Time period: 25 September – 1 October 2021

Top news story. The main news has been multiple energy-related challenges, from China to the UK. These include disconnections, shortages, and price increases. In line with our model of crisis, this is a perfectly natural phenomenon: since the post-crisis structure of the economy will be very different from the current one, spontaneous structural changes are beginning to occur. Somewhere, there’s more resources than we need, and somewhere there’s less. Additional resources, which, on the one hand, are simply not available, and, on the other hand, need to be concentrated and properly used, are needed to solve the “overload” and to replace the deficit.

All of this makes markets very nervous – with the exception of Friday, markets have been falling all week – increases the cost of insurance, and other problems are getting worse. Avoiding all these processes, even simply stopping them, is most likely not possible, because the main (to say the only) resource for this operation – emissions – is no longer working. As a result, these problems will be exacerbated in all industries, regions and companies.

Macroeconomics

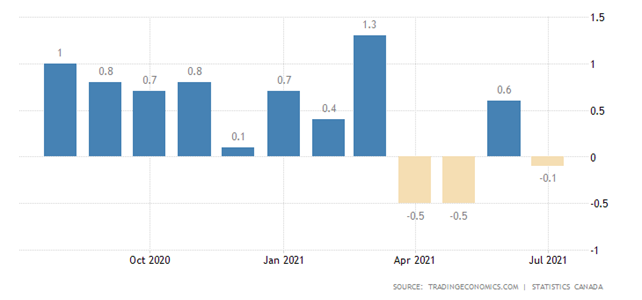

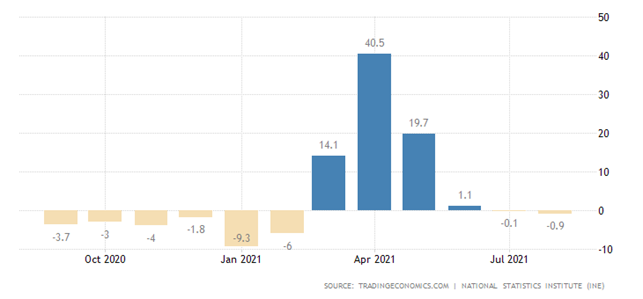

Canada’s GDP is down three months in the last four months:

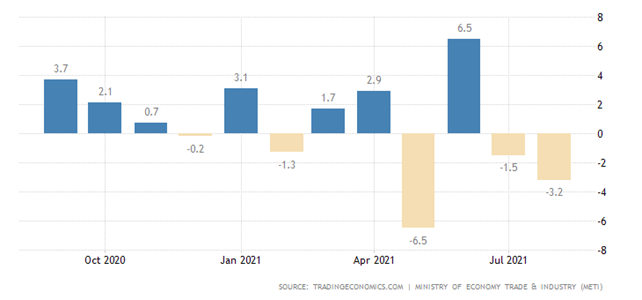

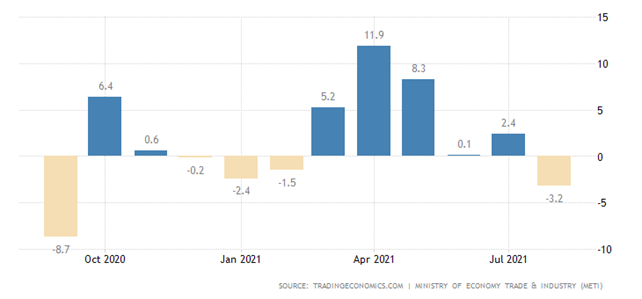

Industrial production of Japan -3.2% per month, 2nd negative in a row:

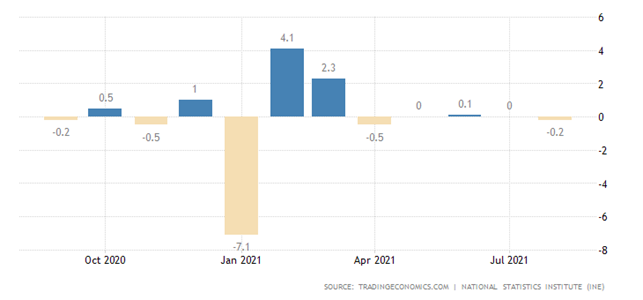

It also went down monthly in South Korea (-0.7%):

Let us remind that if we take into account the real value of inflation, which the authorities tend to underestimate, the picture becomes even worse.

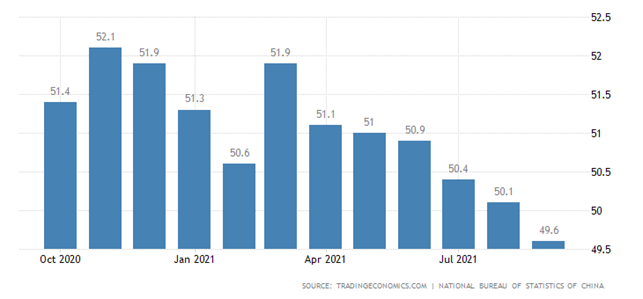

The PMI (Purchasing Managers’ Index, which measures the state of the industry; its value below 50 signifies stagnation and decline) of the PRC industry is officially in recession (49.6 points) for the first time since February 2020:

Another study shows a boundary value of 50.0 points:

It should be noted that since the key indicator for any industry is the volume of sales, and it also depends on inflation – the more the price increase is reduced, the more sales are obtained – even in this case, the real situation is probably to differ from the indicators for the worse.

PMI of the Euro Area industry is at the trough in 7 months:

Same in Britain:

Thus, the main question arises: If real inflation were used, would experts remain equally optimistic (i.e., they would not have omitted the index below 50)?

United States Dallas Fed Manufacturing Index is at its lowest in 14 months:

Chicago PMI weakest in 7 months:

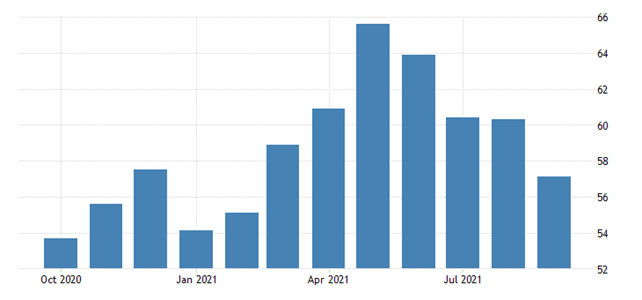

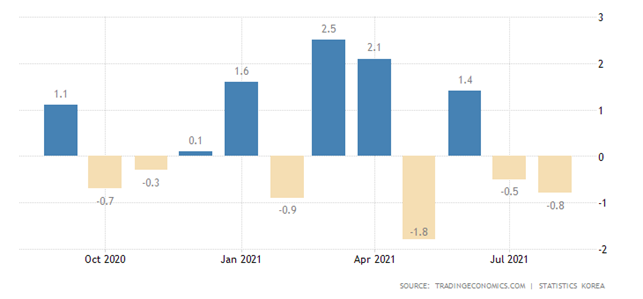

Business confidence in South Korea is weakest in six months:

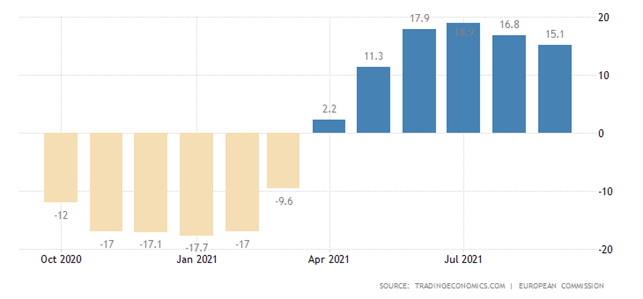

The Euro Area service sentiment is the worst in four months:

The following is a wealth of inflation data.

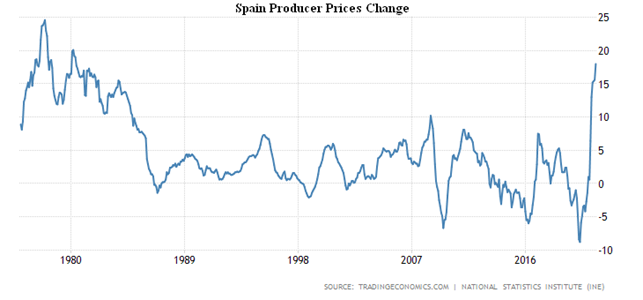

Spanish PPI (Producer Price Index) +18.0% per year, the highest since 1980:

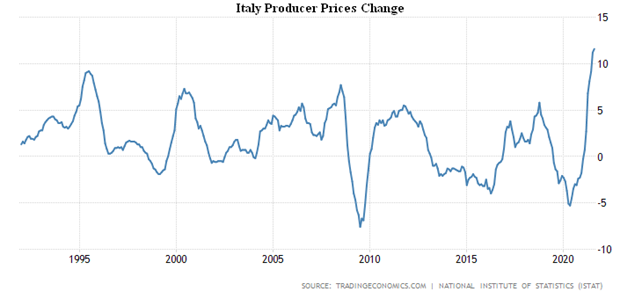

PPI of Italy +11.6% per year, a record for 30 years of observation:

PPI of France + 10.0% per year, this is the peak for 21 years of observations:

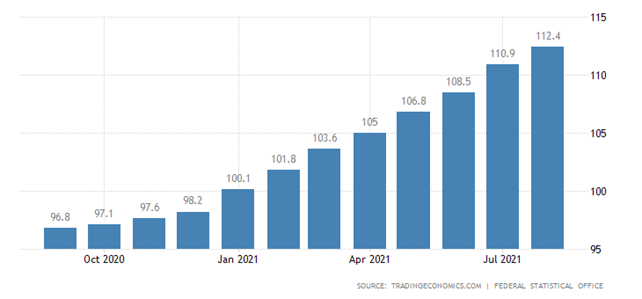

Import prices in Germany +16.5% per year, the highest since 1981:

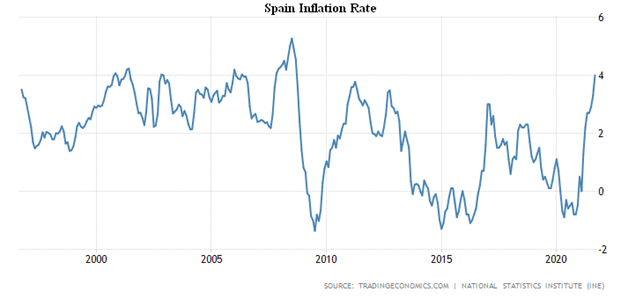

CPI (Consumer Price Index) of Spain +4.0% per year, this is the peak since 2008:

Let us note that if the PPI (Producer Price Index) is higher than the CPI (Consumer Price Index), this leads to either an increase in the latter or a decline in GDP.

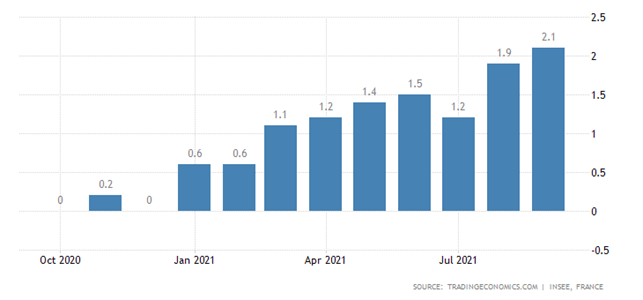

CPI of France +2.1% per year, at its highest since 2018:

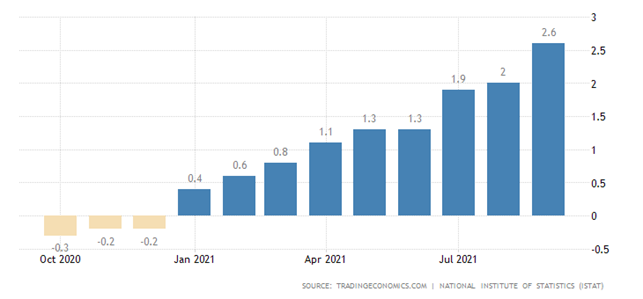

CPI of Italy +2.6% per year, maximum since 2012:

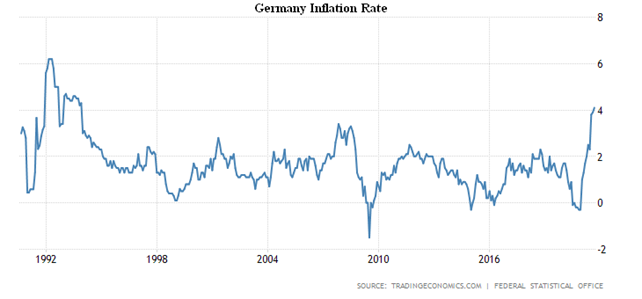

CPI in Germany +4.1% per annum, peak since 1993:

The Euro Area CPI +3.4% per year, is at its peak since 2008:

Without energy, food, alcohol and tobacco, +1.9% is right next to the 2008 high:

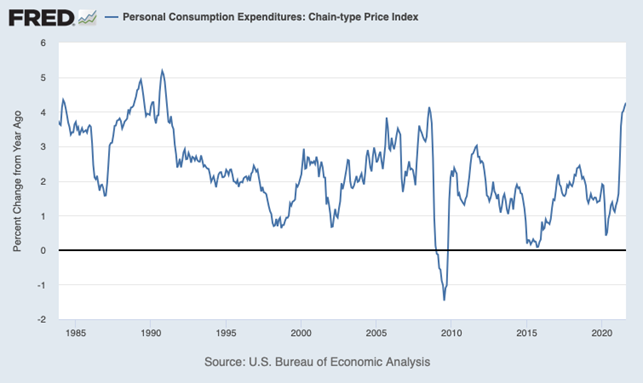

Personal consumer expenditures (Chain-Type Price Index) in the US +4.3% per year, this is the peak since 1991:

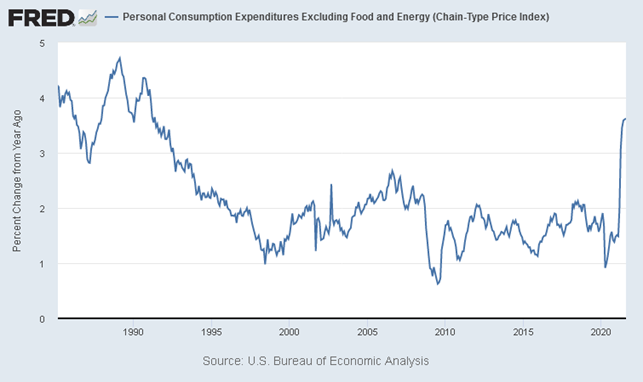

Excluding food and energy (Chain-Type Price Index) +3.6%, this is also the top since 1991:

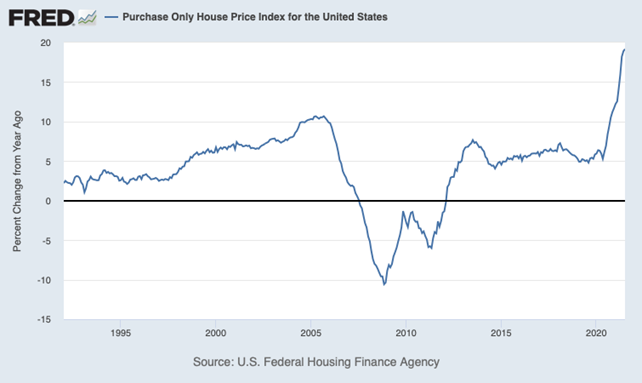

According to official data, US housing prices (Purchase Only House Price Index) are 19.2% per year, a record in 30 years:

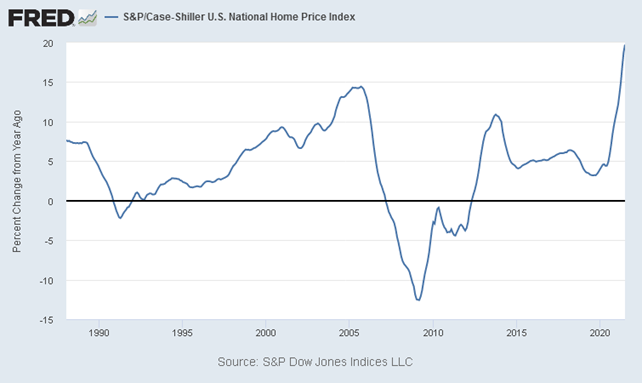

Similar pattern in S&P/CoreLogic/Case-Shiller (S&P Case-Shiller US National Home Price Index): +19.7% per year:

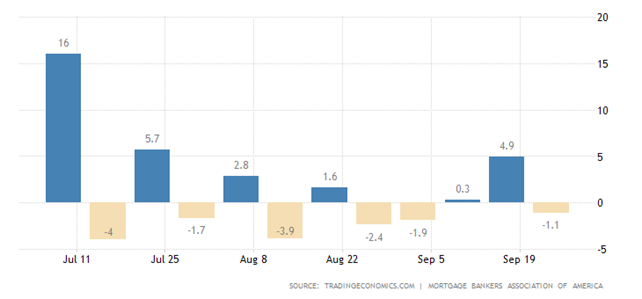

Mortgage applications reverted to a week-long negative once the credit rate was only slightly raised:

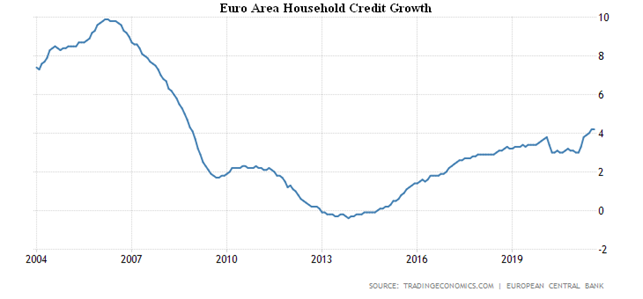

The Euro Area household lending is 4.2% per year, the highest since 2008:

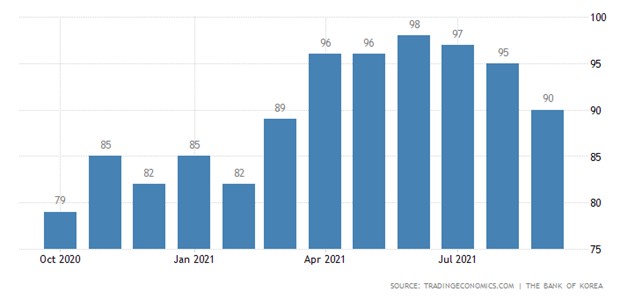

According to the Conference Board, the market sentiment of the Americans is the worst in 7 months, 109.7 against the projected 114.5 and the previous value of 115.2.

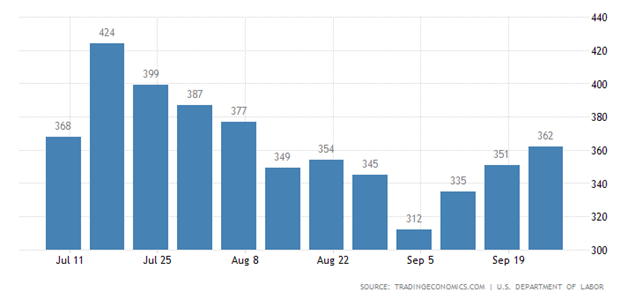

Initial jobless claims in the United States came out at a 2-month peak:

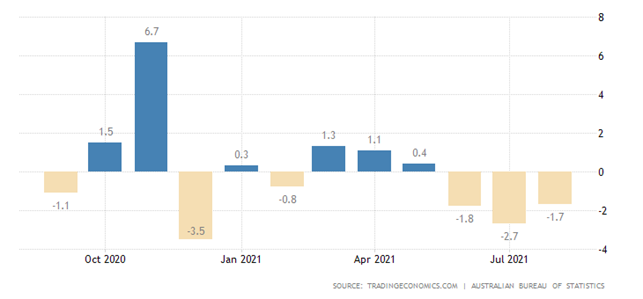

In retail sales in Australia, the third consecutive monthly negative:

That’s when the annual trend went down: for all 38 years of observation, it was only once – in April 2020:

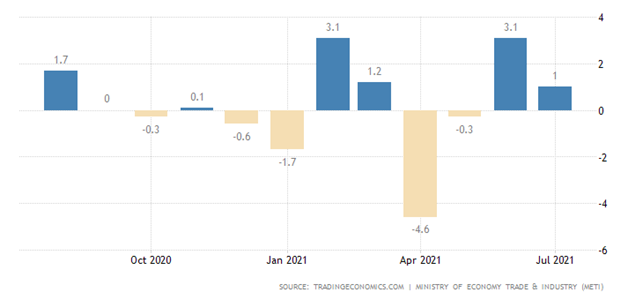

The same is true in Japan: -4.1% per month:

And -3.2% per year (annual lowest value):

Retail sales in Spain -0.2% per month. In the last five months growth (and then only +0.1%) has been observed only once:

As a result, the annual performance is also negative:

Retail in South Korea -0.8% per month, this is the second negative in a row:

The Mexican Central Bank raised rates by 0.25% to 4.75%.

Summary. In a way, a normal week. There have been no major failures or positive economic developments, except for the structural problems mentioned in the first section of this Review. But the past week has been marked by a lot of political problems (worsening in Transcaucasia and Kosovo, Turkish President Erdoğan’s visit to Russia, worsening in Syria etc), but this is not formally economic. Let us note that the purely propaganda political campaign related to the “default” of the United States had nothing to do with economic realities.

Overall, it can be observed that established trends (rising inflation, declining business and production activity, GDP problems) continue to pick up growth. Indeed, they have become sustainable. The structural problems that are clearly exacerbating these tendencies will become deeper. It cannot be excluded that, with the passage of time, political problems may sooner or later have a direct impact on the economy, but so far this has not been the case.

We wish our readers a pleasant autumn weather and a successful work week!