Period: 26 December 2020 – 01 January 2021

Main event: The main event is, of course, the beginning of the new year! Happy holiday! Christmas is not so clearly linked directly to the start of a new cycle, so it is the new year that is the main one. In this review, I will provide a short description of the past year and a brief forecast for 2021.

From the point of view of our theory of crisis (detailed in the book «Reminiscences about the Future», Russian version, English version) the meaning of events of the last year is quite easy to interpret. These distortions are primarily related to the mismatch between the real income of households with a normal economic cycle and their real expenditures.

Since any economic system seeks equilibrium, and in this case we are in full agreement with liberal theory, to maintain and even deepen these imbalances, it was necessary to have a resource that was taken up at the expense of emissions, both monetary and credit, based on monetary easing. Until 2008, despite a series of crises (1987, 2001, 2007), the system was evolving, but since the interest rate had actually gone to zero, its effectiveness has plummeted.

From 2008 to 2020, it was already talked about preventing a rapid, «explosive» return of the economic system to an equilibrium state. In fact, in recent years, the task has been strictly to maintain the situation, the real GDP of most countries did not grow at that time, capital was not reproduced. And the main question was when the recession would start and according to which scenario (controlled or «explosive») the situation would develop. The COWID-19 pandemic was the very part of the firing mechanism that triggered the downturn.

A number of experts are seriously discussing the possibility of a collapse next week. The Eurobonds crash on Friday is not an indicator, because it is linked to Britain’s final exit from the EU. But some stock market indicators have been questioned.

Technicians suspect that the index could break the upper blue line, reach the red level (the absolute maximum), and then fall sharply, breaking through the lower blue line as well. In their opinion, this picture could mean that the stock indices (on the S&P 500 a similar picture) are very close to the historical peak and in the near future the long-term trend will change to a downturn.

The answer to the question of the pace of the downturn is still pending. As our research shows (the report of the Khazin Foundation on the comparison of the «Biden plan» and the «Trump plan»; Russian version, English version) today can be carried out both variants of the crisis: both controlled and «explosive». It is not possible to determine this in economic analysis, and decisions will be made at the political level.

Thus, we entered the year 2021 with the onset of the structural crisis, the specifics of which are described in detail in the above-mentioned book by M. Khazin. This means that the world economy has entered a long-lasting recession, which will be accompanied by a significant reorganization of its sectoral, regional and price structure. The macroeconomic models used by the IMF and large consulting firms to describe these processes are not workable. The Khazin Foundation has developed an alternative set of mathematical models for this purpose.

For this reason, starting this year, the forecasting tools used in recent decades are losing their viability – and this is the main forecast not only for the current, but also for the next years. For these reasons, we propose not only to read our reviews, but also to study other products of the Khazin Foundation based on these alternative models.

Macroeconomics

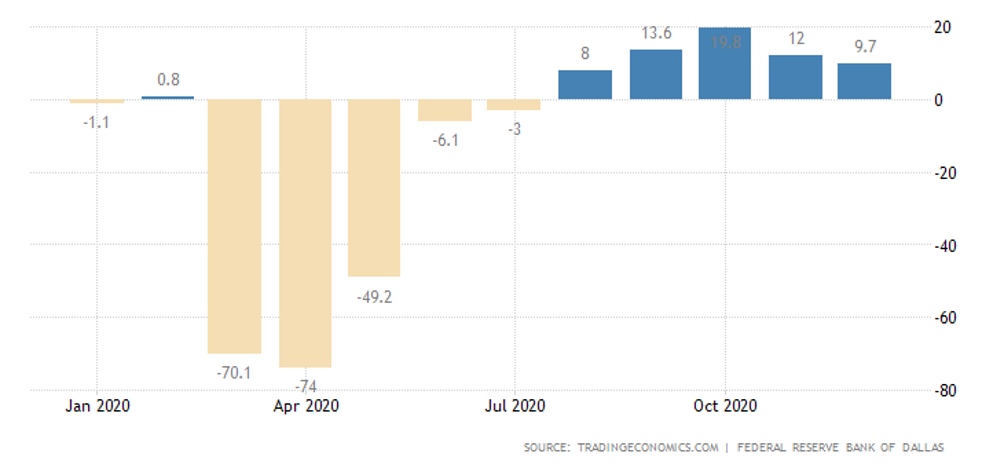

As last week, there’s little data on the holidays. The monthly growth of industrial production in Japan in November went to zero, due to which the annual decline increased from -3,0% to -3,4%. United States Dallas FED Manufacturing Index is the worst in four months, although it has remained in its growth zone. The question is, can this not be the effect of hidden inflation?

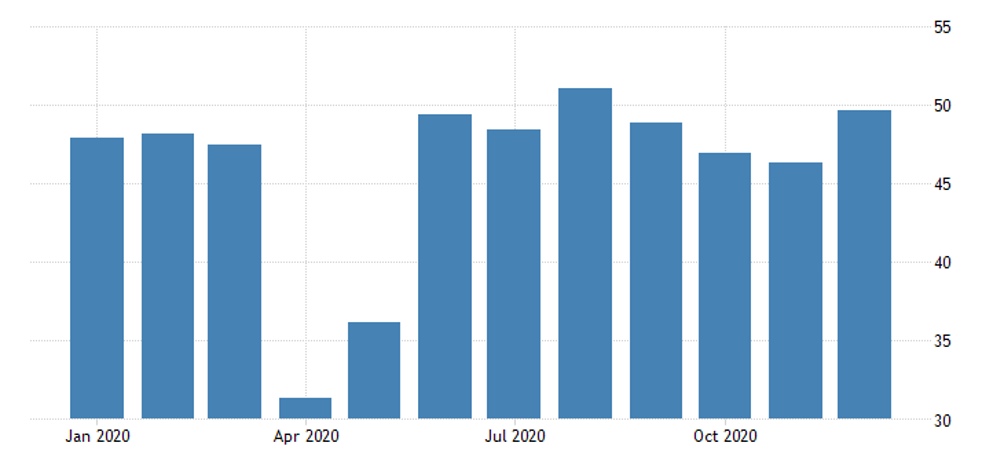

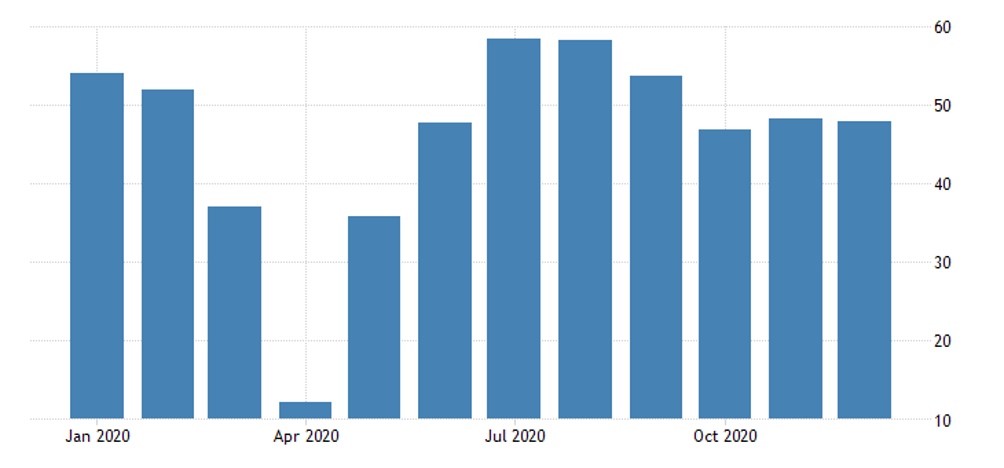

The PMI of production and services of the Russian Federation remains in the zone of recession (let’s remind, this is a specially processed index of expert evaluation of own industries; the index below 50 means a decline):

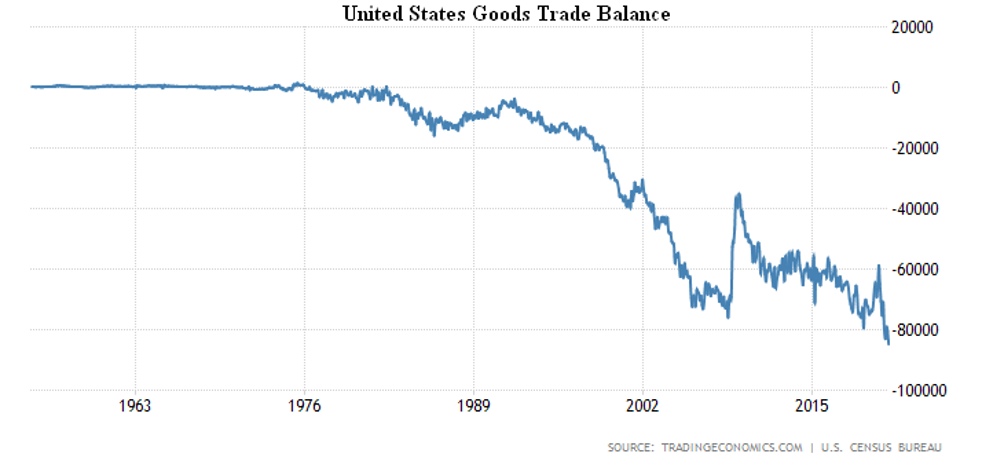

The US foreign trade deficit is a record in 66 years of observation:

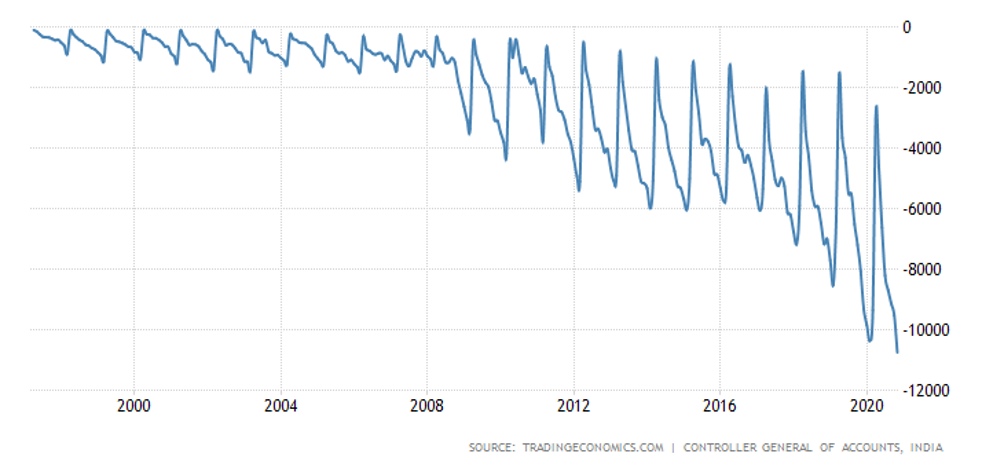

And India has a record budget deficit for 24 years of observation:

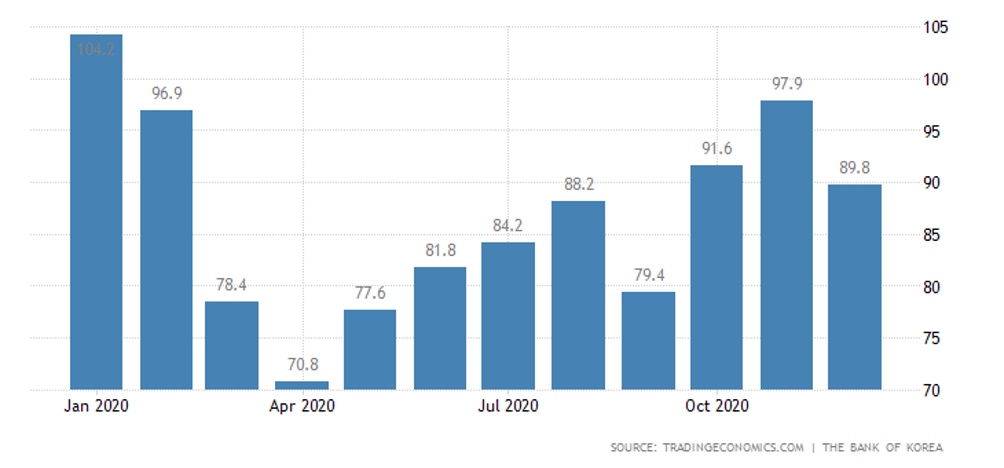

South Korea’s market sentiment deteriorated sharply in December:

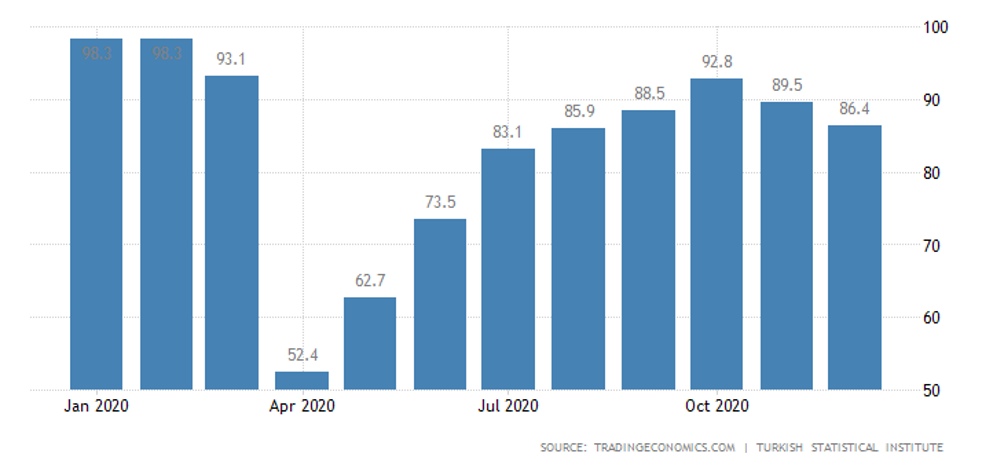

Grim mood also in Turkey:

The official CPI of the Russian Federation, i.e. consumer inflation in December is the highest since May 2019 (+4,9%). Please be reminded that this is a monthly value increased to the annual value (i.e., multiplied by 12). But, as Russia’s devaluation has clearly gone beyond double-digit values, and consumer prices are heavily tied to import prices, there is strong reason to believe that this figure is significantly underestimated by the authorities.

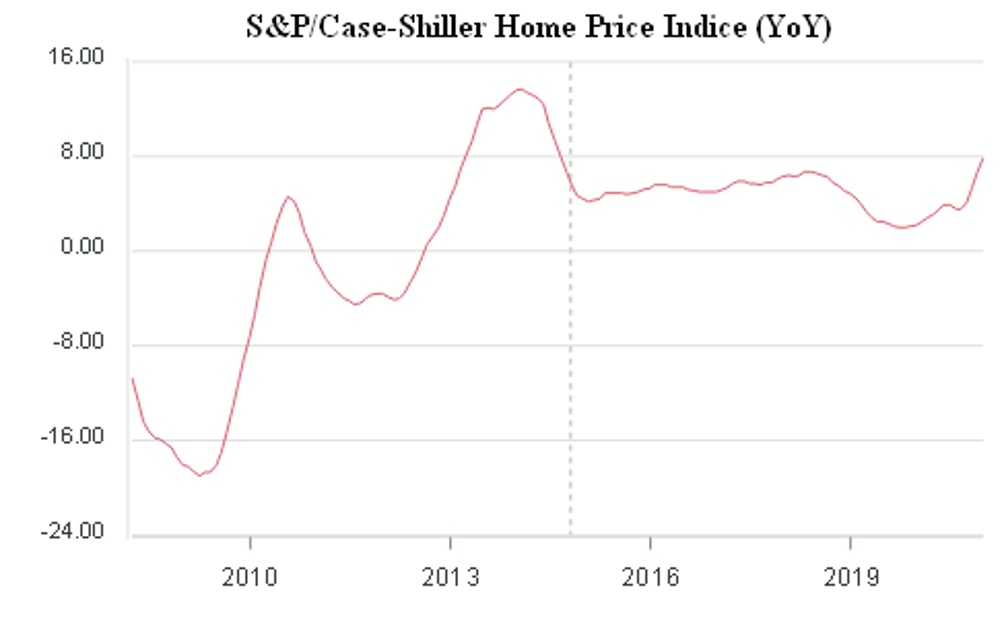

House prices in major US agglomerations increased by 7,9% in October (peaking in June 2014):

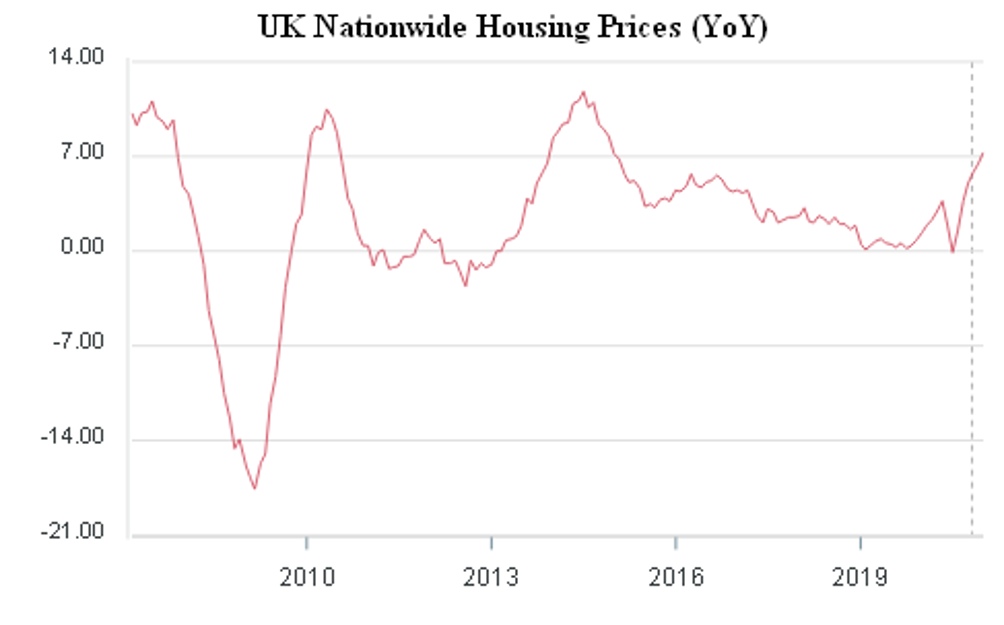

The same pattern in Britain (+7,3%; 6-year high):

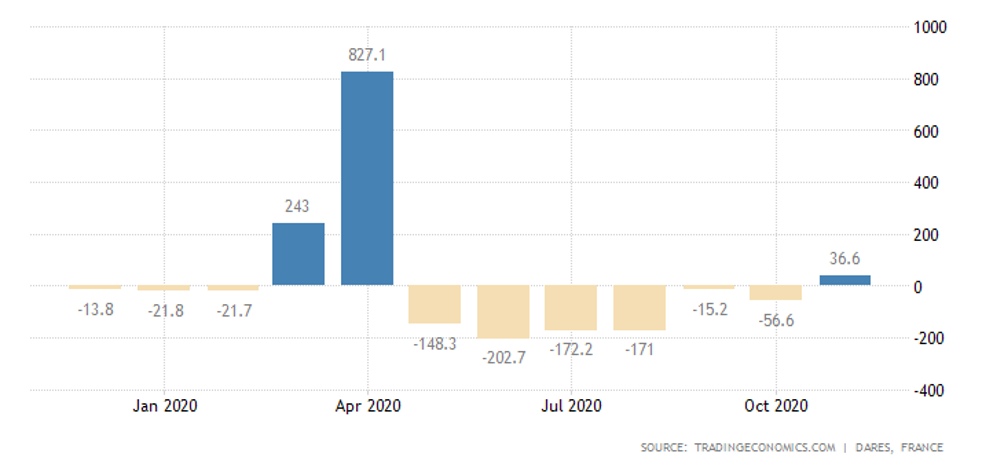

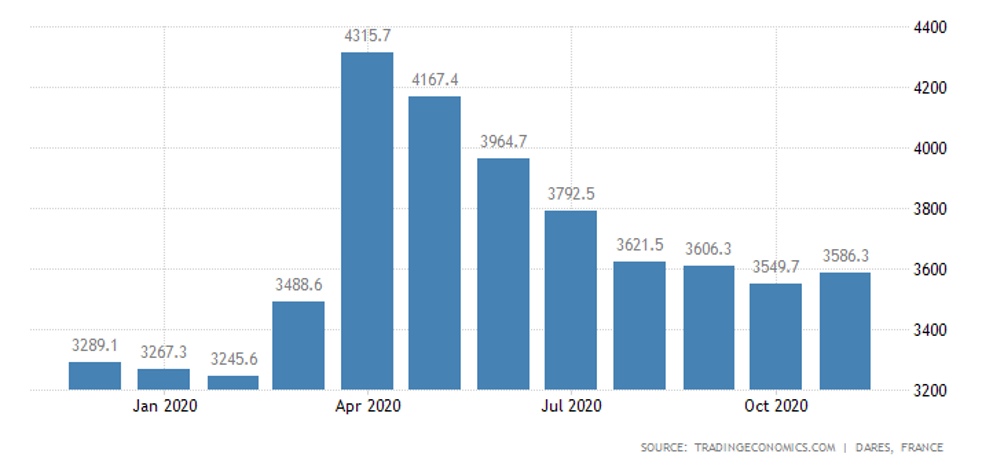

Initial jobless claims in France began to rise in November for the first time in seven months:

As well as the number of unemployed:

The Spanish retail store fell 0.8% a month in November. The annual decline ( -4,3%, and excluding food -6,8%) is the worst in five months.

The situation is similar in South Korea; -1.0% per month and -1.5% per year.

The dollar ended the year at the bottom in three years, a little bit more, and it will drop to the levels of six years ago:

By the way, this adds value to the words of the stock market experts, whose views are presented in the first section of this review.

Summary: There is no deviation from the baseline trends of the last months of 2020. A recession is developing in the world economy, and as is the case with the spontaneous elimination of structural distortions (see «Reminiscences about the Future»), the rate of decline is not increasing, remaining at some stable level. Indeed, the downturn may gain momentum if markets fall, but the rate of downturn in the real world economy will not be significantly affected.