Time period: 5-11 February 2022

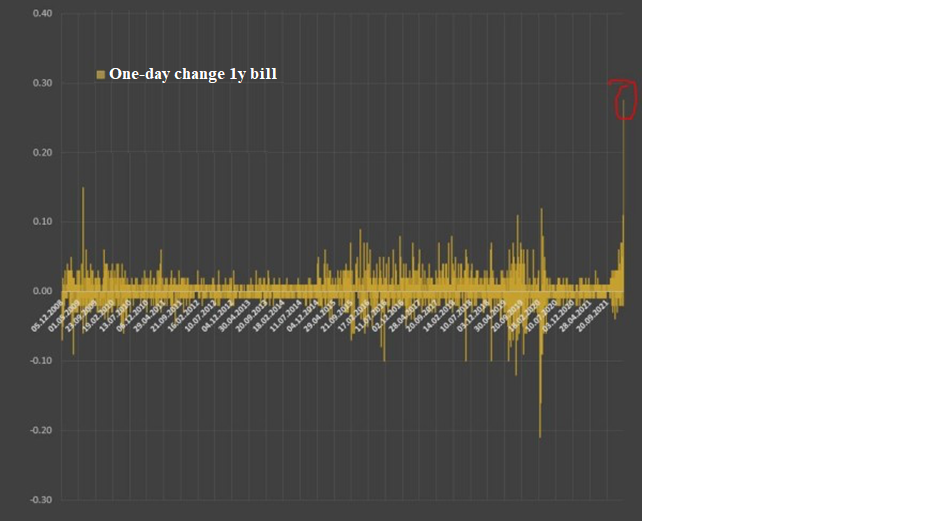

Top news story. Of course, the highlight of the week was the extraordinary meeting of the Fed’s Board of Governors on Monday. The reasons are clear. These are the highest inflation rates in the US (see the following section). Moreover, the troubles began in the U.S. debt market, almost 30 B.P. in one-year promissory notes per day, 15 times more than the average daily volatility of the last 15 years:

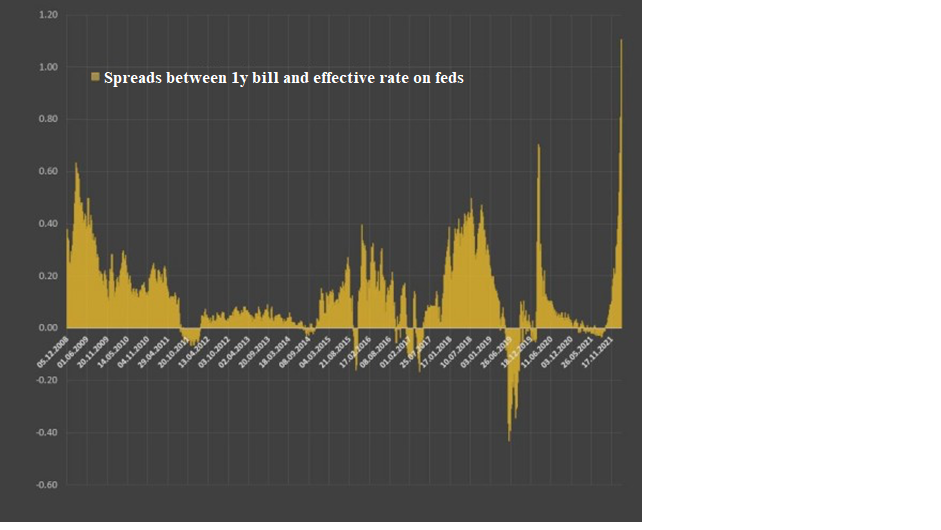

As we can see in the following picture, the spread between the same 1-year yield and the effective federal funds rate has widened dramatically:

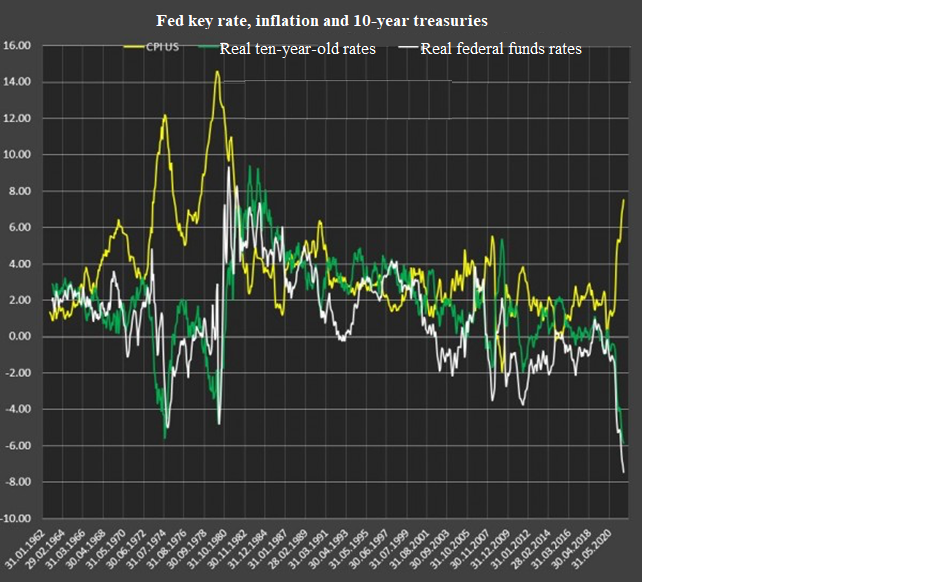

This is not surprising, because the return on debt (and not just on government, but on any debt at all) is significantly lower than real inflation. And inflation, moreover, as we showed in the previous Review, is in fact much higher than the official figures.

So the situation, if we add even official inflation indicators to it, becomes even more amusing:

The graphs presented are taken from Pavel Ryabov’s latest review, where the topic of the debt market is explained in more detail. We are not inclined to draw catastrophic conclusions and make an ambitious statements (which, however, have been used repeatedly in this review), but we must note that there are some reasons for this. And if we add to that the problem of the November election (we don’t even mention Canadian truckers), it’s clear that on Monday we can learn a lot of new and interesting things.

Let us note that we have no inclination to condemn or praise the leadership of the Fed. In our view, as repeatedly noted in the reviews over the last two years, the US has entered a structural crisis, and the question is not whether it is possible to prevent it (no), but what scenario to choose: A rapid decline, with living standards falling by about 50%, or a slower (controlled) but possibly stronger decline.

Actually, in the book “Sunset dollar empire and the end of the ‘Pax Americana'” back in 2003 A. Kobyakov and M. Khazin wrote that if the crisis had been allowed then, its scope would have been approximately equal to the scope of the recession of 1930-32. So a drop in people’s living standards would be about 40%. But the onset of the acute phase of the crisis was postponed – at the cost of deepening it to 50-55%. If it continues to delay, the result will be even more unfortunate.

Macroeconomics

In December, UK GDP -0.2% per month:

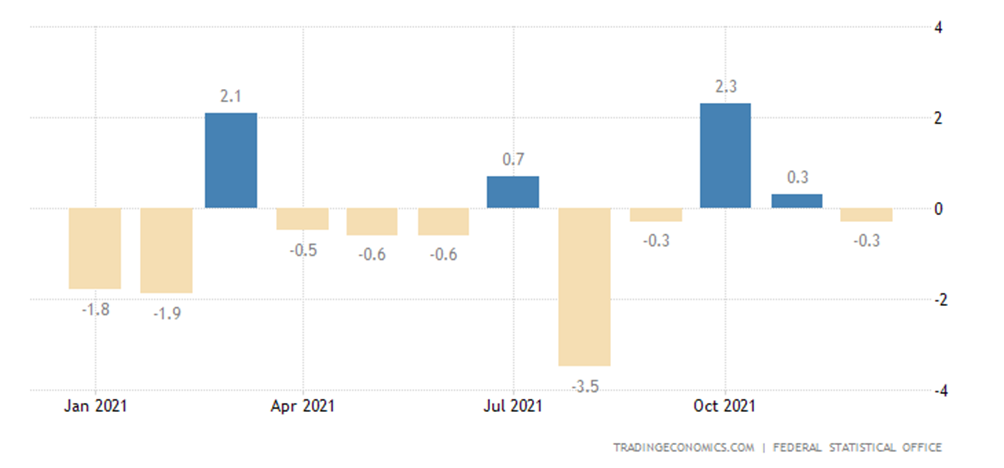

German industrial production -0.3% per month – 8th negative in the last 12 months:

And -4.1% per year, this is the 4th negative in a row and the trough in 10 months:

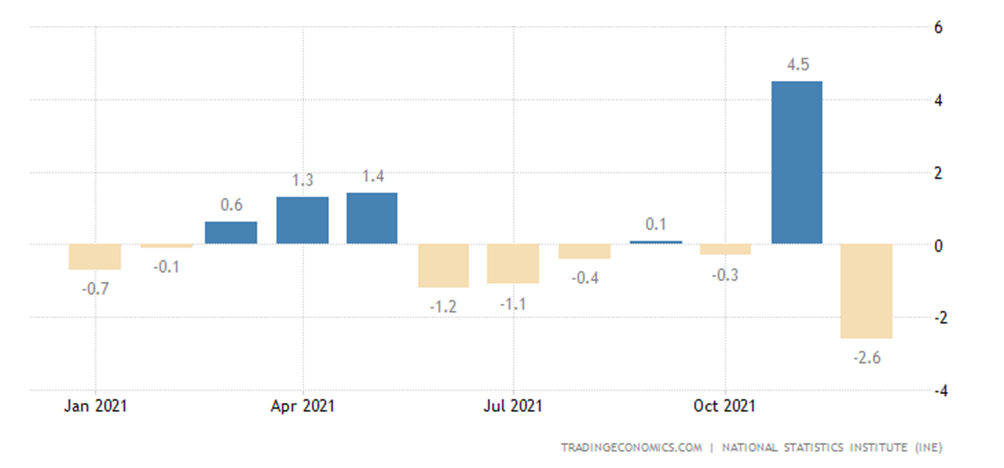

Industrial output in Spain -2.6% per month, which became an anti-record for 20 months:

Once again, we will note that, in reality, the figures will be even worse if we consider inflation fairly. By the way, spikes such as those in Spain’s quarterly indicators often occur when government statisticians begin to change the way they measure inflation.

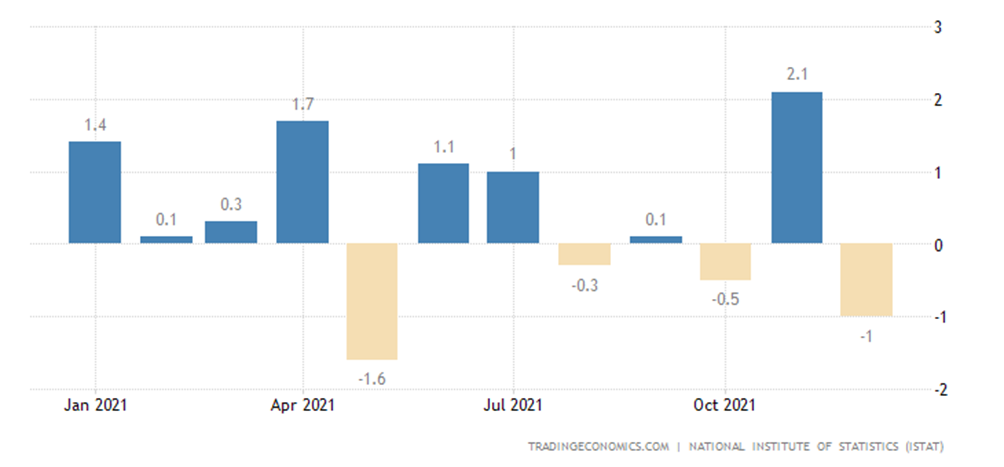

In Italy -1.0% per month:

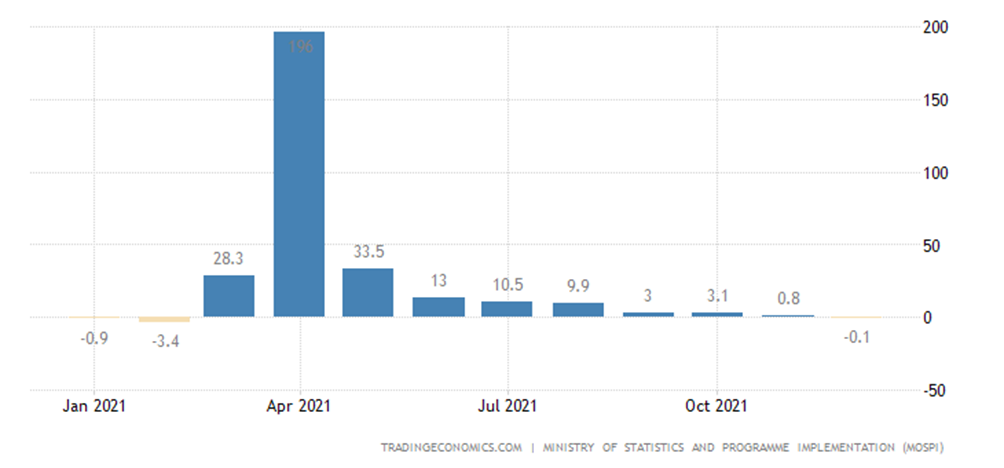

Indian manufacturing output -0.1% per annum – 10-month trough:

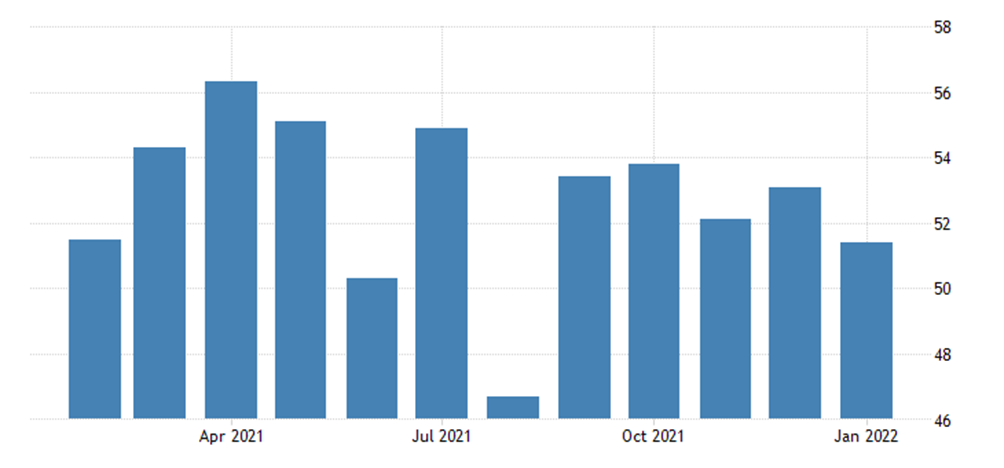

PMI (index, meaning expert assessment of industry conditions; its value below 50 signifies stagnation and decline) China’s service sector 51.4, which is a 5-month low, external demand is weakest in 15 months, employment falls:

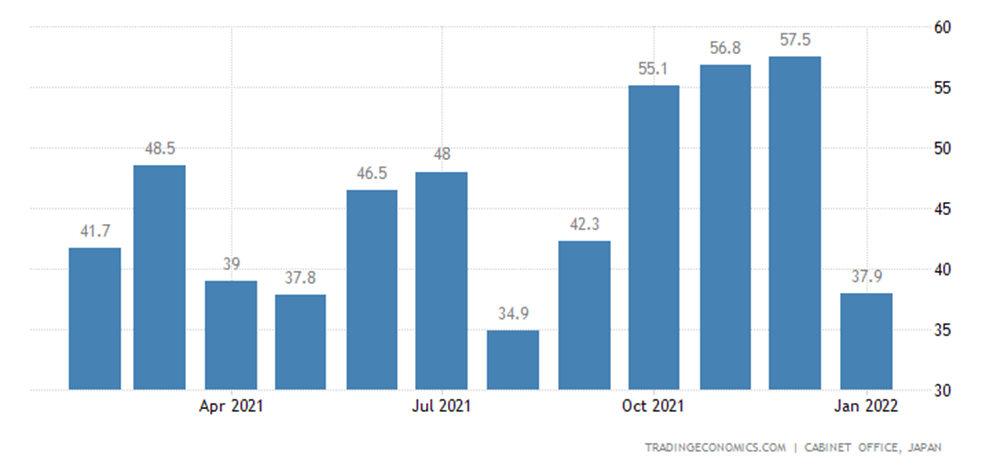

Japan Economy Watchers Survey is at its lowest in 5 months:

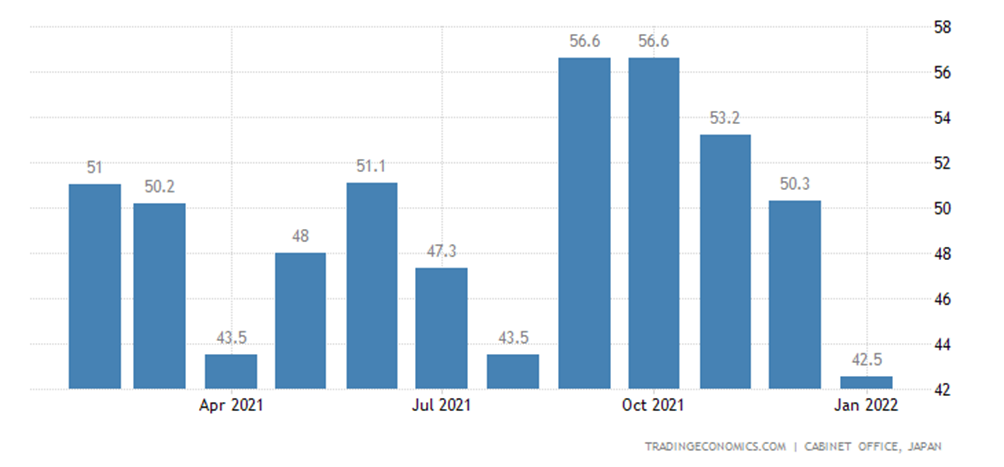

And Japan Economy Watchers Survey Outlook is the lowest for the year:

United States Nfib Business Optimism Index in the USA is on 11 months bottom and below average of multi-year values:

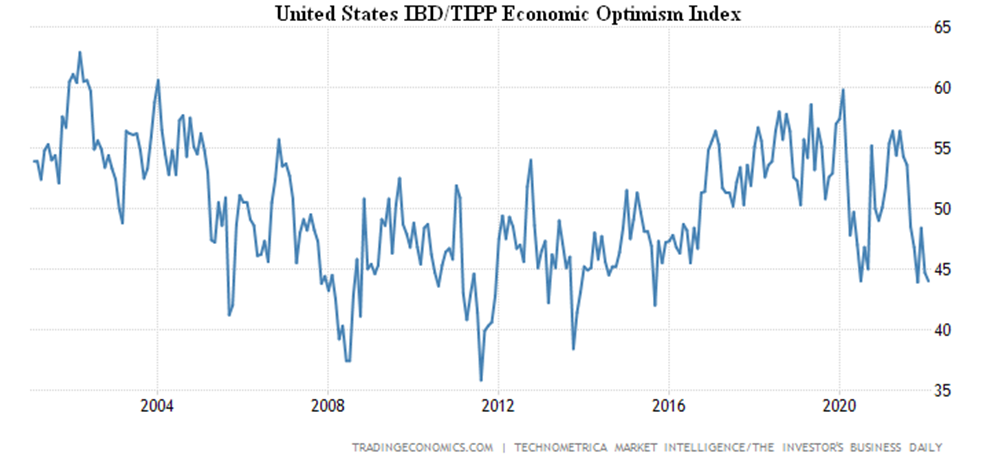

United States IBD/TIPP Economic Optimism Index for the 7th month in a row is in the area of pessimism, and it is only 0.1 point from the trough since 2015:

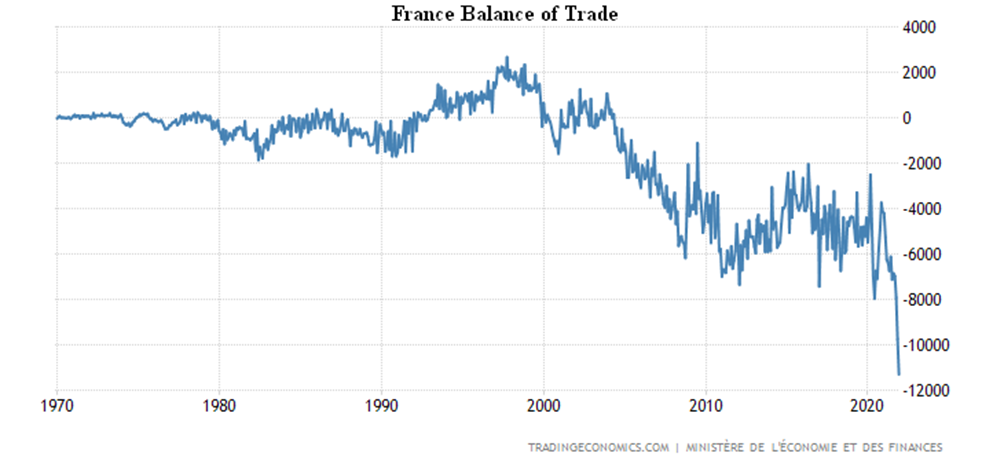

France’s balance of trade is a record one, and by far the opposite of previous peaks:

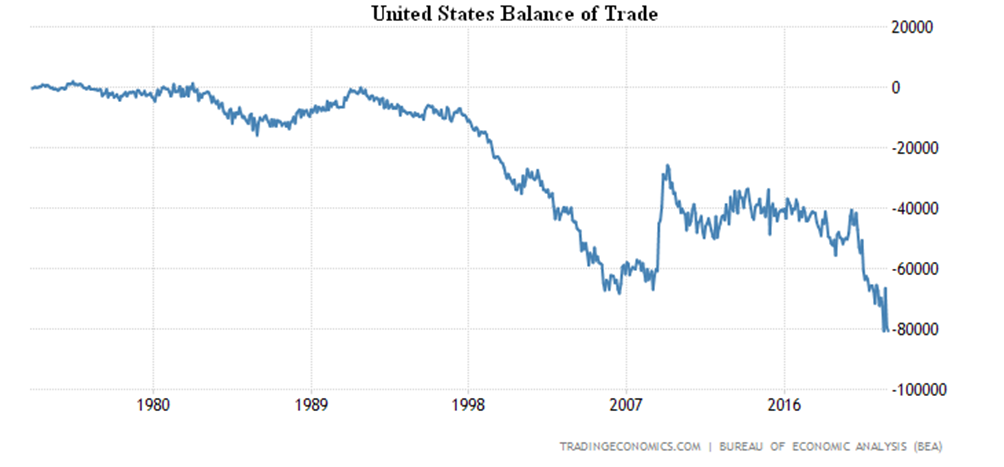

The US balance of trade almost reversed the November peak, with a strong new record overall in 2021:

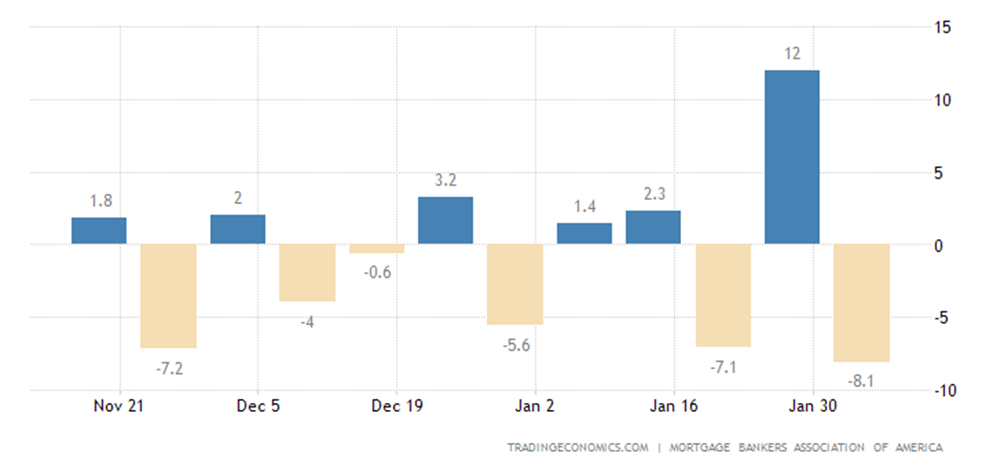

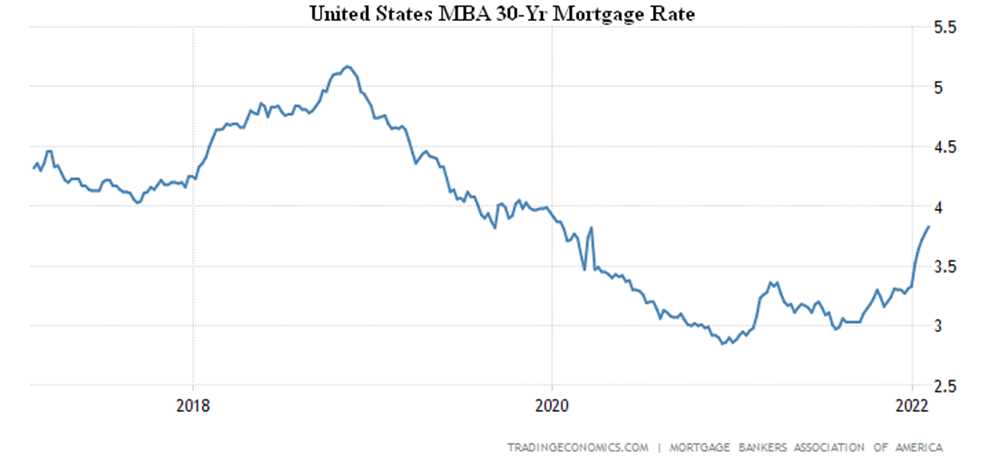

Mortgage applications in the US were -8.1% per week:

Because 30-year fixed-interest rates are at their peak since January 2020:

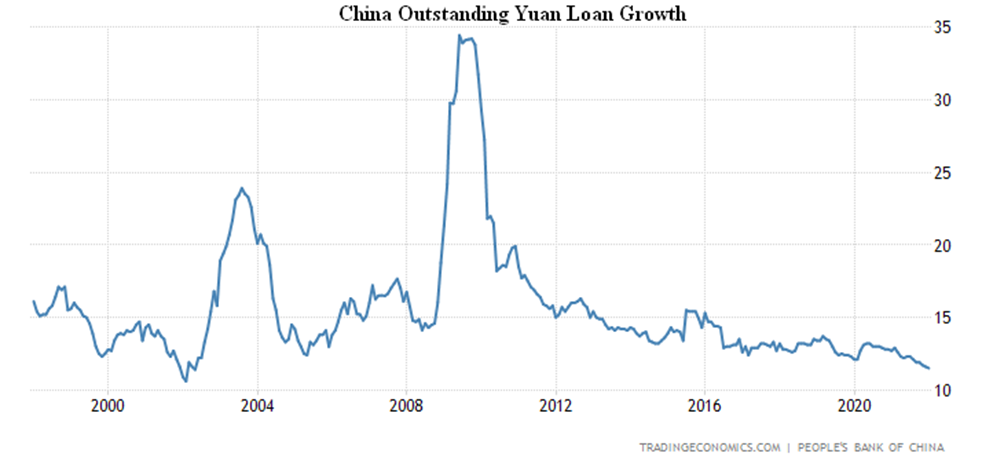

In China, outstanding yuan loan growth was +11.5% per year:

This is followed by inflation rates, which have traditionally broken records in recent months.

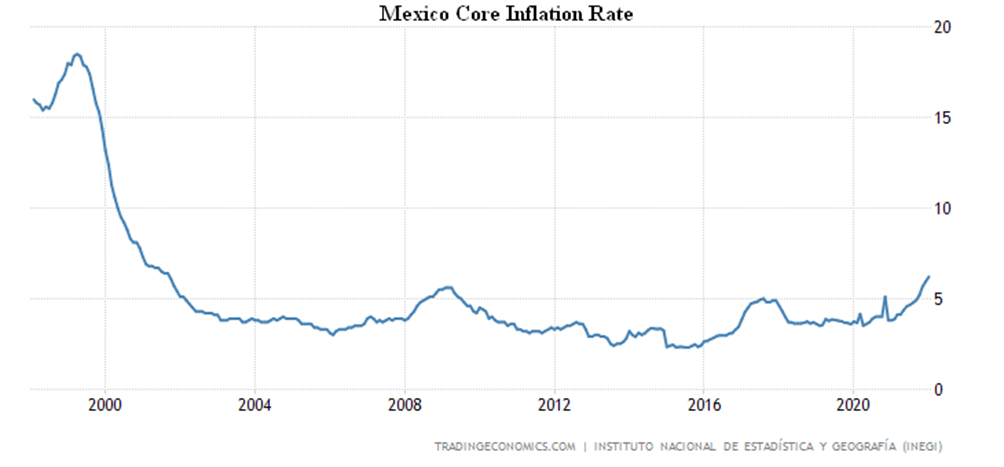

Mexico’s CPI (Consumer Price Index) has slipped slightly from its peaks, but secondary effects have followed – less food and energy set a record since 2001 (+6.2%):

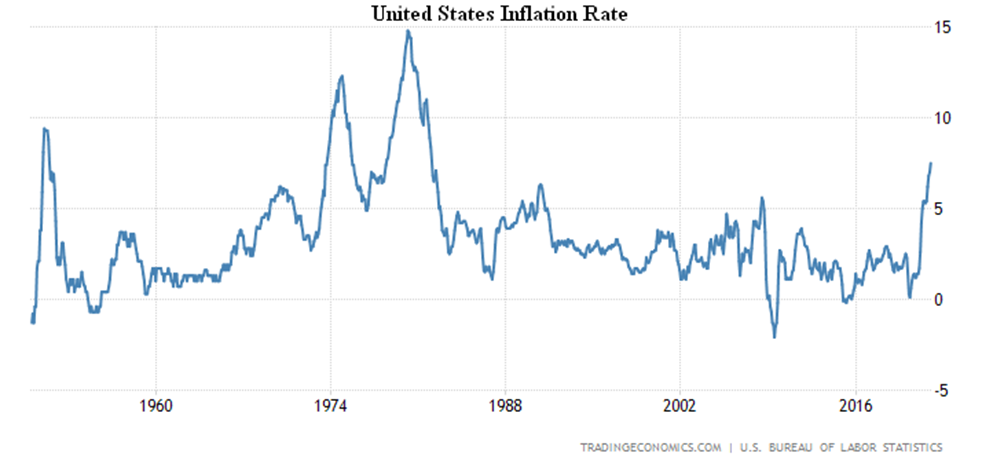

US CPI +7.5% per year – the highest since February 1982:

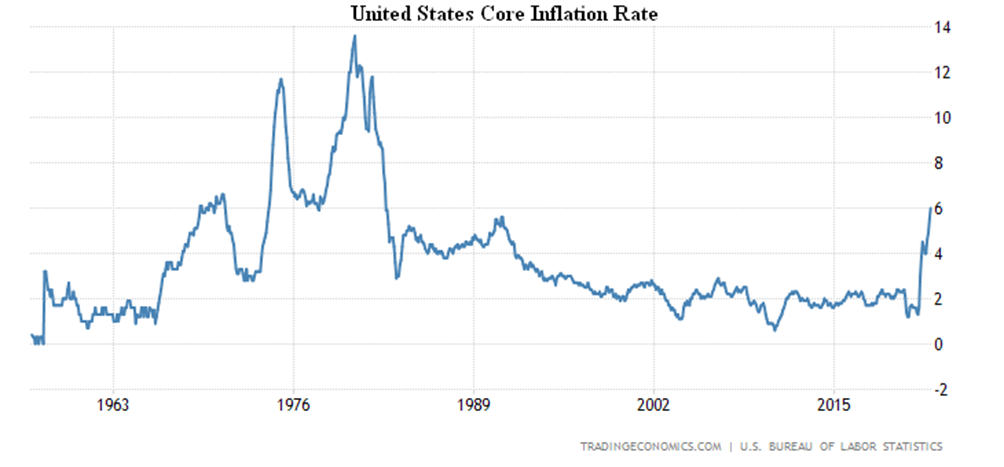

Core inflation rate +6.0%, which is the top since August 1982:

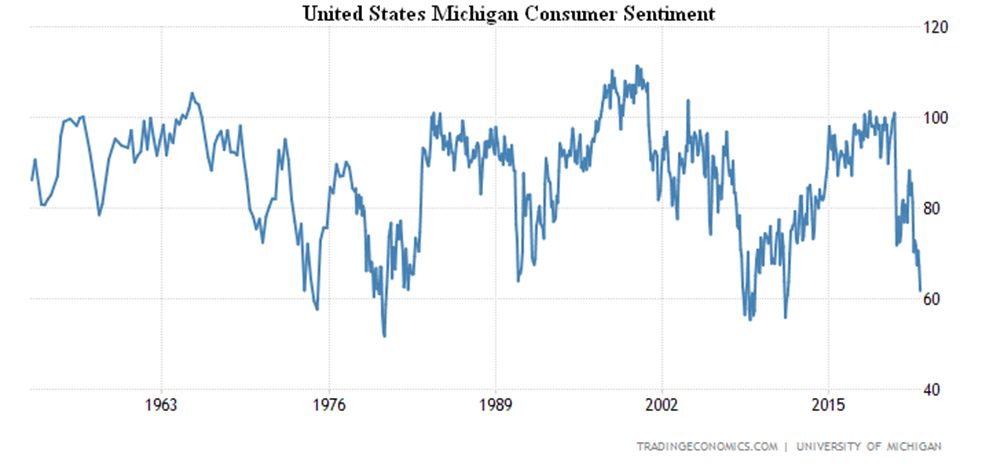

US consumer confidence is at its lowest level since 2011:

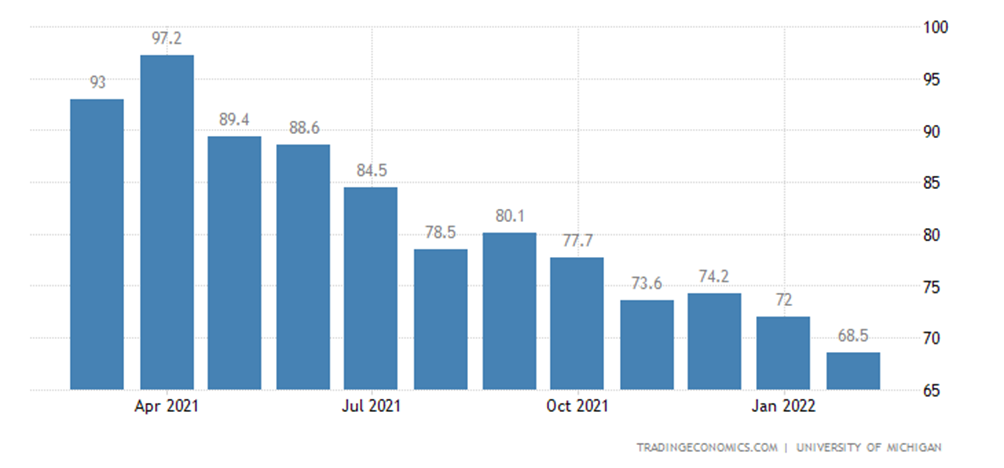

This is equally true of current conditions:

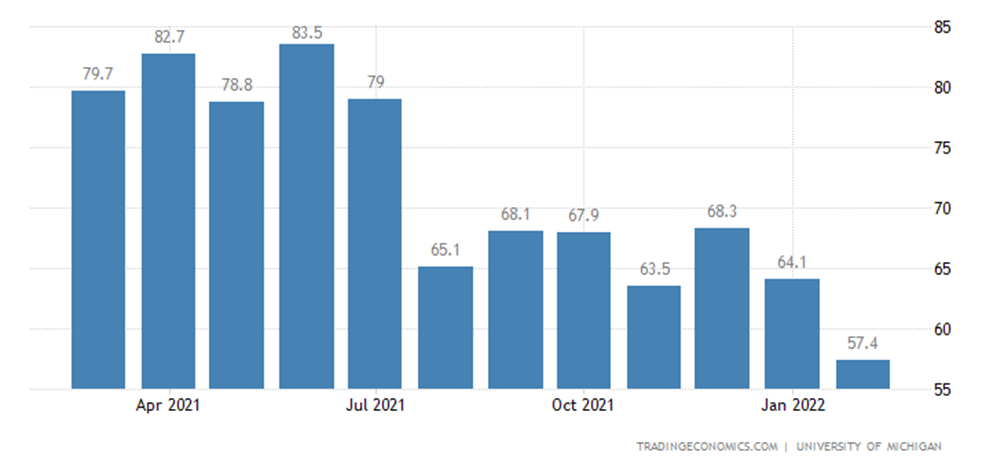

And expectations:

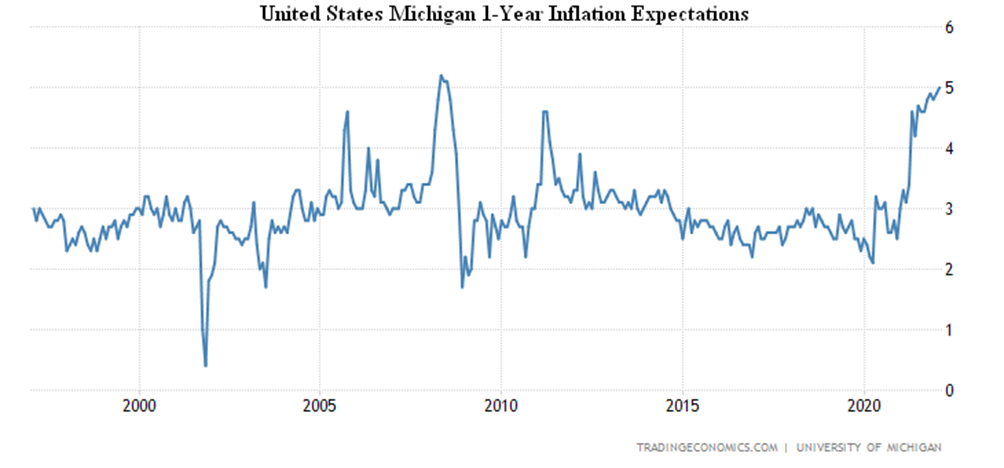

Inflation expectations (+5.0% per year) are close to the top of 2008:

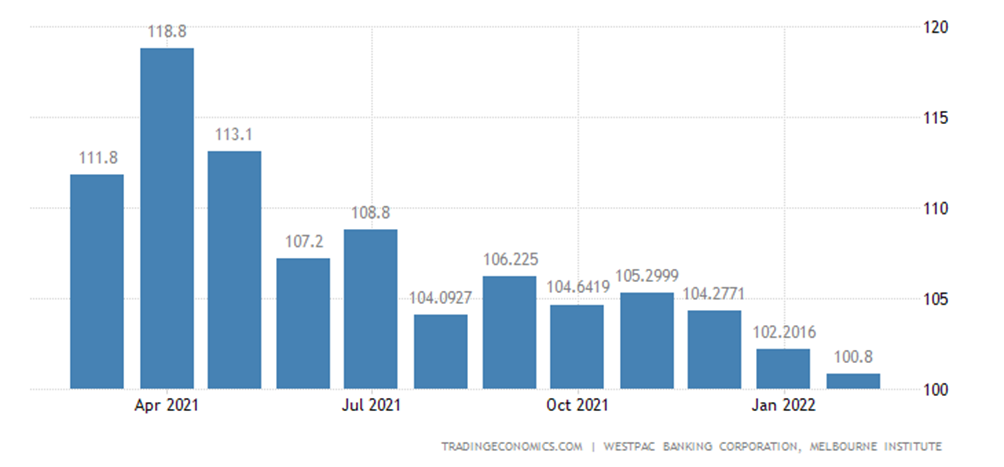

Australian consumer confidence is at its weakest since September 2020:

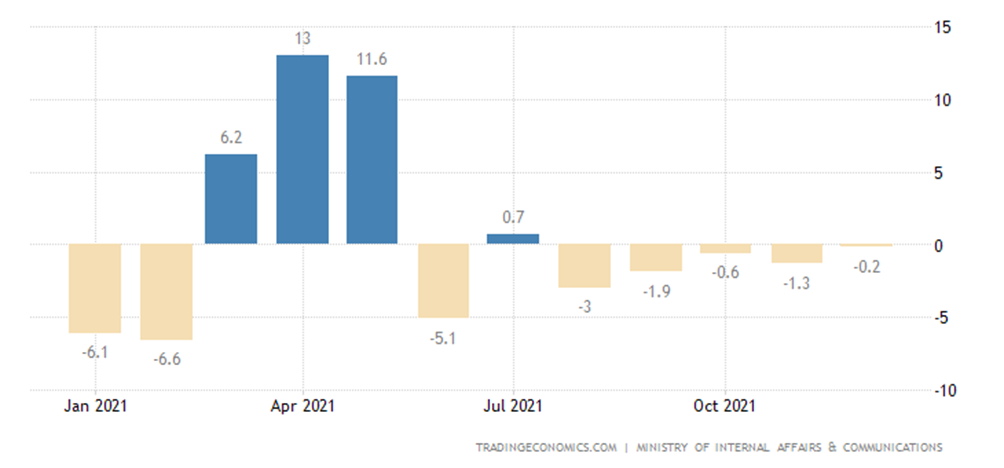

The income of the Japanese went into the annual red (-0.2%) for the first time in 10 months:

And their expenses have remained there for half a year (also -0.2%):

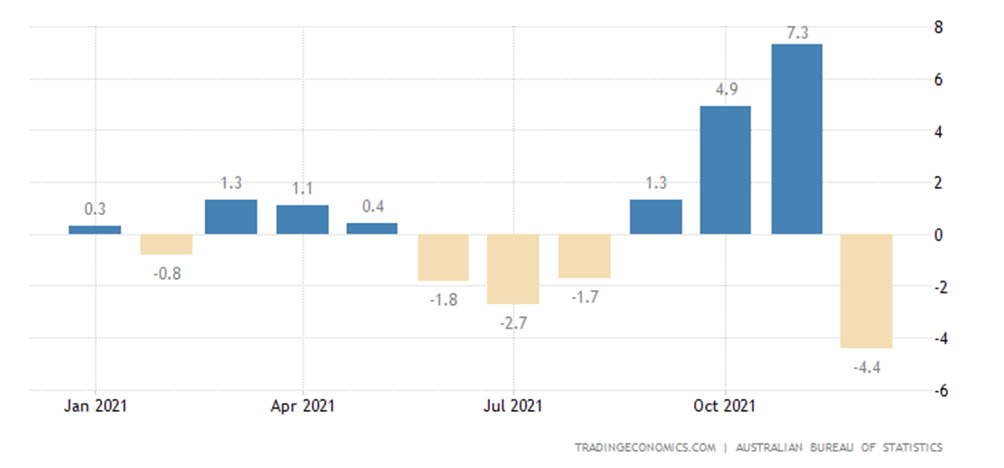

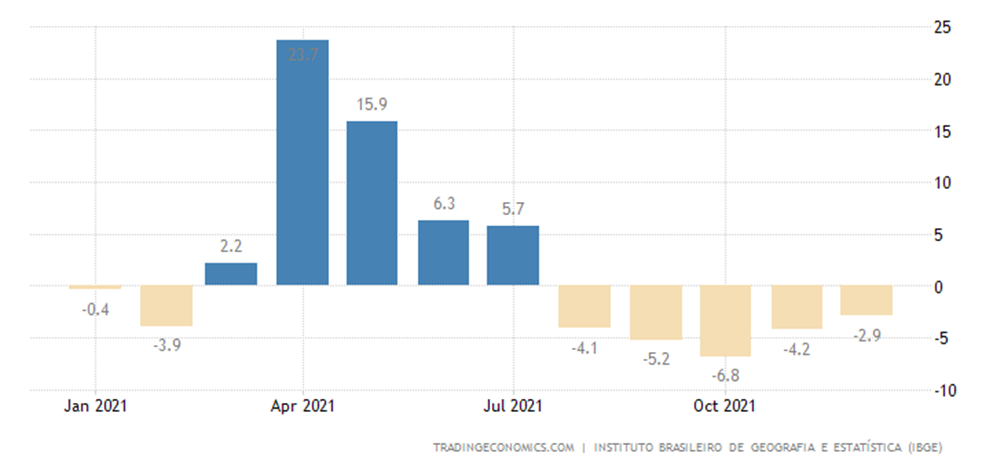

Retail sales in Australia -4.4% per month, the worst performance in 20 months:

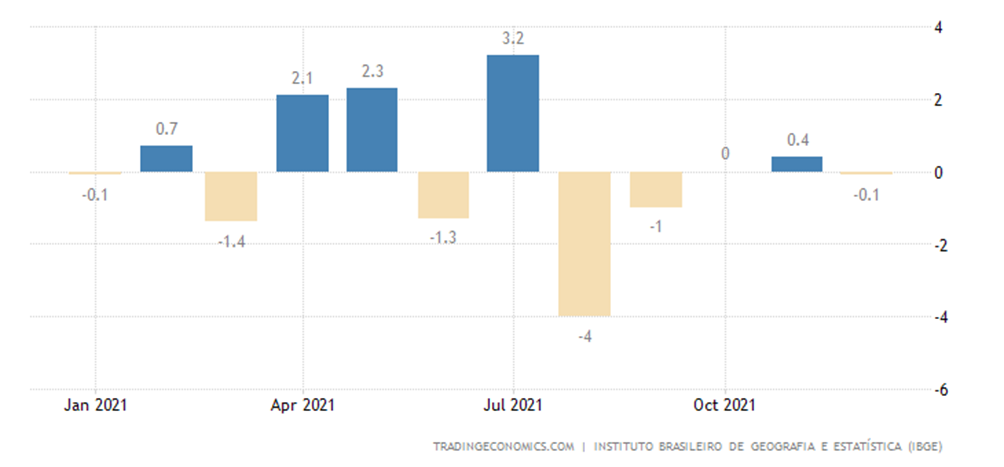

Retail Brazil -0.1% per month (there was only 1 positive in the last 5 months):

And -2.9% per year, this is the 5th negative in a row:

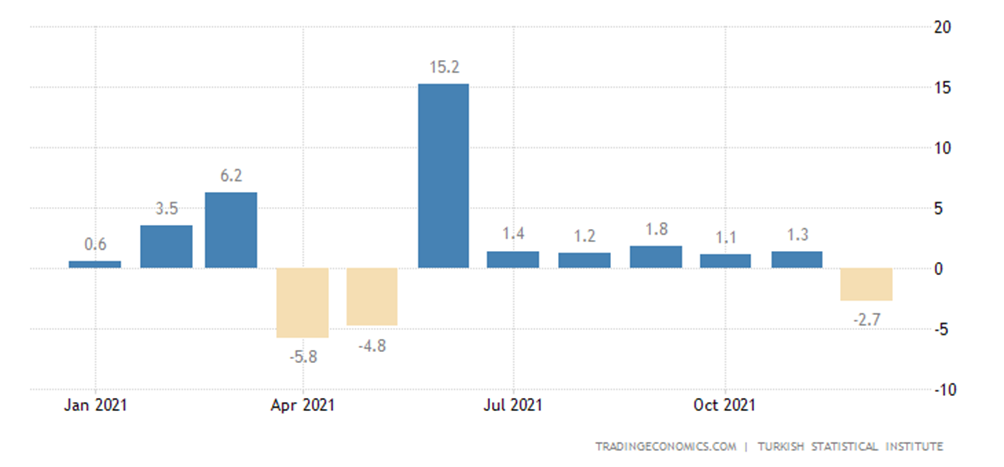

Retail Turkey -2.7% per month and is at the 7-month lows:

The Bank of Russia raised the rate by 1.0% to 9.5%, the highest in five years.

The Central Bank of Mexico raised the rate by 0.5% to 6.0%.

The Central Bank of India left its policy unchanged, as did the Central Bank of Indonesia.

Summary. Repeat the conclusions of the first section of this Survey: in a situation where inflation has two components – monetary and structural – any monetary policy is useless. If it is tightened, the structural component of inflation increases (for the United States, as we already found out in the previous Review, it is about 20% for industrial inflation today), if it is softened, the monetary component grows.

Indeed, that is precisely the dilemma of the Fed’s leadership: if monetary policy (that is, providing liquidity to the economy) is relaxed, the crisis becomes more manageable and protracted, but its final extent is intensifying. If policies are tightened (liquidity withdrawn, rate raised), the crisis accelerates and becomes less controllable. It is in this scenario that speculative markets could collapse abruptly and dramatically.

According to a number of experts (quoted above by Pavel Ryabov), the imbalance in the debt market has become so severe that it is almost impossible to contain the situation. We cannot confidently state this: since the system has long exceeded the boundaries of all “normal” intervals, there is nothing to compare the situation with. There are no models, no analogues in history. So we can only observe, realizing that the real economy is firmly on the path of continuous downturn. Which can be hidden in official figures, understating inflation, but it is impossible to hide the overall economic decline and the decline in living standards.

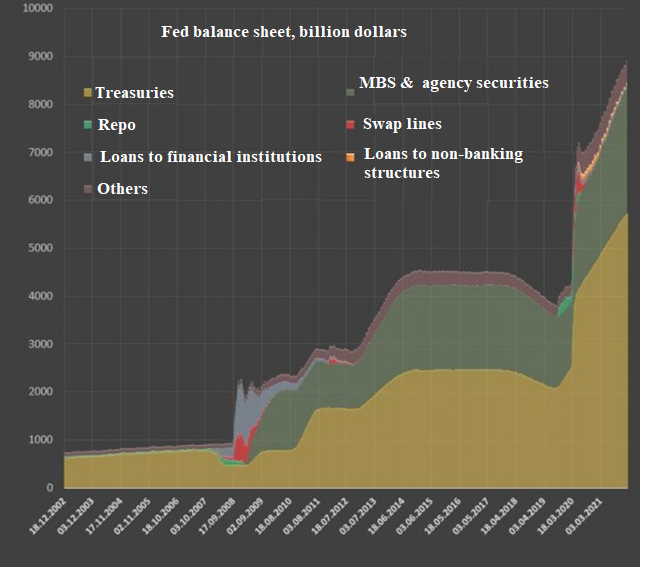

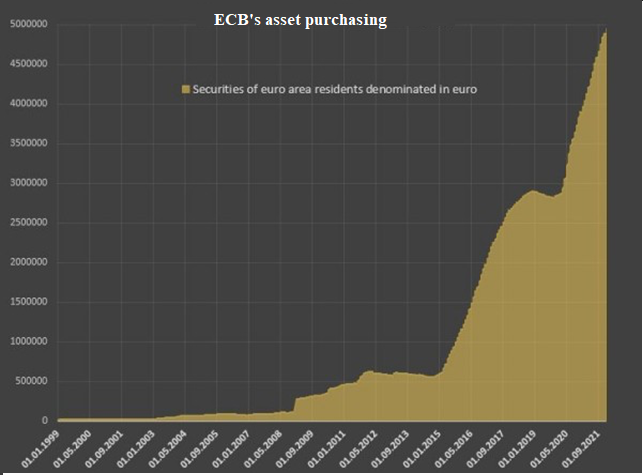

Let us note that the Fed leadership, under pressure from the Biden administration to demand a positive (or, rather, at least not a negative) outcome of the November election, does not see the structural component of inflation. And, as a consequence, it’s trying to solve the inflation problem solely by reducing the money supply. Here are some more graphics from Pavel Ryabov’s LiveJournal, namely the Fed’s balance sheet and the ECB’s balance sheet of recent years:

With such constant injection of liquidity “blossoms” any speculative markets along with inflation. But if the decision to tighten monetary policy is implemented (probably as early as Monday), we will get a remarkable picture – a sharp drop in the profitability of any company, aggregate demand collapses rapidly against the backdrop of high structural inflation. It is impossible to explain this to Powell and Lagarde, who do not know the current theory of the crisis, but the result will be quite unexpected for them.

We wish all our readers a happy working week!