Time period: 25-31 December 2021

Top news story. The main news of the week was a political event – a conversation between US President Biden and Russian President Putin, which had unexpected results. And we think that this event is directly economic in nature, and that’s why. The interaction with Russia takes place against the logic of the “deep state” of the progressive movement, therefore it has to have very serious objective (economic) grounds.

This ground – in the form of inflation – we foresaw in our Reviews long before US officials began to discuss them. These discussions began in September with assurances that the rise in industrial inflation was “accidental” and would quickly stop. As early as August, we warned our readers that, on the contrary, consumer inflation would start to rise after industrial inflation.

We must pay tribute to the new US political leadership, which came to power in the logic of “returning to Obama’s policies”, and two months later, by mid-March, it realized that there were no resources for such policies, and Biden turned the wheel of public policy drastically, including in relations with Russia. But monetary policy is the prerogative of the monetary authorities, first and foremost the US Federal Reserve, and their response is clearly overdue.

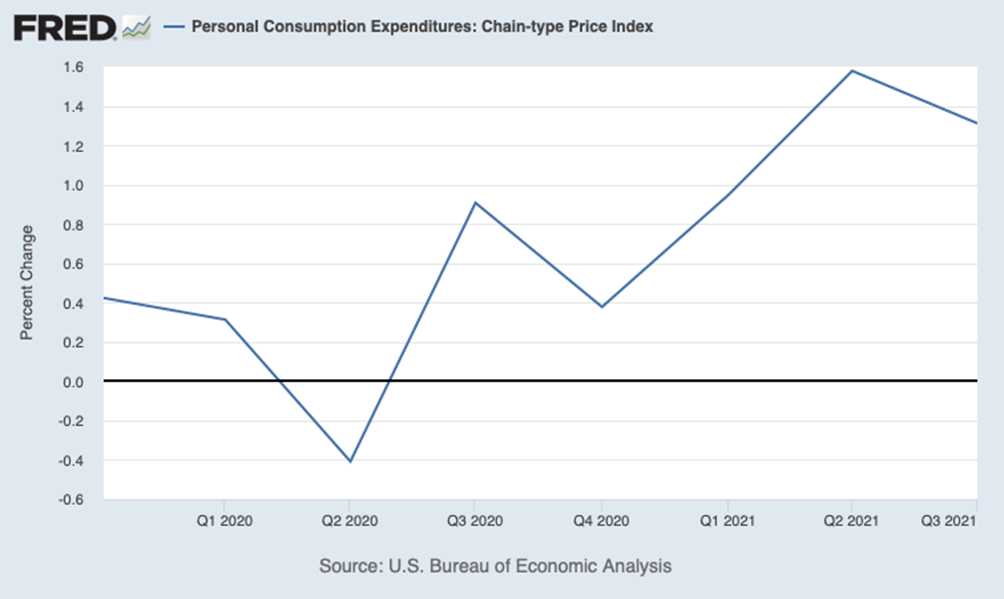

It should be noted that these are still official statistics (and somewhat outdated, newer and less “official” in the previous Review), but the graph shows that inflation has stopped a little.

The sterilization began sometime in mid-November (primarily through reverse REPO operations), and the result did not slow down – consumer prices began to roll back from their peaks (we wrote about it in the previous Review). On the official graph, however, only a drop in the rate of growth of consumer inflation is observed (on the graph – the Chain-Type Price Index, that is, the rate of change relative to the previous quarter).

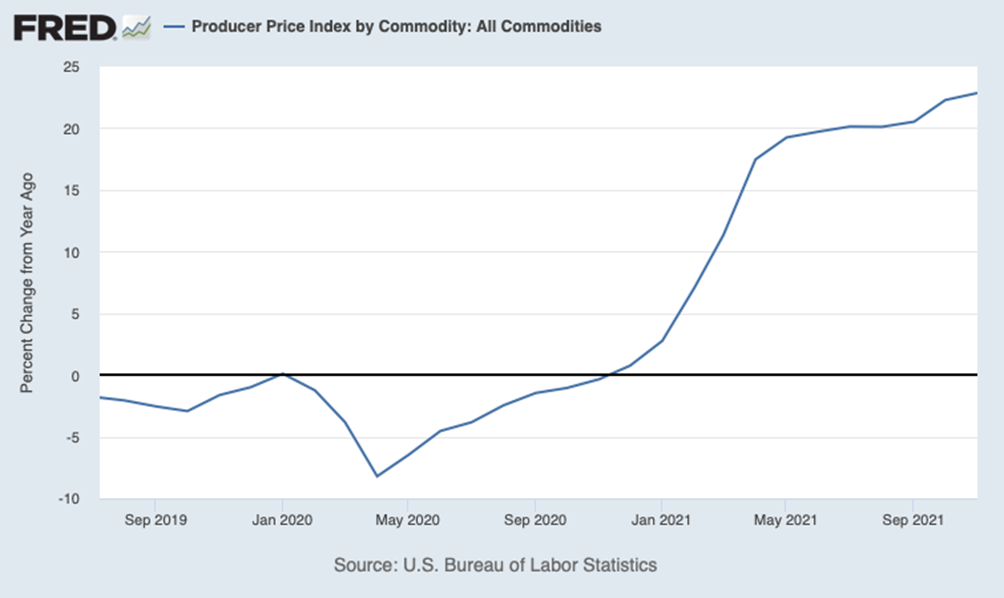

However, industrial price reactions were not so convincing, their rise almost halted (industrial inflation rose from 25% to 26.3% in two months), but the decline has not yet been noticed. And there are reasons (see the last section of this Review) that a new tide may begin.

Since entering the 2022 election campaign (the election will take place in early November) with industrial inflation of about 25% is a disaster for the Democratic Party, and the deadline for reducing it is the end of May, rather tough measures are needed to reduce the burden on the dollar emission center. And it’s the biggest cost of maintaining the world’s dollar system.

It is for this reason that negotiations with Modi, Xi, and Putin are so important – it is these three who must take responsibility in the context of the collapse of the world dollar system and the reduction of the Fed’s burden. Without this, the US economy cannot be improved. Let us remind you that the world dollar system (Bretton Woods) began in 1944, when the US share in the world economic system was more than 50%, and today it does not exceed 16-18%. And judging by Biden’s actions, he and his team understand that.

It is for this reason that negotiations with Putin play such an important economic role, especially for the US: if they fail, inflation in the US cannot be stabilized. Or, more precisely, they will not be able to do so in a manageable process, whereas they will be able to deflate on a 1930-32 model. But if agreements are reached by the beginning of the year, and their potential stakes are comparable to 1944-45, then Biden’s team has a chance.

Macroeconomics

United States Dallas Fed Manufacturing Index declines for 2 consecutive months:

In the service sector of the same region, there is also a 3-month trough:

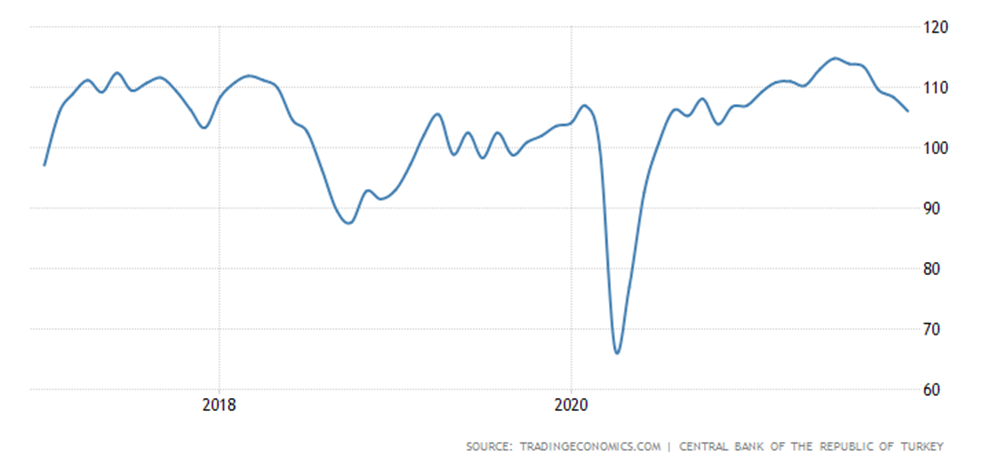

Business confidence in Turkey is at the trough for 13 months – apparently, Erdoğan does not have everything under control. I wrote a column about this in my Telegram channel, but apparently there is a need to make a model of the Turkish economy. The India Economy Report and the United States In-depth analysis are in the process of being published, but it seems that Turkey’s time has come.

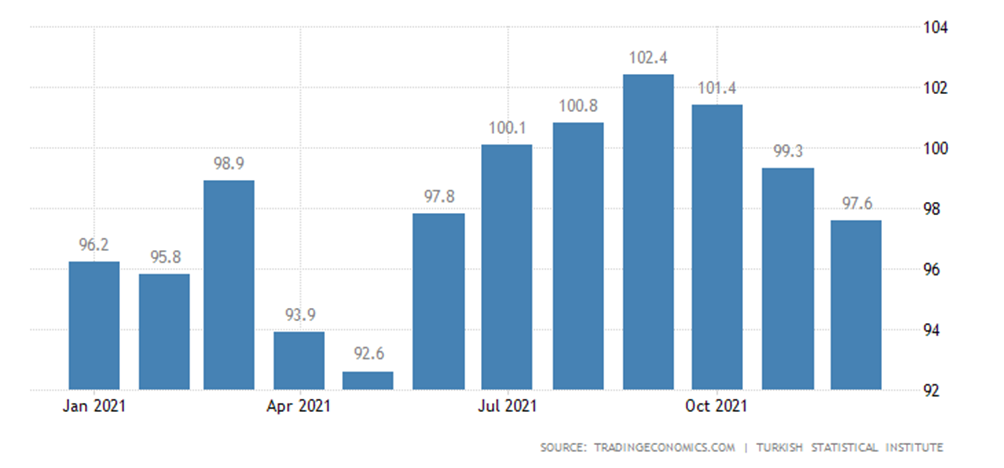

And the consumer sentiment of the Turks is on the seven-month trough:

KOF economic barometer in Switzerland is the worst in 10 months:

Business confidence in the Russian Federation is the weakest in a year:

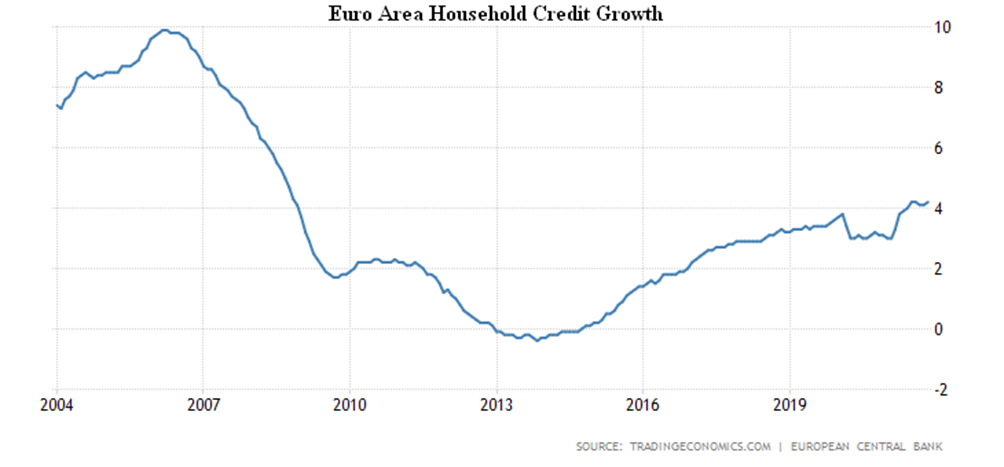

The Euro Area household lending +4.2% per annum, which is 13-year high:

This in itself is not very favourable, as households try to maintain their standard of living by borrowing, and if a crisis ends quickly, it helps to smooth out its negative effects, but if it is prolonged, the opposite is true. As there is no indication that the crisis has come to an end (see below), this figure is extremely pessimistic.

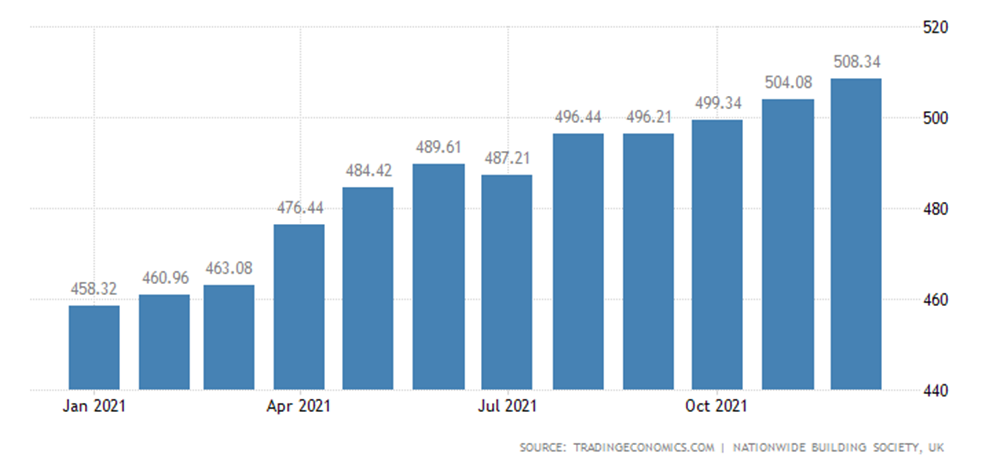

House prices in Britain +10.4% per year to a record high:

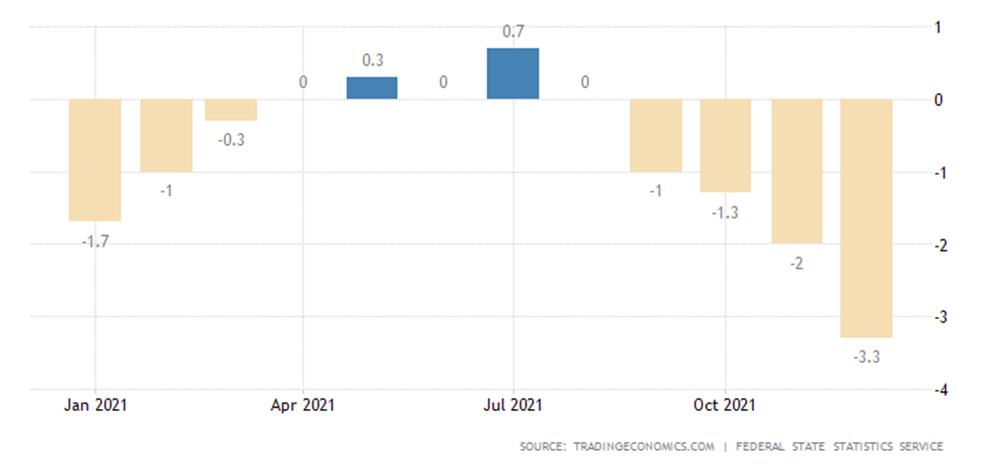

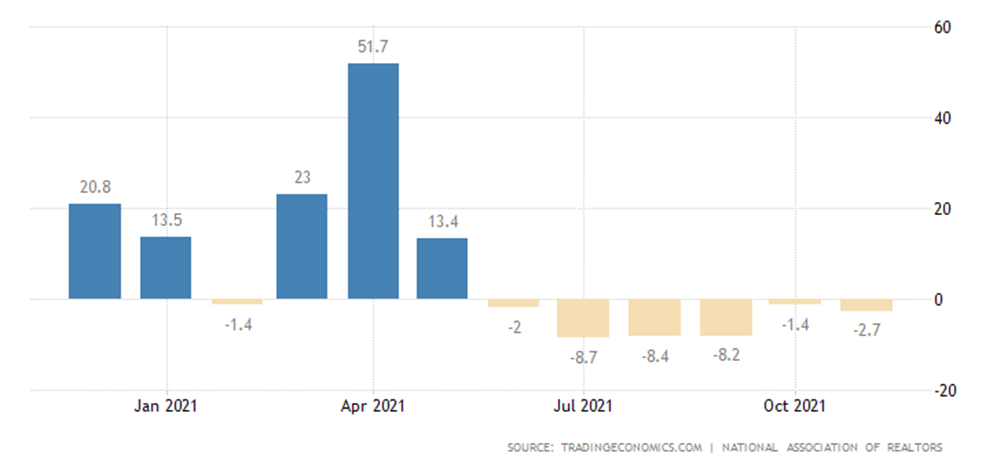

Pending home sales in the US -2.2% per month:

-2.7% per year, which is the 6th negative value in a row:

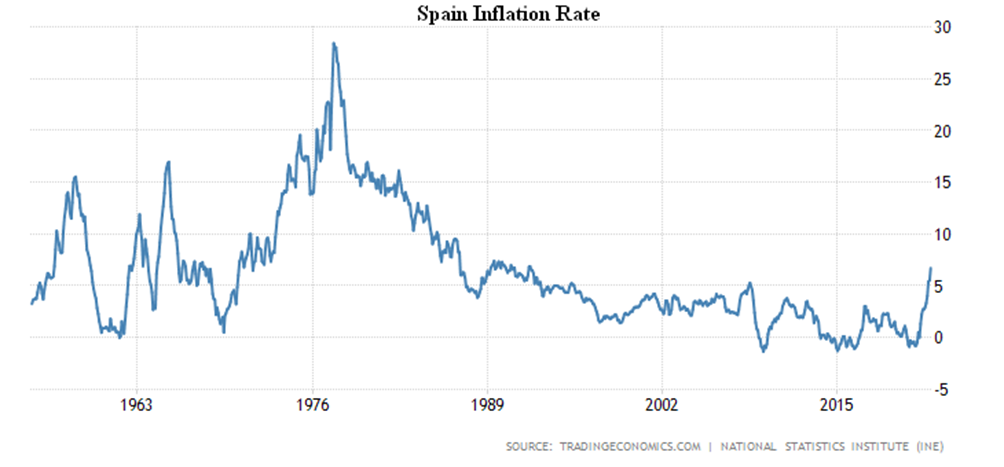

CPI Spain +6.7% per year, at its highest since 1992:

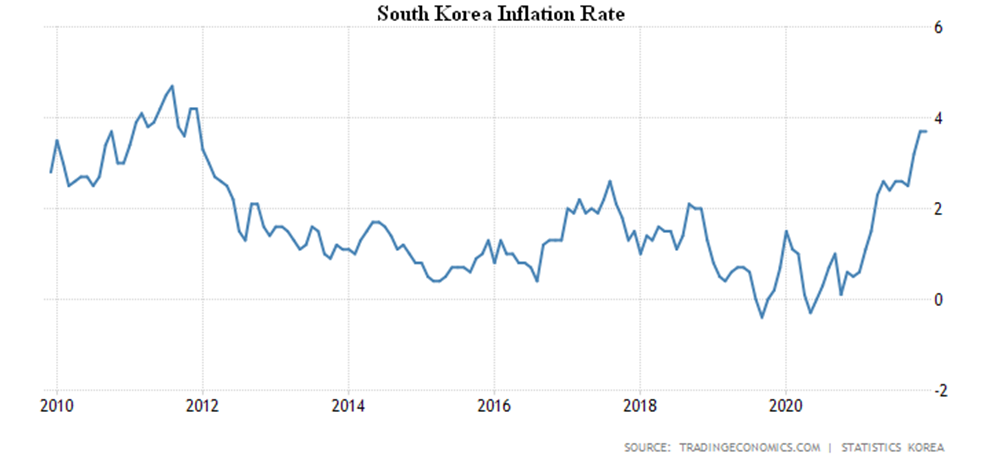

CPI of South Korea +3.7% per year, which is a peak since 2011:

Summary. The general theory of structural crisis is set out in M. Khazin’s book “Reminiscences about the Future”, but let’s try to explain briefly the essence of the problem, because otherwise it will be difficult to explain further problems of the world economy. The essence of the modern model of the economy is that, starting in 1981, the monetary authorities of the United States began to provide credit stimulus to household demand. The main instrument of this process was the refinancing of private debt against ever-declining interest.

As a result, from 1981 to 2008, the United States Federal Reserve’s interest rate fell from 19% to almost zero (in December 2008), and average household debt rose from a historical high until the start of the Reaganomics policy, 60-65% of real disposable income, doubled, up to 132-135%. The point of all the events that have taken place since then has been to avert the crisis, the details of which can be read in the above-mentioned book by M. Khazin, but now it is important that maintaining the standard of living of people since 2019 has become possible only through direct emissions. It is important that rising living standards have significantly transformed the pattern of private demand. Goods and whole groups of goods that were included before the beginning of the 80s in the group of luxury became mass consumption goods, a mass middle class appeared. Moreover, even new industries have emerged, and also very large ones: for example, modern tourism with a focus on 4-5 star hotels.

The inevitable decline in demand and the almost inevitable disappearance of the masses of the middle class will reverse the process: many goods will revert back to luxury, some industries will simply cease to exist. The fall in demand for specific groups of industries is highly uneven, and any production with a high division of labour is concentrated in multiple sectors.

Consequently, the process of structural price increase, which is linked to the need to support production in a context of falling demand and rising costs, is occurring in different ways in different industries, and prices can both rise and fall. A typical example is the behavior of US lumber prices:

In addition, a highly speculative sector allows the use of these shifts in normal financial and trade flows with their general decline, which leads to a very phantasy-like skyrocketing in prices, as, for example, for gas in the European Union. Note that the prices here are not for 1000 cubic meters, as in our Russia, but for the energy equivalent, so the figures are not entirely familiar.

There is no doubt that the rise in inflation in the past year 2021 has led to a fall in the standard of living of the people, all GDP growth statistics have been associated with an under-inflation, and we have repeatedly shown in last year’s Reviews why they are not reliable. In particular, to compensate for the inflationary recession, the growth in sales of industrial enterprises in nominal terms should be at least 25-27%, and if we assume an increase of 7%, then 32-34%. It doesn’t even make you laugh.

Part of this falling demand during the pandemic was offset by budget expenditures (made at the expense of core emissions), but the compensation is running out. And here it turns out that real salaries have fallen, and jobs have decreased, and somehow it is impossible to return to the previous standard of living.

Thus, we think that if the US monetary authorities do not take extraordinary measures, then producer prices will enter a new round of growth. Well, or, equivalently, they will not fall against the backdrop of tightening monetary policy (that is, the growth of the cost of money). Already now, reverse REPO operations complicate the work of small and medium-sized businesses, since the cost of a loan to replenish working capital is growing for them – for this reason, we predict a worsening of the situation.

Note that the instruments of monetary policy are generally not capable of having a serious impact on the processes of structural inflation, the fact is that it is no longer possible to compensate for the falling demand of households through loans (the rate no longer falls, banks stop lending), and direct subsidies have a sharp negative effect on consumer psychology. It is not even socialism, at which it was impossible not to work, it is something like the “Roman Empire during the recession”, at which people demanded “panem et circenses” and threatened, otherwise, to start a riot.

As the structural crisis develops further, shifts in commodity and financial flows will become more and more significant, and either the budget will constantly increase its expenses to compensate them (with inflation), or at some point this process will be stopped. It is almost impossible to pinpoint this moment precisely (it is accepted at the political level), but some hypotheses can be made, the US authorities have adopted some real-sector development programmes (“structural reforms”), and the money spent within them can be that compensation (at least partial) what the US economy needs.

The problem is that this money can quickly be taken out of the economy, the simplest option – when reinforced concrete parts purchased to repair bridges, which are written off at the price of the US domestic market, can be produced in Korea or Vietnam. At a price three times less. Without a rigid restriction on the movement of goods and capital, this problem cannot be solved, but it means a rapid collapse of the WTO and the entire Bretton Woods system, at the initiative of the United States (See the first section of this Review). If our hypothesis about the reasons for Biden and Putin’s negotiations is correct, the process could start as early as the end of January, with all the attendant consequences.

And if decisions of this magnitude are not made, the structural crisis will come into full force, and then the US (and the world) will go into socio-political cataclysms of unthinkable power. Thus, the choice here is quite simple: the alternative to abandoning the Bretton Woods dollar system is an unmanageable global recession of 1.5 to 2 times greater scope than the 1930-32 crisis. In general, 2022 is likely to be part of world history, and our readers have a clear competitive advantage, because experience has shown that we warn them of problems well before they can learn about them in the official press.

Happy New Year to our readers and wish them good luck and happiness!