Time period: 29 January – 4 February 2022

Top news story. The highlight of the week was the joint statement of the Russian Federation and the People’s Republic of China on a new era of international relations and global sustainable development, which was made public during the visit of Russian President V. Putin to China. Why is this statement central to the economy?

All today’s economic model is built within the Bretton Woods system, which was adopted in 1944 with minor changes, the most famous of which was the abolition of the “Gold standard” in the United States on August 15, 1971 and following modifications. This model was driven by the economic resources of the United States, and therefore provided maximum preferences for the state, with almost all participants benefiting. However, the US also suffered negative consequences – in particular, its share of the world economy fell from more than 50% to less than 20% (according to various estimates, today between 16% and 18%).

As a result, the economic base of the world’s global geopolitical order has shrunk sharply, and it has not been possible to maintain the living standards of a significant proportion of the world’s population. Accordingly, already by the beginning of the XXI century it became clear that the collapse of the dollar world is unavoidable (see, for example, A. Kobyakov, M. Khazin “Sunset Dollar Empire and the End of the ‘Pax Americana’,” M., 2003). But if the old rules are no longer valid, someone must formulate new ones. If everything is clear with economic models – each currency zone will have its own system – what about interzonal interaction?

The statement just mentioned indicates that the world’s largest markets and economies (China, Russia, and implicitly India) are proposing such a rule. Of course, they still have to be operationalized, and a new financial model needs to be attached to them, but they already exist. And in this sense, on February 4, 2022, will undoubtedly go down in the world history of the 21st century.

And for ordinary people and entrepreneurs this is very good news – it is safe to say that we will not return to feudal order since there is clearly a new system that changes the process of destruction into creation.

Macroeconomics

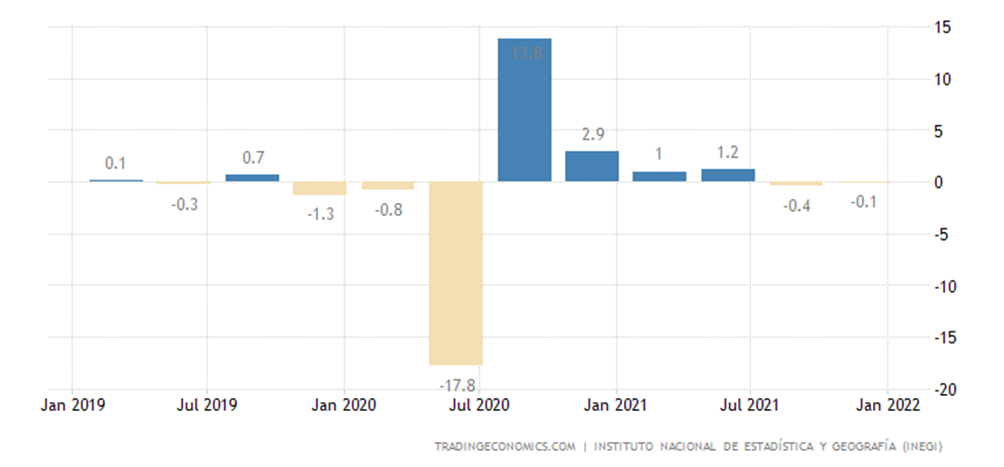

Mexico’s GDP has been falling for two consecutive quarters:

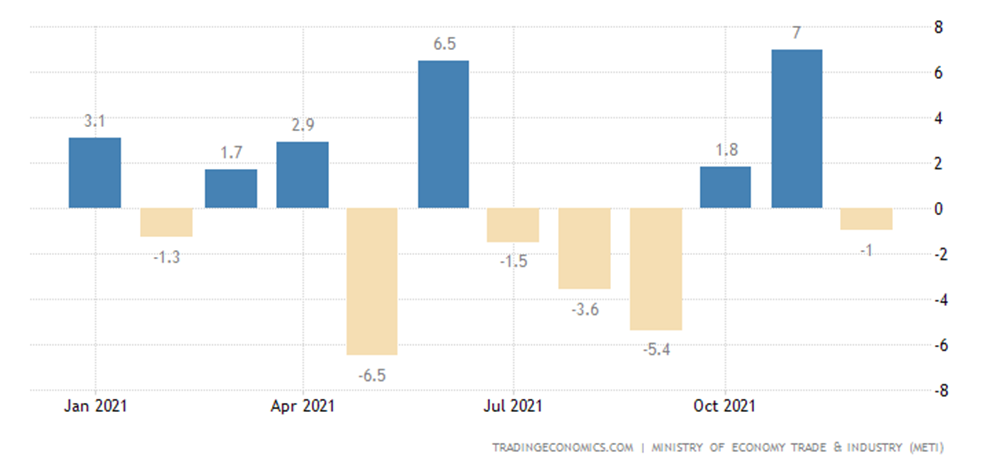

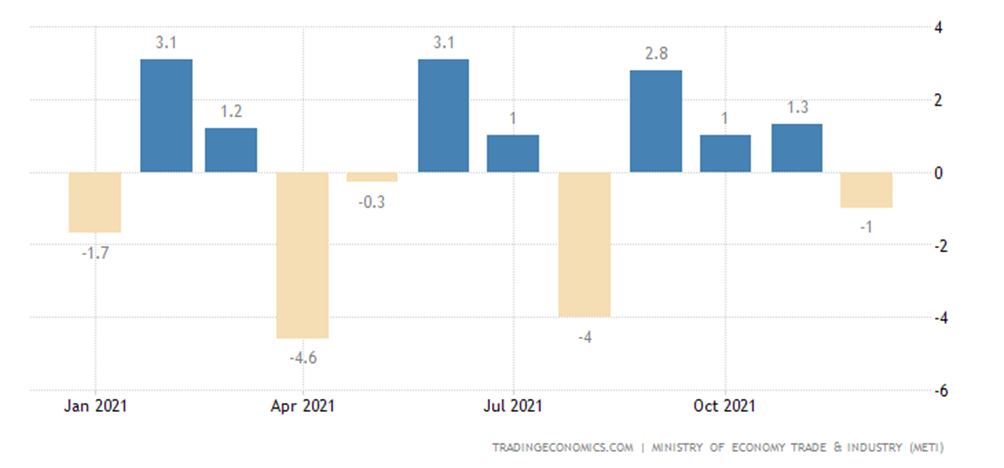

Industrial production in Japan was -1.0% MoM:

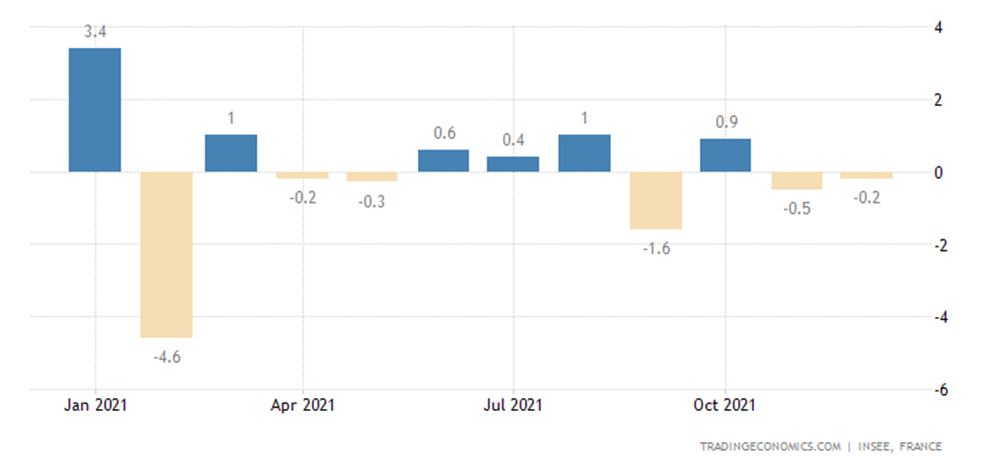

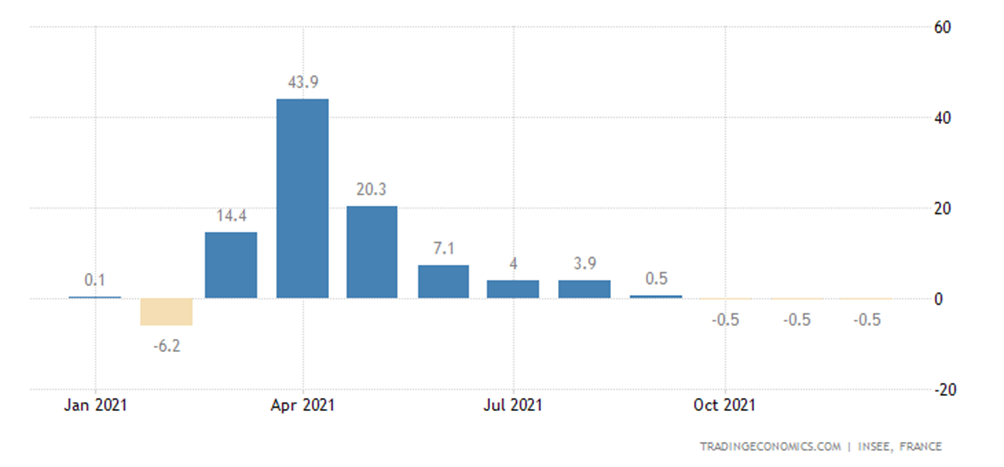

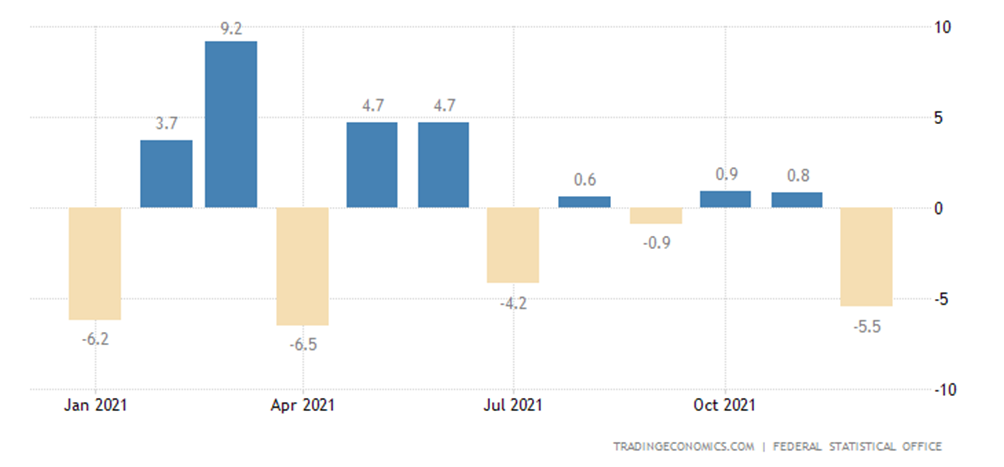

In France, industrial production -0.2%, the second quarterly negative in a row:

As a result, the annual performance was negative for the third consecutive month (-0.5%):

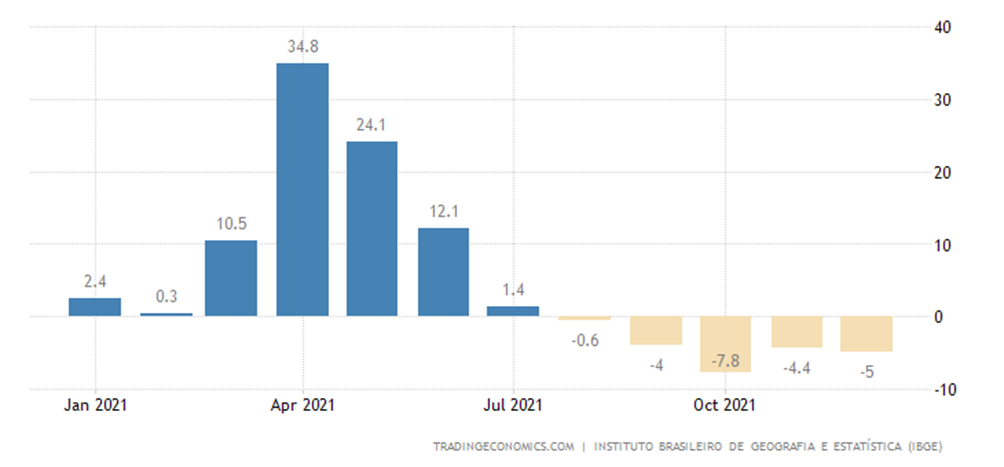

The output of the Brazilian industry has been maintained in the annual red for 5 months:

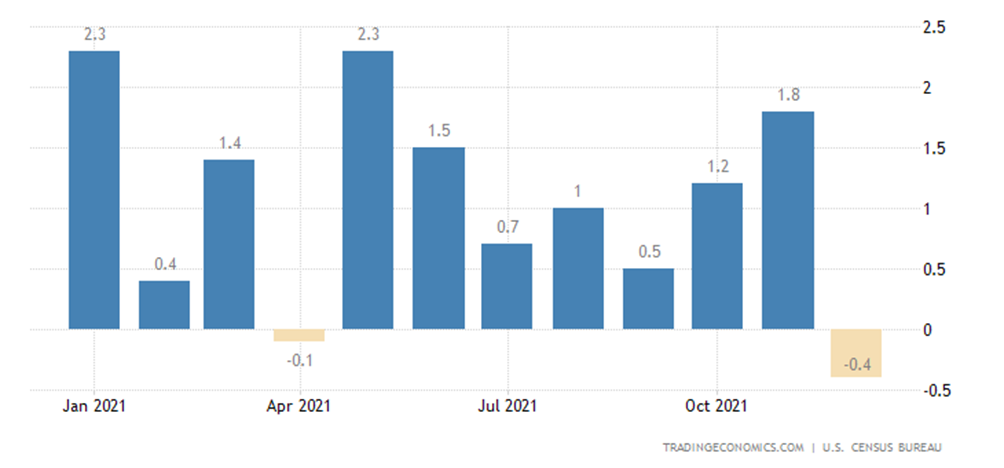

Factory orders in the United States -0.4% per month, the worst performance in 20 months:

As a precaution, we recall once again that all these figures are part of official inflation. Since the reality is worse (often many to many worse), the indicators need to be reduced by the difference between official and real inflation, with all the resulting conclusions.

China’s production PMI (an expert assessment of industry conditions; index value below 50 means stagnation and recession) is the worst in 2 years and in the recession zone (49.1 points):

Official figures look better, but only slightly – in industry 50.1:

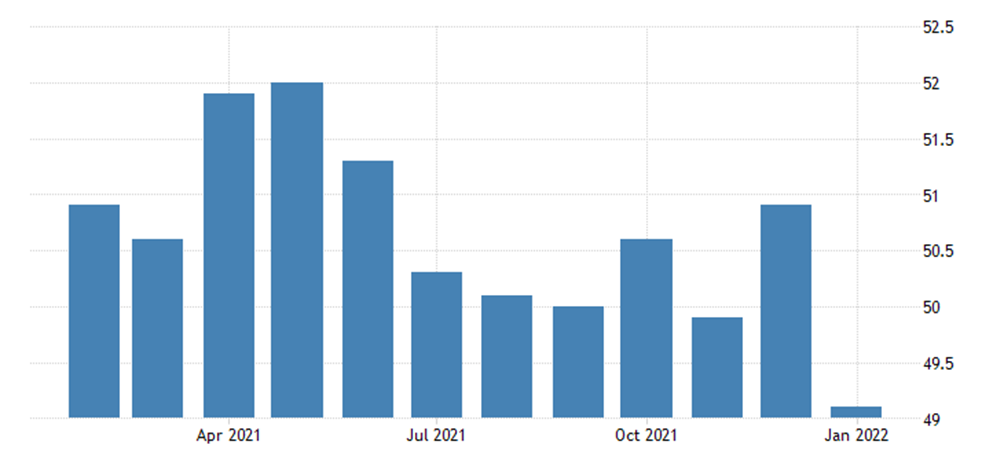

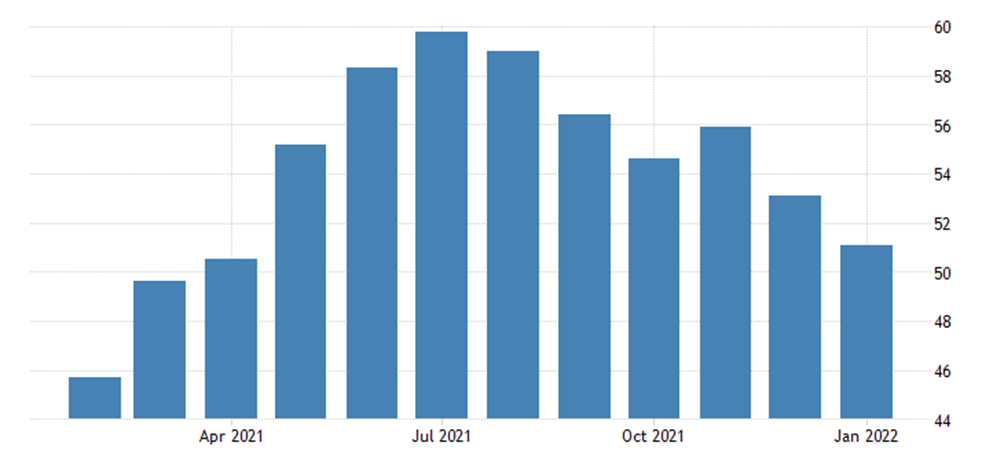

In non-manufacturing sectors there is 5-month low 51.1:

US non-manufacturing PMI is the weakest in 11 months:

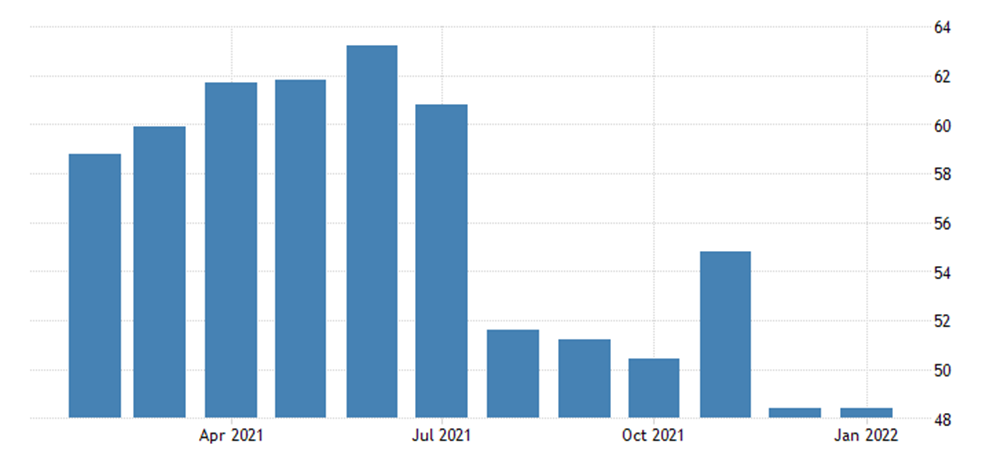

Australia’s industry PMI is in decline and has been at the trough since September 2020:

Services are also in decline:

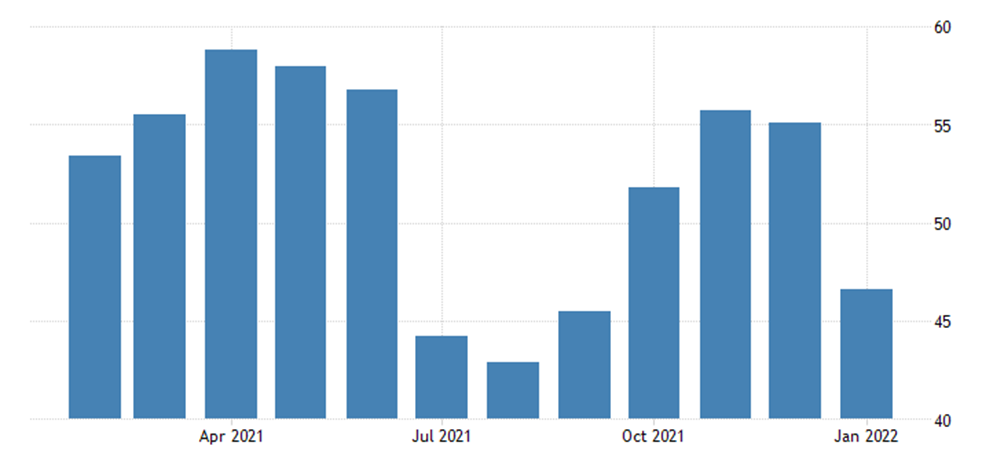

Japan’s services sector is in recession:

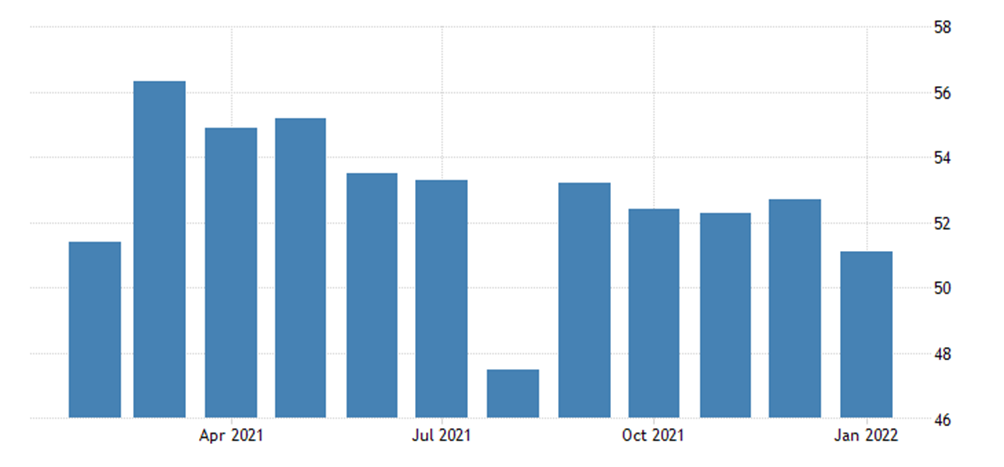

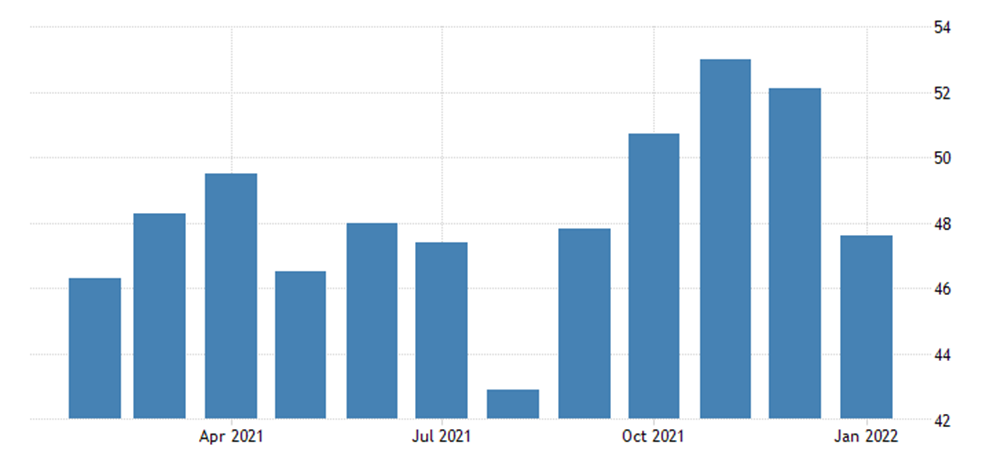

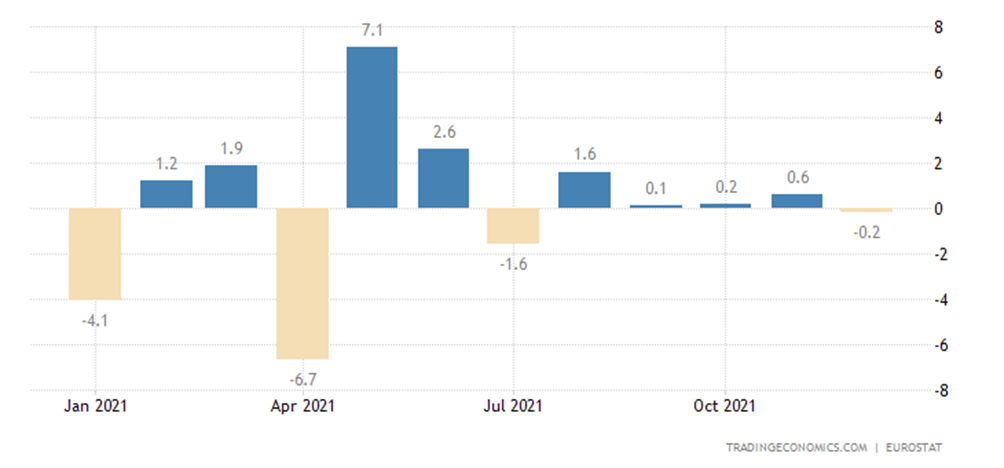

The eurozone has not yet experienced a recession (51.1), but there is a 9-month low:

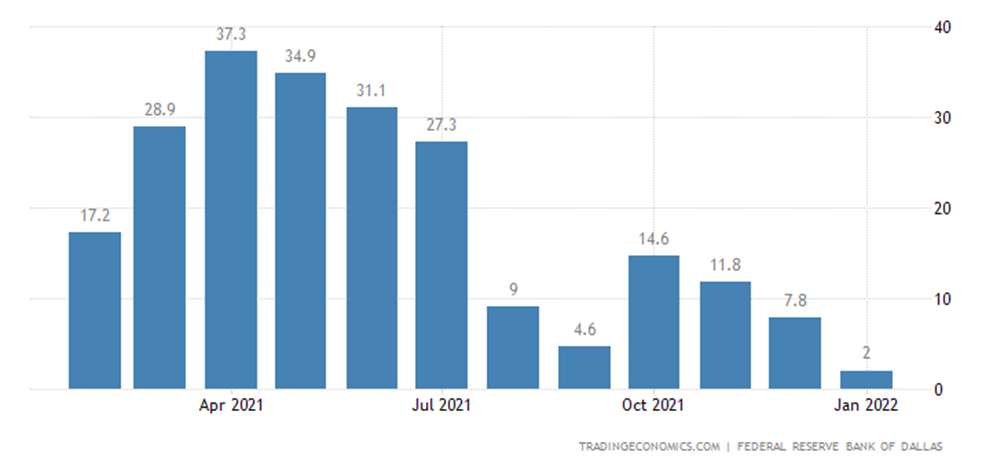

United States Dallas Fed Manufacturing Index at weakest in a year and a half:

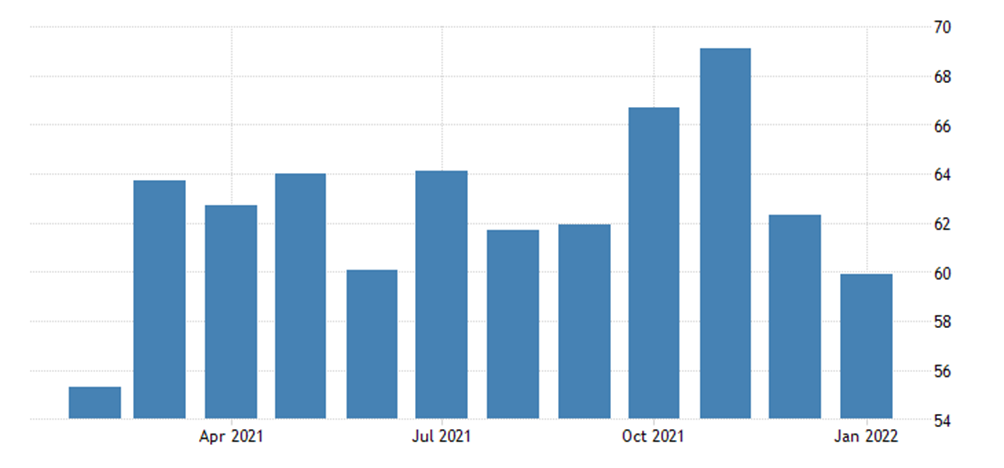

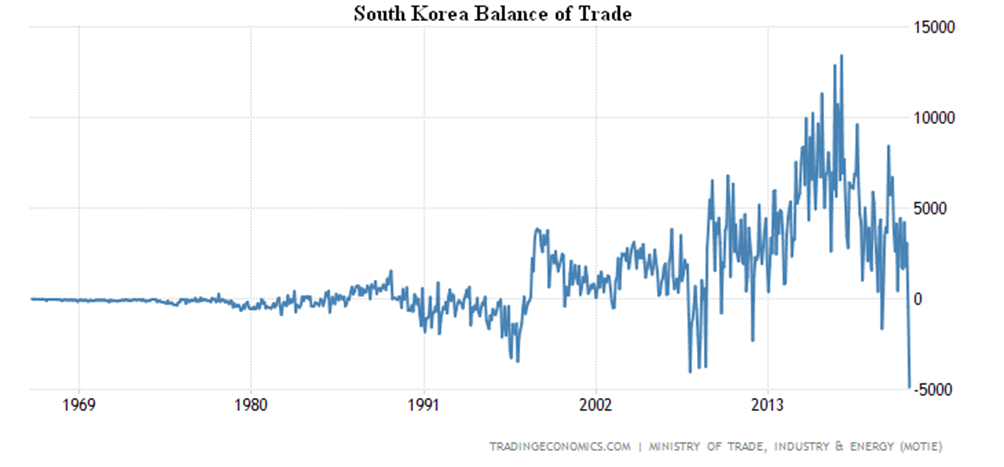

South Korea’s trade deficit is record-breaking:

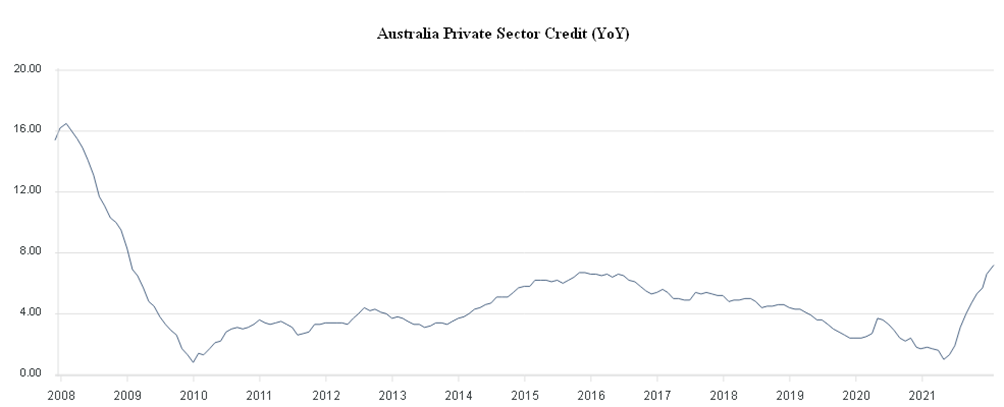

Private sector lending in Australia has been at 7.2% per year, at most since 2008, indicating not only an increase in inflation but also a deterioration in people’s standard of living:

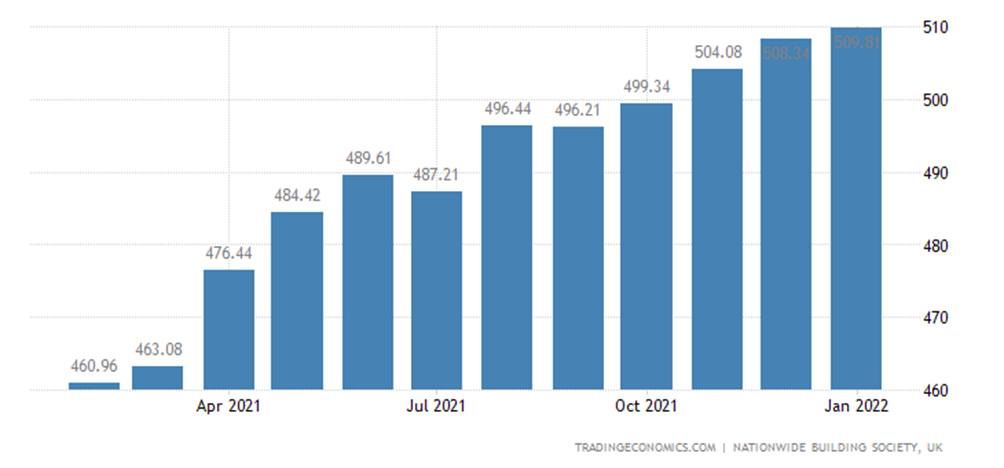

House prices in Britain started to pick up again (+11.2 per year):

As usual, inflation rates beat records.

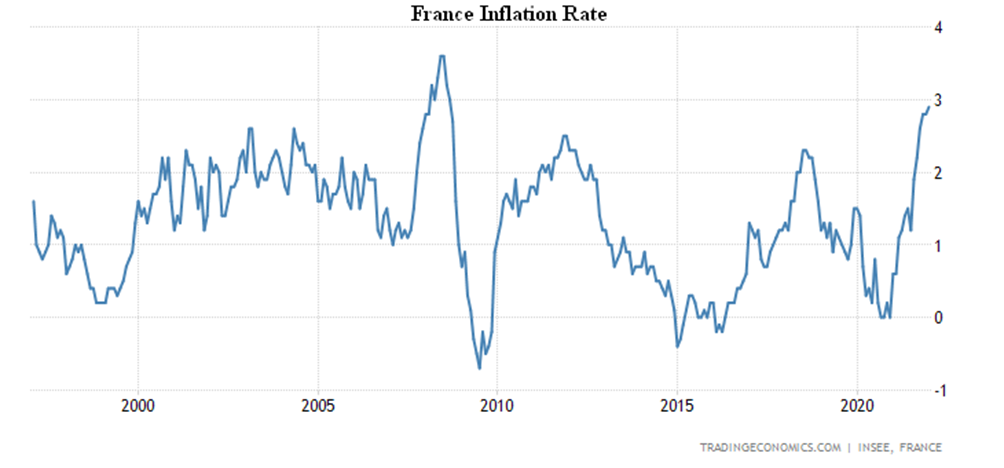

CPI (Consumer Price Index) of France +2.9% per annum, it’s a peak since 2008:

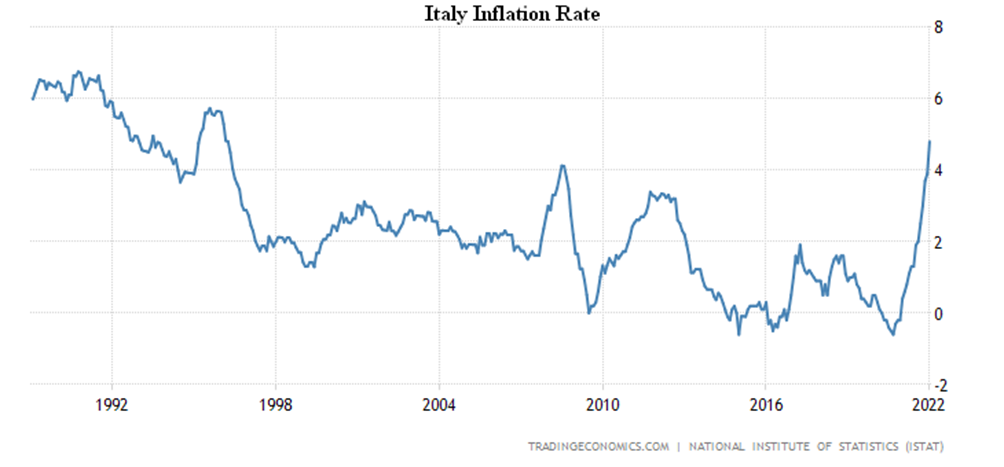

CPI of Italy +4.8% per annum, which is the highest since 1996:

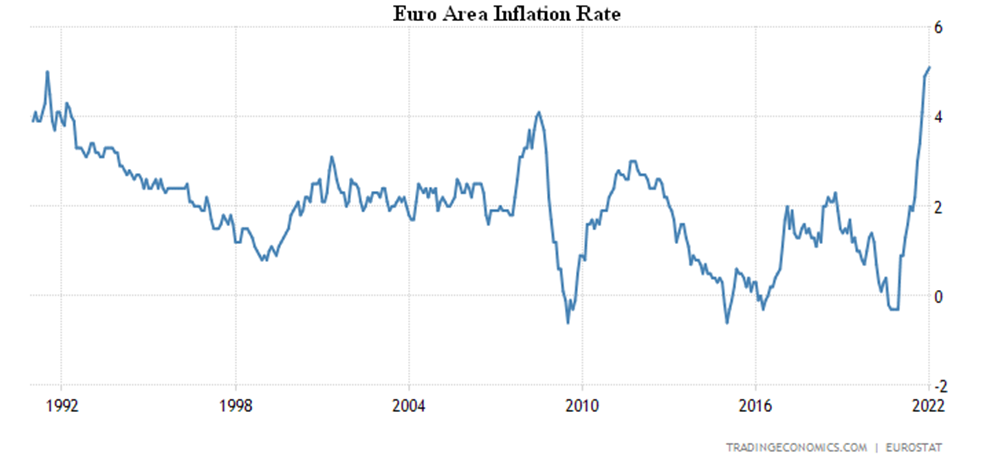

CPI of the Euro Area +5.1% per year, which is a record for 31 years of survey:

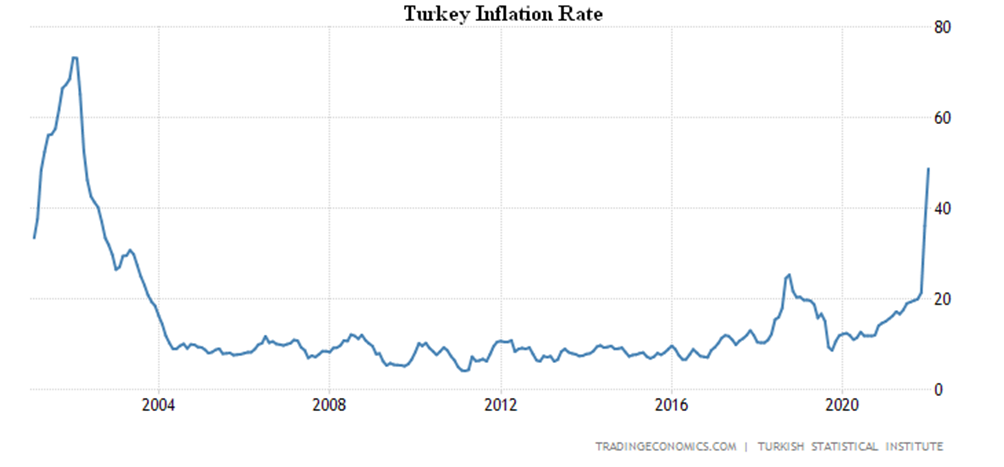

CPI of Turkey +48.7% per annum, which is 20-year high:

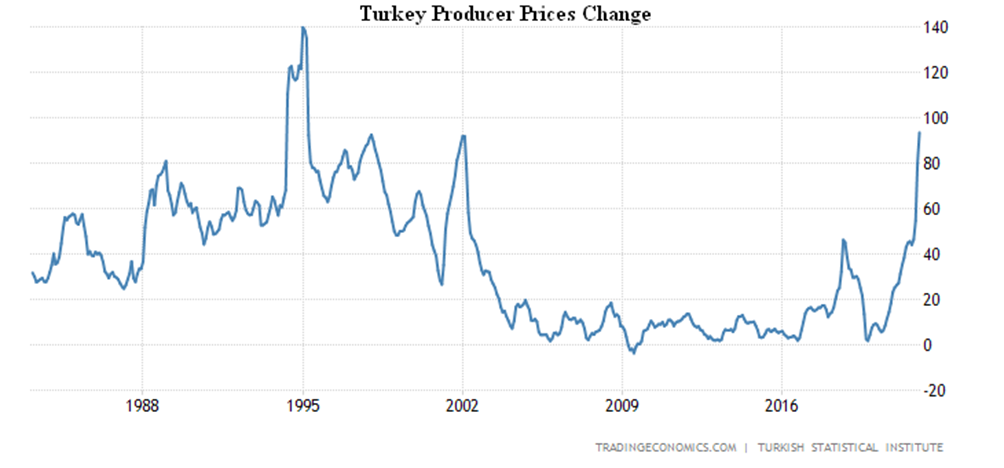

And PPI of Turkey (Producer Price Index) is +93.5% per year, the highest ever since 1995:

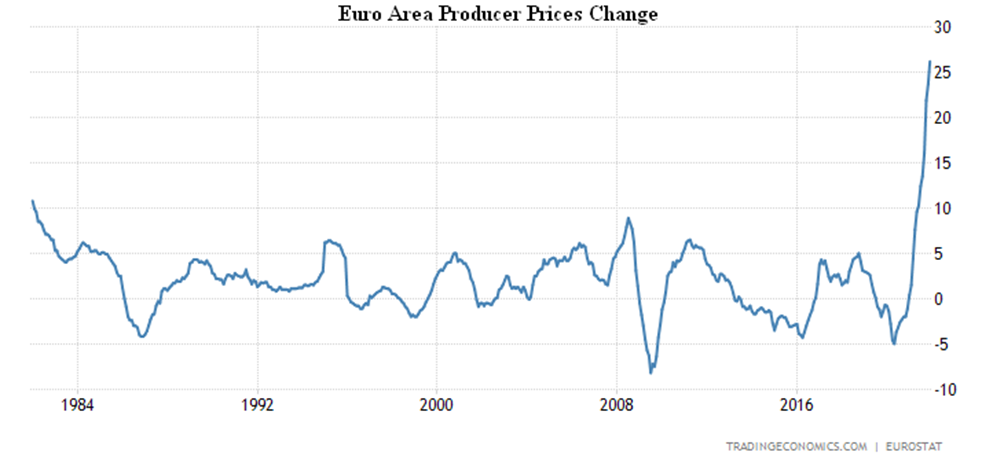

PPI of the Euro Area +26.2% per year, this is an unprecedented rate for all 40 years of statistics:

There is no doubt that the reasons for this inflation rate are structural (as in the US), so that the European Union’s consumer inflation rate will be roughly the same as that of the US (indeed, at least 12-15%). The question is whether the 20-25% rise in industrial inflation, as has been the case for many months in the US, will stop or will continue. It depends on whether the European Central Bank makes the decision (bad or worst) to tighten monetary policy or to continue issuing.

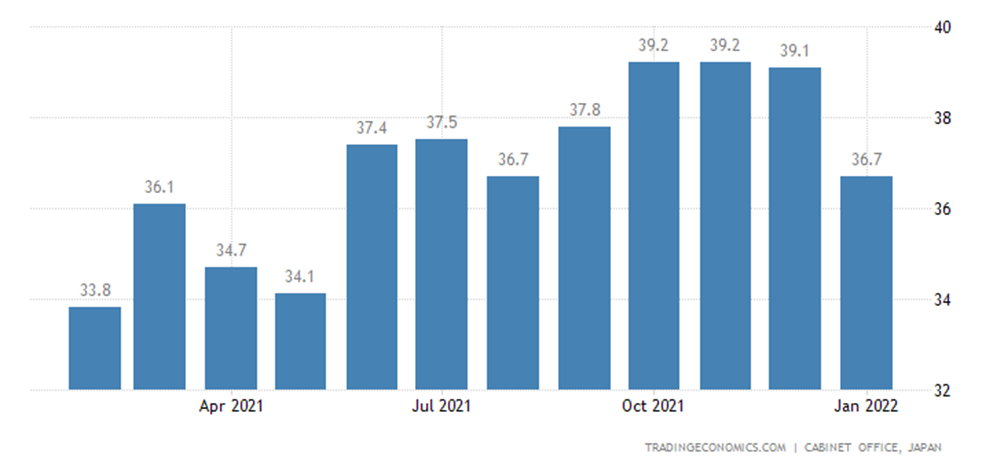

Japanese consumer confidence is the weakest in eight months:

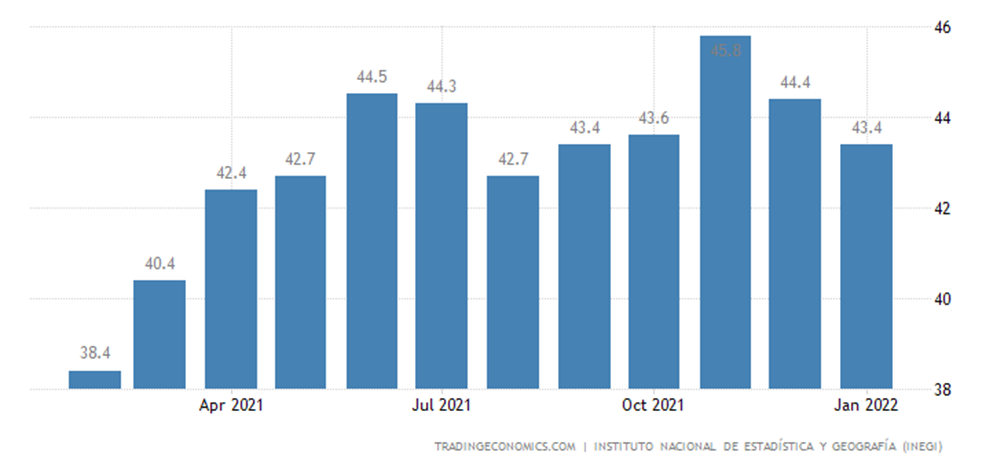

And Mexican consumer confidence is the weakest in five months:

Retail sales in Japan are -1.0% per month:

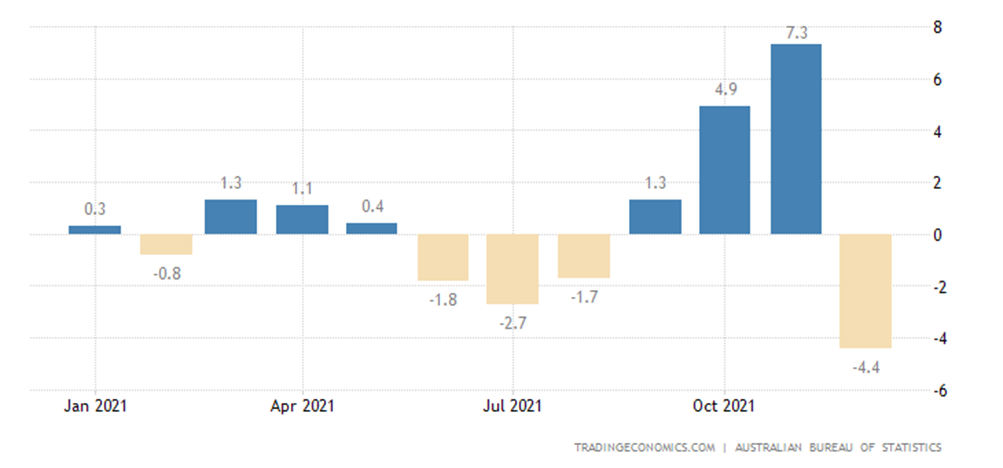

Retail sales Australia are -4.4% per month, the lowest since April 2020:

Retail sales in Germany are -5.5% per month, it’s an 8-month trough:

Retail sales in France are -0.2% per month:

Retail sales in the Euro Area are -3.0% per month, it’s the worst performance since April 2021:

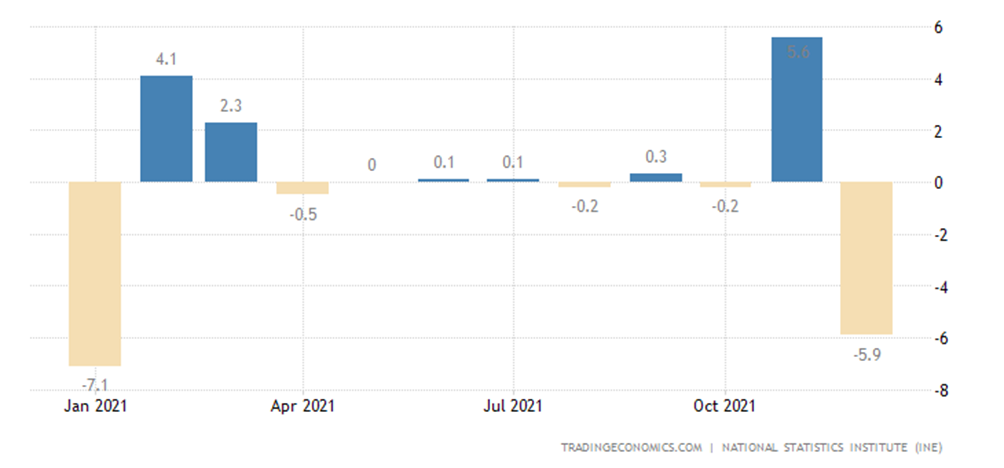

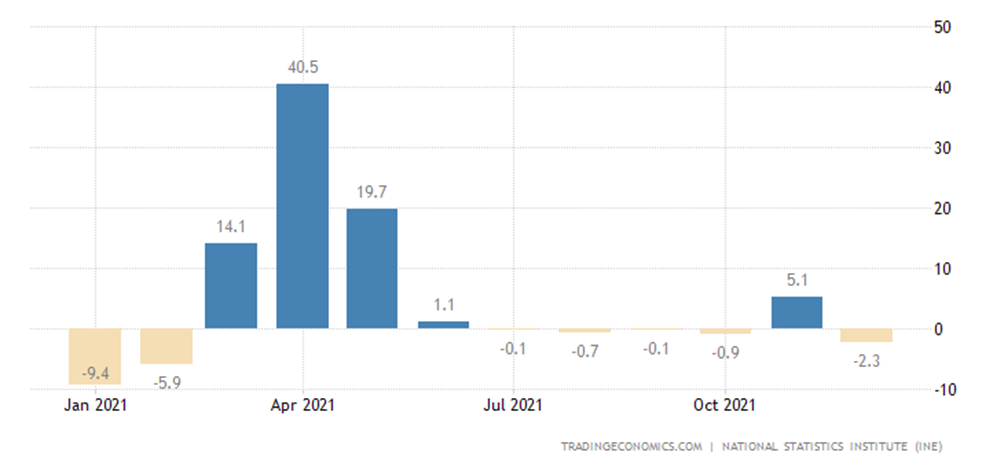

Retail sales in Spain are the weakest in 11 months (-5.9% MoM):

And -2.3% YoY, which is the fifth negative in the last 6 months:

Retail sales figures will soon resemble inflation rates – numerous records have also been set, and if we take into account that these figures are in denominations, given official inflation, not real inflation, then records may be even more stunning. And of course, with these numbers, showing economic growth means disrespecting the readers.

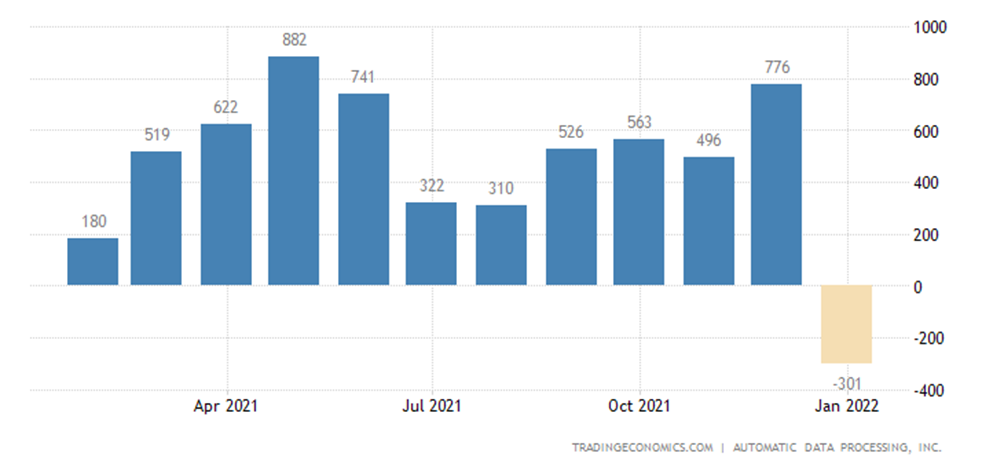

Private sector jobs in the United States have suddenly fallen by 301 000, it’s the worst performance since April 2020:

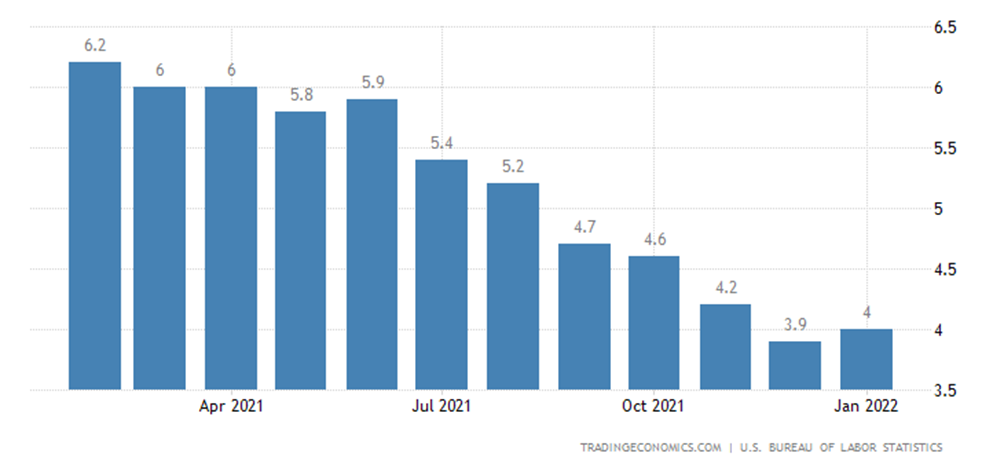

Unemployment has also risen in the United States:

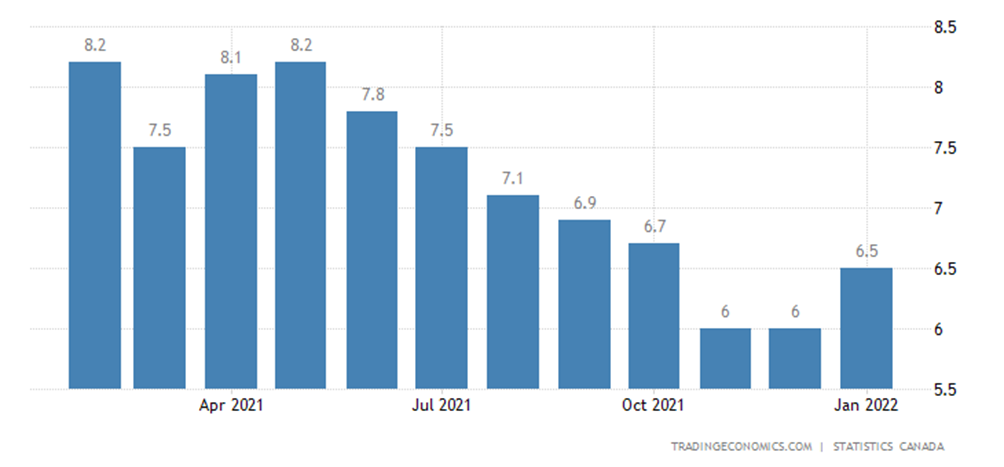

And in Canada:

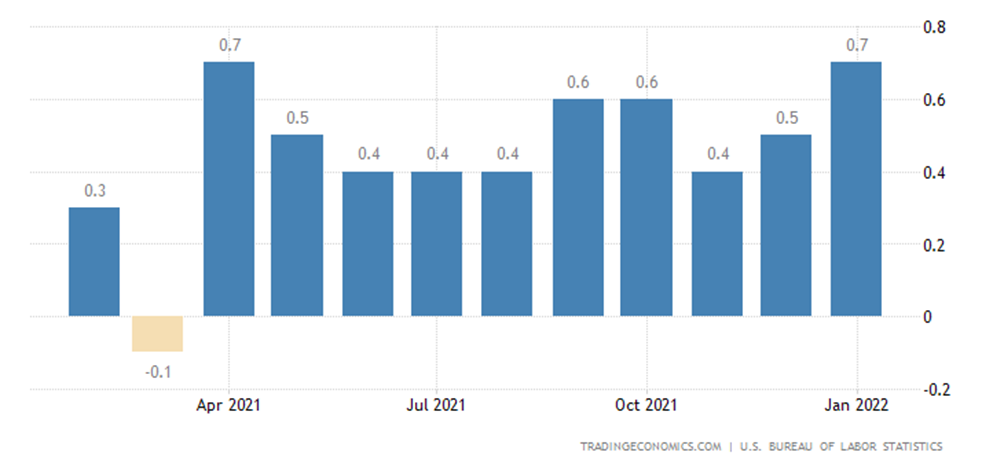

The increase in the average hourly earnings in the US was +0.7% per month, this is a 13-month high:

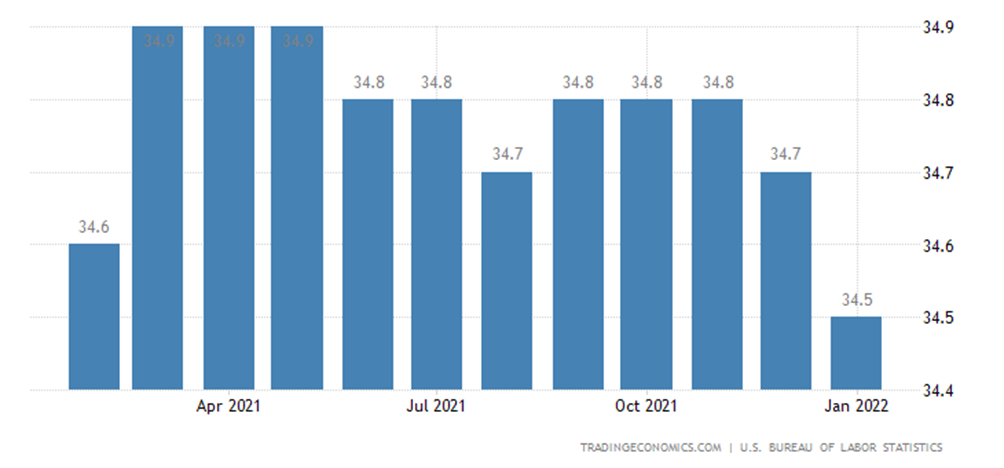

And average weekly hours are at their lowest since April 2020:

Note that the latter figure is completely out of step with the high official figures for GDP in the United States: with economic growth, the length of the working week increases. Thus, labor statistics indirectly support our almost obvious hypothesis that inflation is significantly underestimated.

The Bank of England hiked the rate by 0.25% to 0.50%, with 5 out of 9 board members voting for the raise by 0.50%; further tightening was promised; the CB is beginning to cut its balance.

The Brazilian central bank raised the rate by 1.50% to 10.75%.

The Australian Central Bank left the rate unchanged, but finished the asset-purchase program. The ECB did not change the interest rate, did not stop buying assets and made it clear that it would not raise rates anytime soon. In other words, the answer to the EU’s inflation dilemma is that it will grow.

Summary. The labor statistics presented above provide an indirect estimate of the extent of under-inflation in the United States. Since the steady decrease in the working week indicates a fairly steady decline, and official figures for the fourth quarter of 2021 show about 7% growth (I remind you, this is an estimate, so you should not be too critical of the accuracy of the figures), the underestimation of inflation can be estimated at 8% – 10%. And, rather, on the upper edge. Of course, this is a GDP deflator, but the same estimate applies to consumer inflation, even if the difference is reduced to 5-8%. Taking the official data on consumer inflation at about 6-7%, we have the very interval of 12-15% that we wrote about at the beginning of this Review.

However, all the other indicators of the American economy cited in the Survey suggest a fairly steady decline. Thus, it is safe to say that the US monetary authorities have been actively downgrading inflation for at least six months. In fact, all last year, but this is also a value judgment – there is no objective evidence, and the proxies are more contradictory than in recent months.

The political reasons for this are understandable – the Biden administration, which came to power in mid-January 2021, is in no hurry to sign off on its complete economic failure, but the gist of it does not change. The structural crisis has come into its own, as we wrote a year ago, and now it won’t back down. But if the ECB opted for high inflation, which would reduce living standards in the EU without major collapses, the situation is different in the US.

There in November of this year are meaningful elections and political confrontations on an order of magnitude stronger than in any EU country where political elites are reliably scoured. For this reason, Powell announced a fight against inflation, but given the data on the acceleration of the downturn, it is possible that he will take back his words. And if not, he could have a massive financial meltdown by the end of spring.

We cannot yet clearly answer the question of the Fed scenario, because the choice – whether to tighten or continue monetary easing – will be in the political, not the economic sphere. But if the rate is not raised, this means that “Biden’s team” has signed the surrender on internal fronts. External fronts are a little more complicated.

We hope our readers have a good week at work!