Period: 12 – 18 September 2020

Top news story. The main news this week was a decision by a WTO panel that tariffs on Chinese goods imposed by the US under Donald Trump contradicted a number of articles of the General Agreement on Tariffs and Trade. Of course, the President’s subsequent abrupt reaction did not take long, but he has not yet spoken of US withdrawal from the WTO. The WTO is one of the main Bretton Woods institutions mandated by the Bretton Woods Conference in 1944. The WTO was long-standing and the General Agreement on Tariffs and Trade, GATT, was the first phase. Donald Trump, whose economic model implies abandoning global markets, has made the WTO one of its priority targets, and a decision in favor of China could significantly accelerate the process of destroying this systemic institution.

In fact, this decision showed that China in the battle «Donald Trump vs Joe Biden» is on the side of the latter, which represents the interests of the financial globalists, at least in the economic sphere.

Macroeconomics

In Japan, industrial production surged by 8,7% per month in July, but the annual decline is strong (-15,5%). The situation is similar in the Euro Area: +4,1% per month and -7,7% per year. In the US, production in August was 0,4% per month (the lowest in 4 months) and -7,7% per year (in July it was -7,4%).

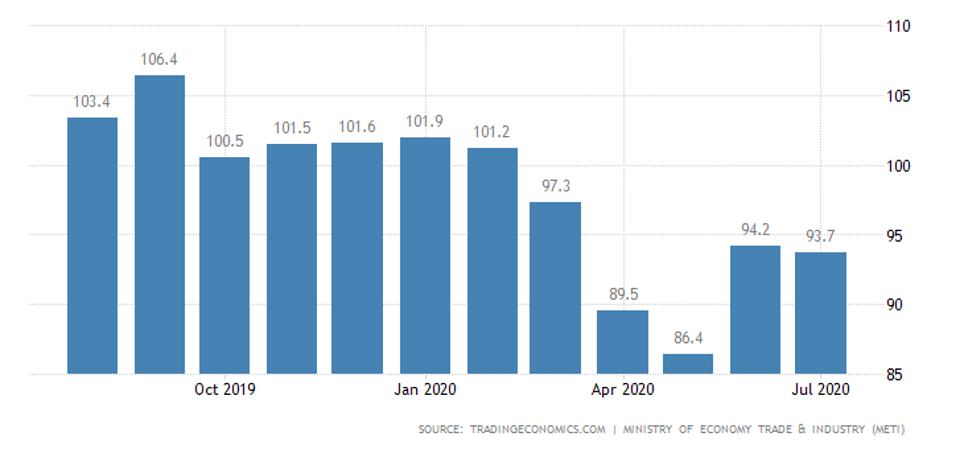

Services activity in Japan fell again in July after a lone bounce in June:

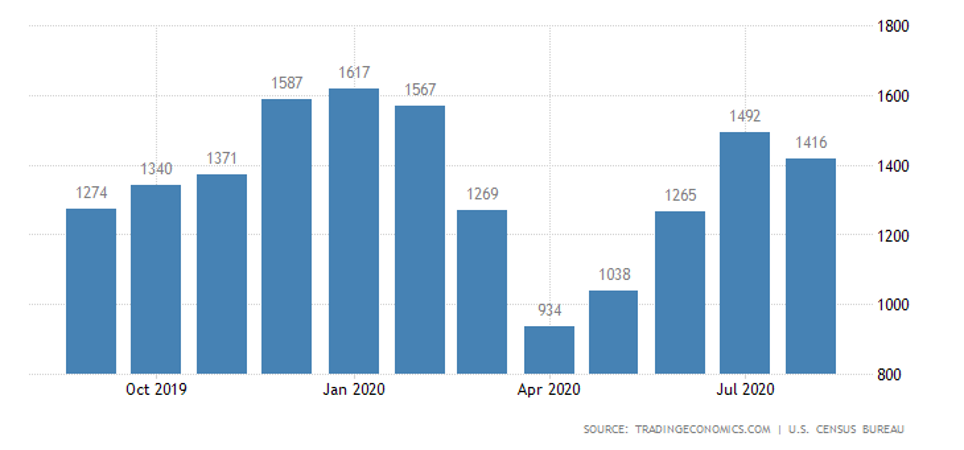

Construction performance in the US slowed down in August after the previous boom in record-breaking low-cost mortgages:

Inflation in France in August -0,1% per month and 0,2% per year – a four-year repeat of the minimum. In Italy, the CPI is +0,3% per month and -0,5% per year – a repeat of the record low for all 58 years of observation.

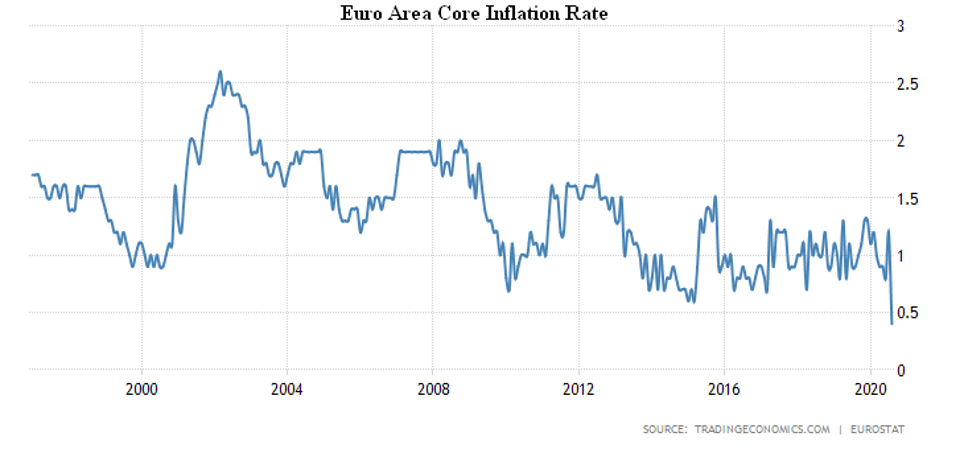

In the Euro Area, -0,4% per month and -0,2% per year (the lowest since spring 2016); no food, fuel, alcohol, and tobacco record trough +0,4% per year:

In Japan, prices without food and fuel are -0,4% per year – the lowest in 4 years.

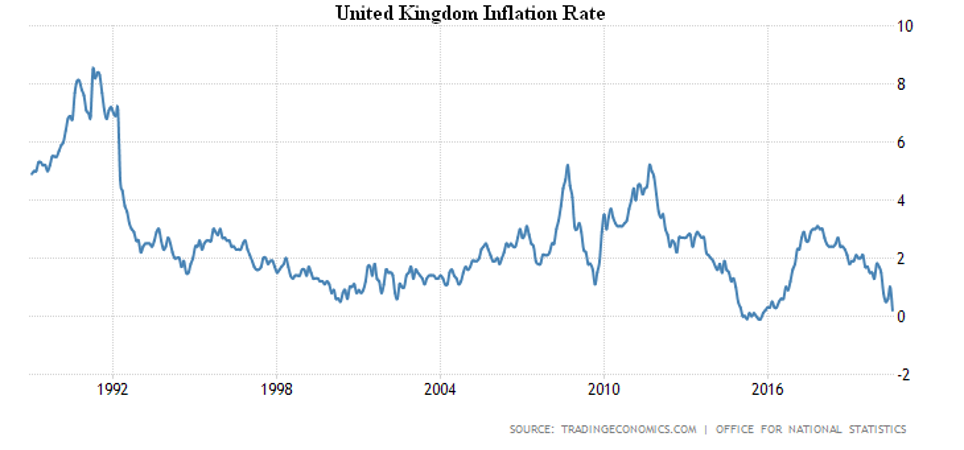

Inflation in Britain in August is -0.4% per month (trough since January 2019) and 0.2% per year (the lowest since December 2015):

Britain’s average wage in May-July fell 1,0% a year after -1,2% in April-June, which was the worst in 11 years.

Unemployment claims in the US declined, but the total number of recipients rose again, to 29,8 million.

Retail sales in the US rose by 0,6% per month in August instead of the expected 1,0%, July also revised downwards; net sales are already negative (-0,1%) – soon, so will the whole.

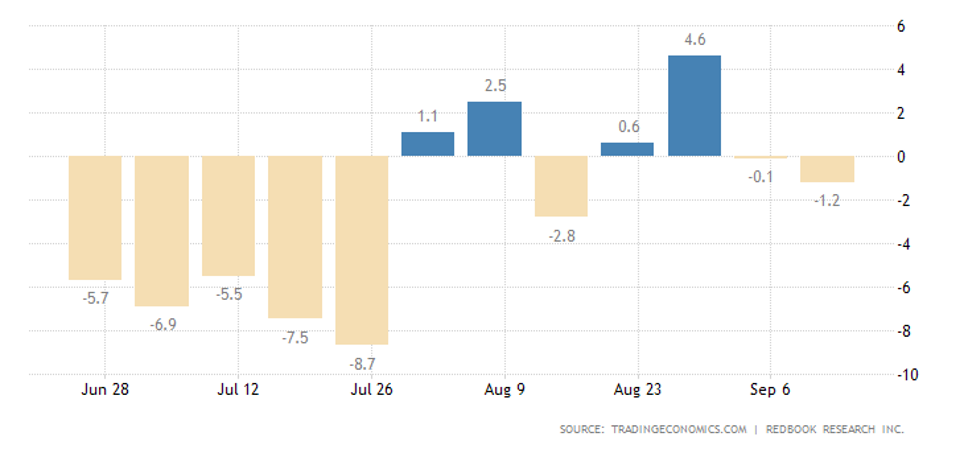

September Redbook US Retail Sales Monitor returned to annual negative values:

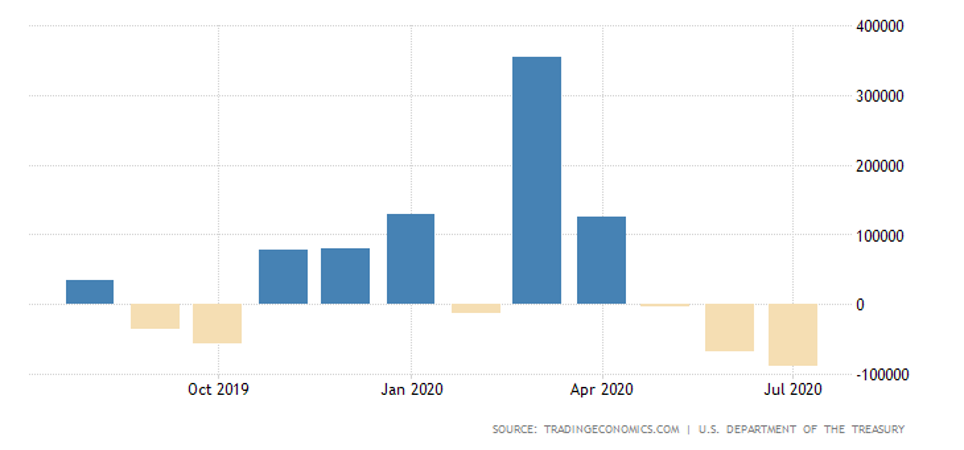

Foreign investors in July reduced US government bond purchases 10,5 times as compared to June:

The US Federal Reserve has left monetary policy unchanged, but there are two dissidents on the Open Market Committee (the Fed’s decision-making structure) – combined with the increase in GDP and unemployment forecasts, the market took it as a sign of discontent with the Central Bank’s excessive softness and its unwillingness to expand incentives. This was a formal reason for the stock markets to collapse.

The Bank of England kept the rates and the size of the stimulus in place, but made clear that it could drive the rate down and expand asset purchases if the economy deteriorated and/or inflation slowed further.

The Bank of Japan has left everything as it was and assessed the economy as slightly improved.

The Central Bank of Brazil, too, did not change anything and made it clear that the chances of new incentives are minimal or even non-existent.

The Central Bank of Indonesia maintained its previous rates but extended the softening of reserve requirements for banks lending small businesses.

The Central Bank of South Africa has not changed anything, but has worsened economic forecasts – yet in 2021 it is ready to raise rates.

The Bank of Russia seems to be completing the cycle of monetary easing, and the rate has remained the same.

Summary: Apparently, the events of the third quarter (which will end in two weeks) have shown not only that the recovery has been less than most experts expected, but also that the crisis potential of the world economy is very high. Clear deflationary signs against the background of huge emissions suggest that there is no willingness to invest in the real sector, and consequently there is neither wage growth nor unemployment reduction.

We have already repeatedly explained this phenomenon due to the fact that during the period of the economic model «Reaganomics», with its direct stimulation of private demand, colossal structural distortions have accumulated. In the US, China, and Western European countries, they reach 25% of real GDP (i.e., demand stimulus is about a quarter of GDP), although the mechanisms of this stimulus vary.

In the US, for example, much of the problem is related to the fact that household savings, which have remained very low in recent decades, have begun to increase in the context of the crisis. This devalues attempts at further stimulus and, in our view, the ongoing structural crisis is unstoppable. However, the theoretical chances of a resumption of the optimistic scenario still remain, the situation will be definitively clarified by the end of the autumn.