Period: 6 – 12 February 2021

Top news story: The global financial elite has once again begun to convince the public of the beginnings of economic growth:

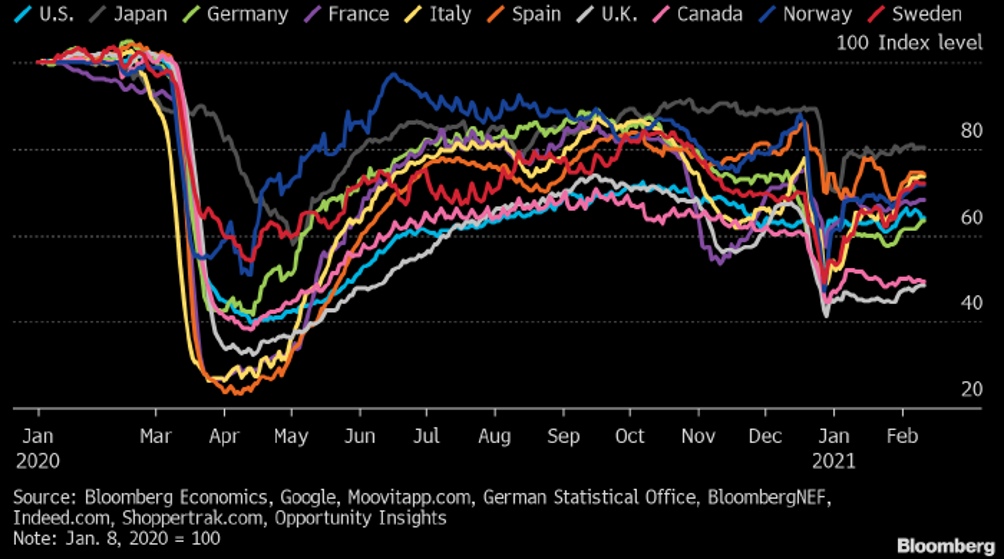

A chart of economic activity in the leading developed countries of the world. It was adopted as a reference point with a value of 100 on an index scale on 8 January 2020. Source: Bloomberg

With Brent crude this week rising to $62.70 per barrel, setting a new 13-month maximum:

and Bitcoin reaching a historical record, it is likely that the growth is not at all a growth. This may simply be the result of an underestimation of inflation. But the very desire to talk about growth is revealing – the world’s financial elite, the stewards of the world economy, realizes that its credibility is increasingly compromised.

The many conversations about changing regulatory methods, introducing digital money and taxing cryptocurrencies can no longer convince anyone, the question is only when economic growth will begin. At the same time, almost no one thinks about the fact that the popularity of digital currencies is due to the fact that traditional currencies are compromised by continuous issuance. But who can guarantee that digital currencies will not be compromised for the same economic reasons that dollars and euros have to be issued?

Surprisingly, the topic of the causes of crises is practically absent from the agenda! This review is one of the rare examples of analytical products in which the analysis of certain economic processes (collectively referred to as the crisis) goes directly to the fundamental, underlying causes. But it is almost impossible to obtain relevant information from open sources.

Macroeconomics

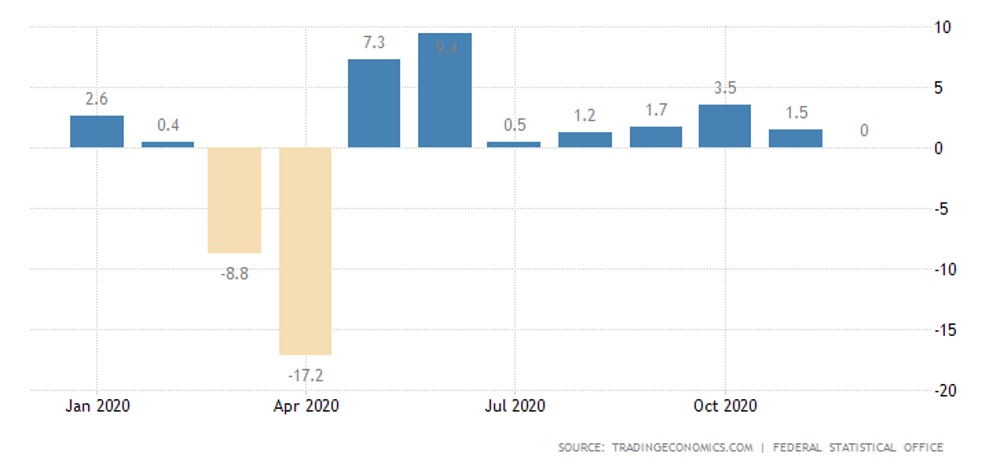

Industrial production in Germany slumped by 8,5% in 2020:

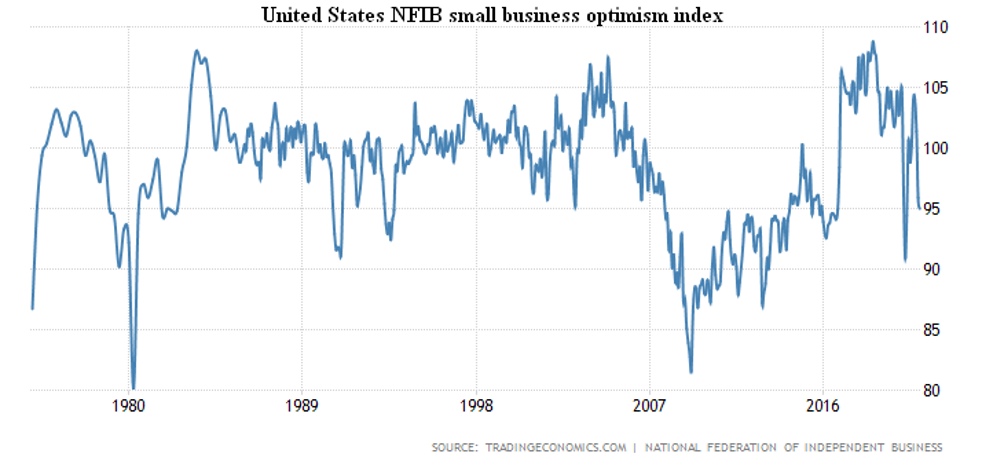

The pessimism of small businesses in the US is close to the peak of quarantine last spring:

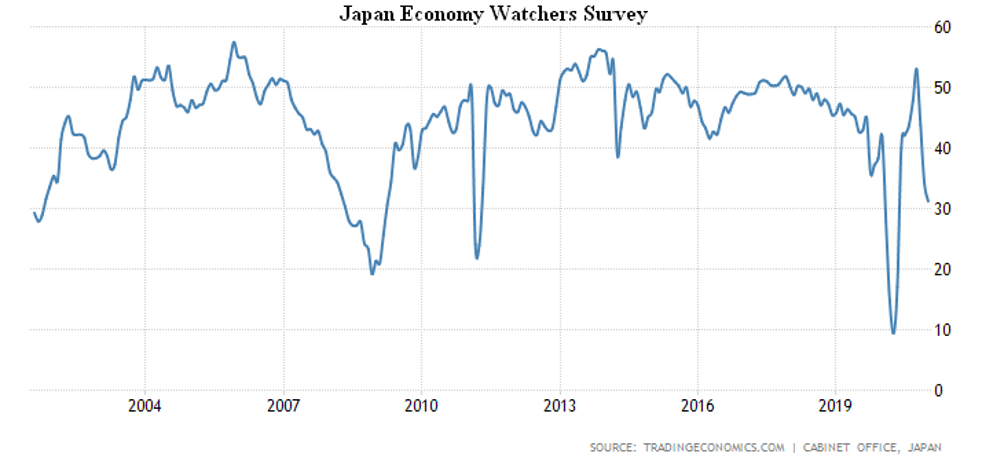

Japan’s Economy Survey index is the worst in 8 months:

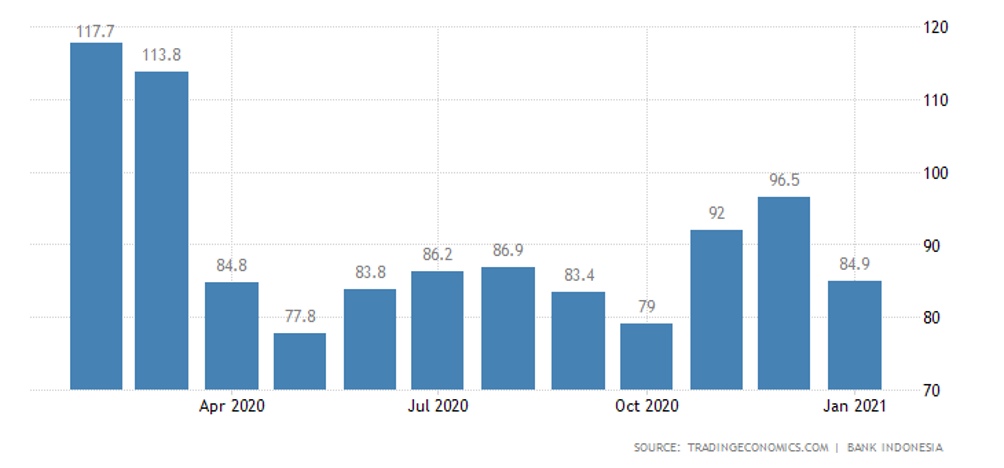

Consumer confidence of Indonesians sharply deteriorated:

And Indonesia retail sales are almost back to the decline of last spring:

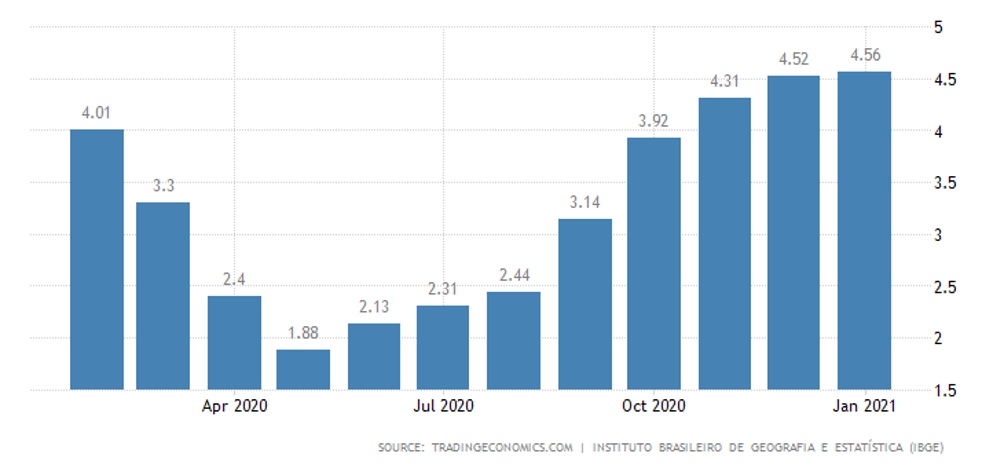

Brazil’s inflation peaked in almost two years:

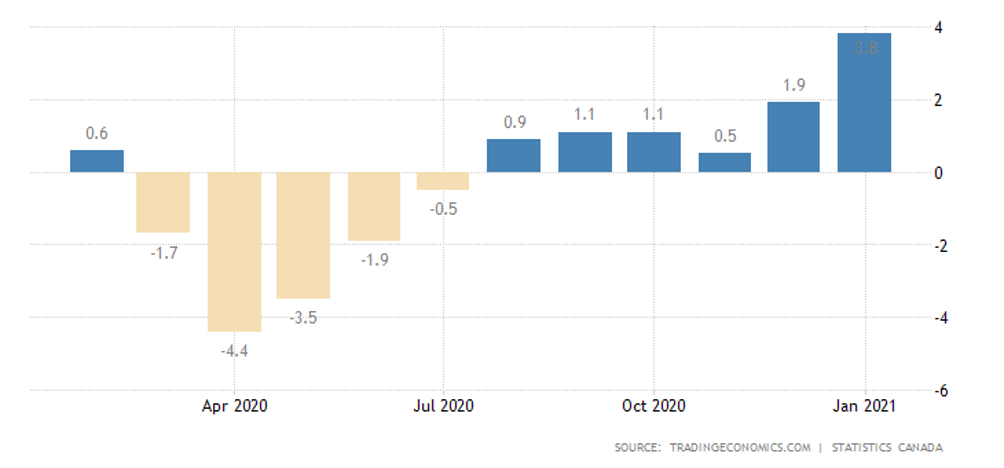

Canada’s PPI (industrial inflation) is the highest since 2018:

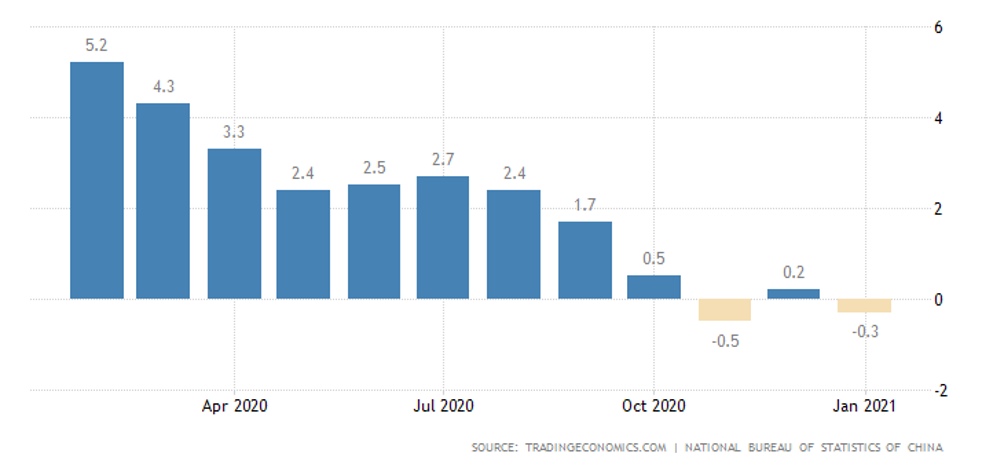

As we noted in the previous review, inflation trends are winning deflationary trends in some countries, and vice versa. They’re both bad symptoms, but they can’t handle a stable situation. In China has now returned to annual losses:

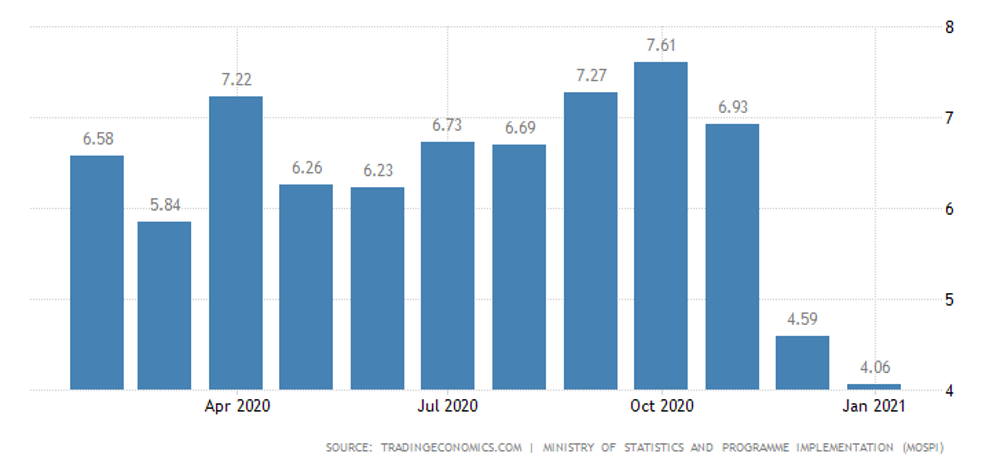

India has the lowest price increase since September:

Inflation forecasts in the US (New York Federal Reserve Survey) have peaked since the summer of 2014 (+3,05%). But core inflation rate in the US is the lowest in seven months (+1,4% per year):

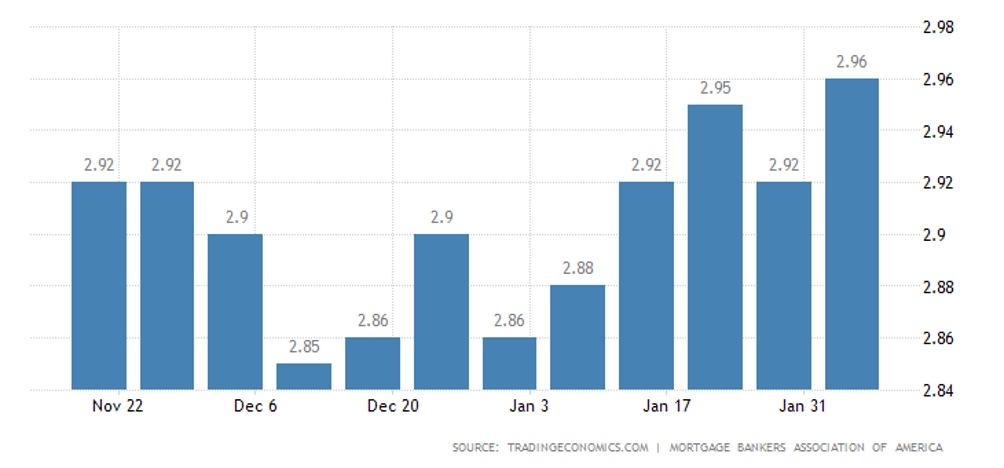

But the US mortgage rate is the highest in three months, so consumer expectations look quite adequate, especially given the forthcoming stimulus measures, which are, in fact, the same emissions:

Unemployment in South Korea has peaked since October 1999:

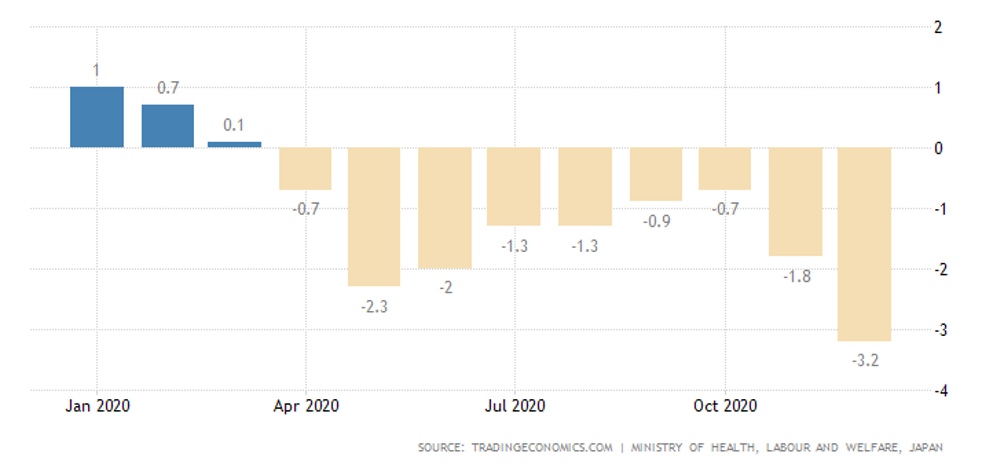

Japanese salaries in December fell at the worst rate since 2009 (-3,2% per year):

The Central Bank of the Russian Federation left interest rate in place, but began to hint at a future tightening of policy whereas the official IMF position is to lower the rate. What is the meaning of this contradiction is yet to be clarified, the Central Bank of the Russian Federation was not previously inclined to so blatantly disregard the opinion of the world’s chief monetary ideologist.

Summary: Given the inflationary trends in many parts of the world, it is clearly premature to speak of economic growth. But there is no denying its existence: the sharp downturn of recent months could trigger a small compensatory growth. This is roughly the same as it was in the summer of 2020, when growth failed to reverse the spring recession. Note that it is premature to draw conclusions about Western Europe (not the EU, because the UK is involved), where harsh quarantine measures continue.

There is no certainty that cause and effect have not changed places here, and such a severe quarantine was imposed precisely because it was necessary to «objectively» justify the failure to fulfill the authorities’ promise of economic growth. The targets of the beginning of last year have not been met and, in general, there is no longer any confidence that they will ever be achieved.

The authorities should not be seen as overstepping and/or being too cynical: the negative effects of mass demonstrations, which are particularly severe in the face of a severe downturn, are even more devastating. Authorities usually choose not between good and bad scenarios, but between bad and worst. But this cannot be explained to voters, and for this reason the desire to appease the ordinary and small and medium-sized business owners for at least a few months seems perfectly natural. This is likely to explain the optimistic projections described in the first section of this review.

Note that this is not the best business option. Misjudging the situation can be very costly, so it is our position that the truth should always be told. The trouble is, few people can afford it.

Good luck next week!