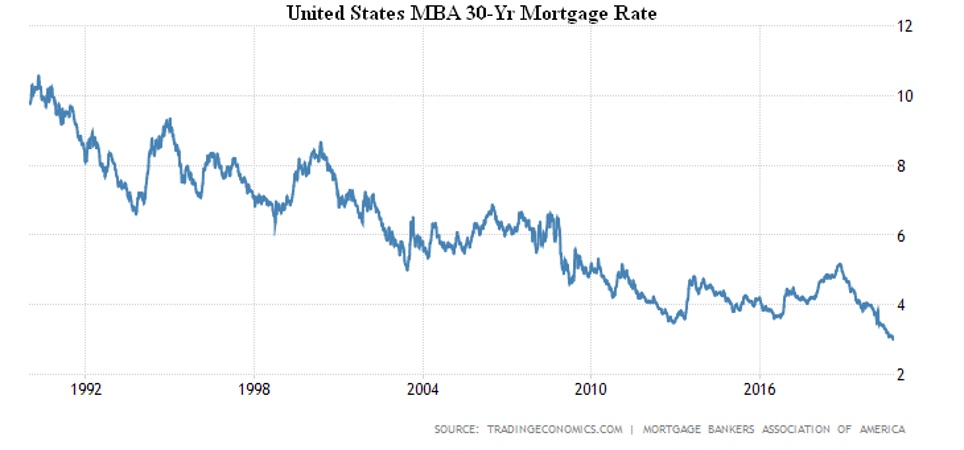

In fact, there is a renewed tendency to transfer some of the Chinese economy’s emission-generating stimulus resources to the real estate market – given the effects of the quarantine crisis of the first half of the year. The opposite is true in the United States, where the real estate market is breaking records, owing to the ever-cheaper mortgage:

The consumer climate in Germany is the worst in 4 months:

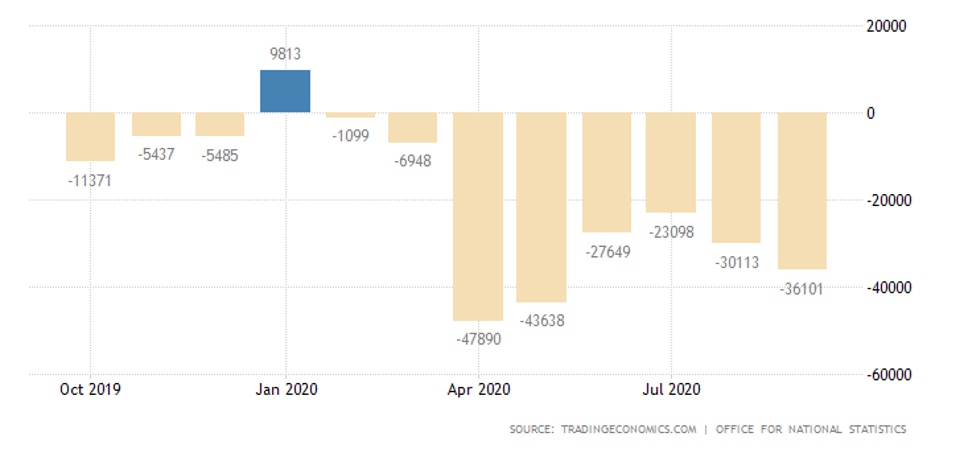

With what was worse only in July, the wider business community has already come to realize that there is no hope for recovery. Note that in the eurozone as a whole, the minimum for 5 months, and in Britain the picture is even worse. Given that Britain’s budget deficit seems to be returning to spring’s historical antidotes, the picture there looks very sad:

For this, Moody’s agency cut its rating from «Aa2» to «Aa3».

The Central Bank of China has left monetary policy unchanged, as has the Bank of Russia. The Central Bank of Turkey left the base rate unchanged, but widened the difference between its different rates.

Summary: We think that already most market participants are preparing for new serious problems. This is likely to be strong inflationary processes and a collapse of financial markets. It should be noted that, given the huge emissions injections, the recession effects associated with the slowdown in price increases mean that the money thrown into the economy does not flow into investment (with the exception of China).

In fact, everyone who has managed to accumulate some «airbag» considers it in this capacity and does not intend to invest any money anywhere. As a matter of fact, a similar effect has begun to emerge in Russia, and large companies are actively closing already announced competitions for investment projects. In other words, this is the calm before the storm, or rather, before the collapse of the stock markets.

Overall, it can be seen from the week’s outcome that, while by early October the pessimism was more prevalent in large businesses, they are now actively entering the medium and small-sized segment, which was hitherto susceptible to mass propaganda «recovery». Reality took its toll.