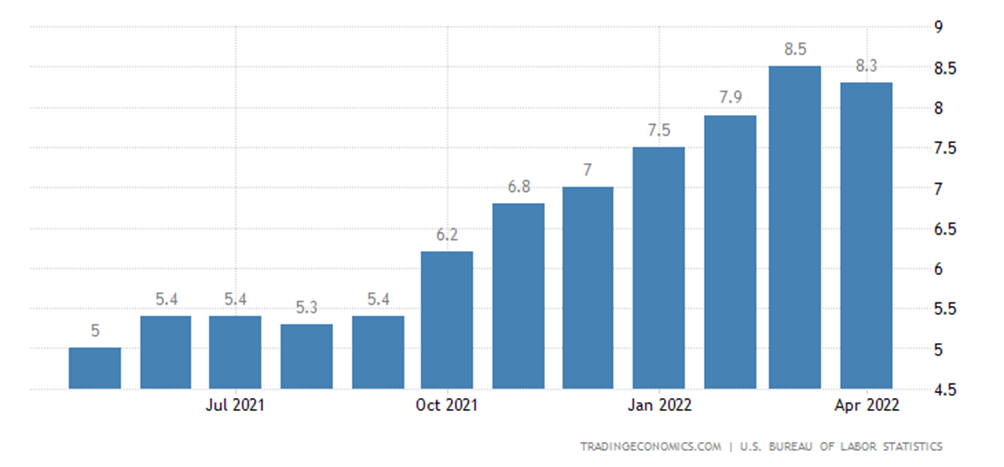

Time period: May 7 – 13, 2022

Top news story. The main news of the week was consumer-price inflation rate. What is important is not the value of the indicator, but its slight difference from the previous week:

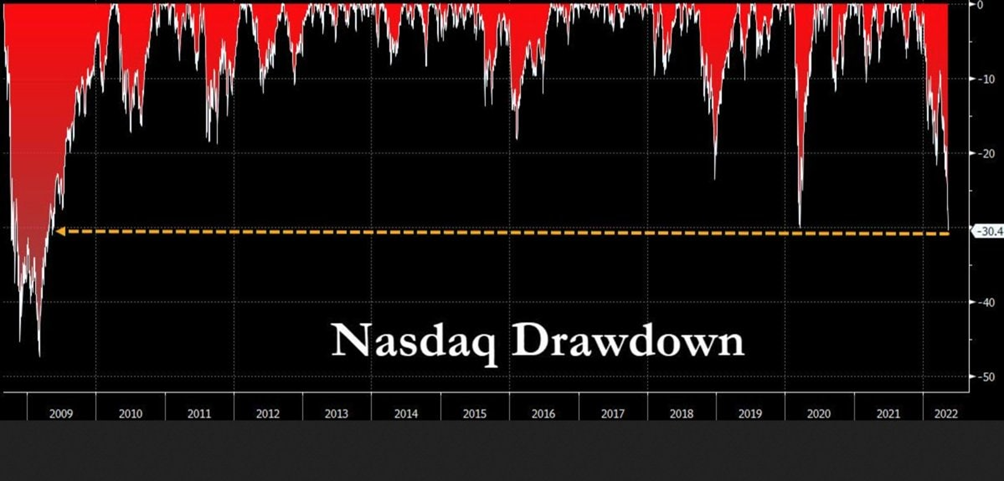

The market reaction turned out to be sharply negative, as can be seen from the NASDAQ index, which showed a record-high decline since 2008:

And in other markets, the pace of negative processes began to grow, for example, there was a collapse of cryptocurrencies:

The reason for this behavior lies in the fact that last week (see the previous Review) the US Federal Reserve raised the interest rate by 0.5%, its leaders made it quite clear that there will be a further increase, and the asset buyout is just around the corner. And stimulating the economy with issuance money is almost over. Such a policy, of course, financial speculators will definitely not like (which caused the adjustments in stock markets), but fundamentally here it is precisely that the inflation figures did not react to this policy directly.

According to mainstream monetary theory, inflation should have been reduced. In fact, this did not happen, and we recall that we have described the reasons for this on several previous occasions in our reviews. The fact is that as part of the Crisis of capital effectiveness in the United States, a structural crisis began, similar to the one that happened in 1930-32 and led to the Great Depression. The structure of the economy is beginning to return spontaneously to an equilibrium state, which is characterized by a balance between real income and household expenditure.

In 1929, the gap between real (i.e., what the US economy could provide) incomes and expenditures overstated by financial boosting of demand reached 15% of GDP, so the decline exceeded 30%. Today, the gap exceeds 25%, which means that, as a result of the structural crisis, the recession will be more than 50% of the US real GDP, which is about $15 trillion, because everything else is a fictitious cost associated with the revaluation of financial assets.

Current US inflation is ambivalent: it is partly monetary and partly structural. Monetary tightening certainly reduces the first component, but increases the second. As the Fed’s experiment showed, the collective impact was in favor of reducing inflation, but the effect was miserable. However, the negative effects of the rate hikes, mainly demand reduction due to the need to reallocate income to debt servicing, have not been reversed.

Macroeconomics

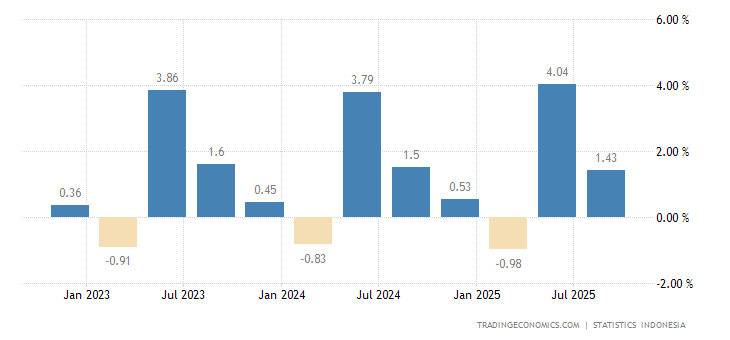

Indonesian GDP growth rate was -1.0% QoQ:

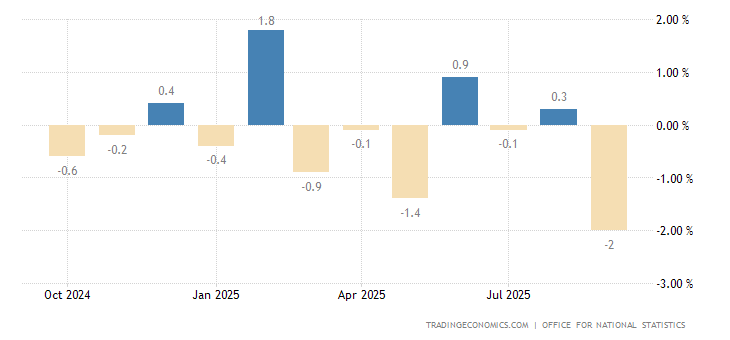

Britain’s industrial production is decreasing monthly for two consecutive months:

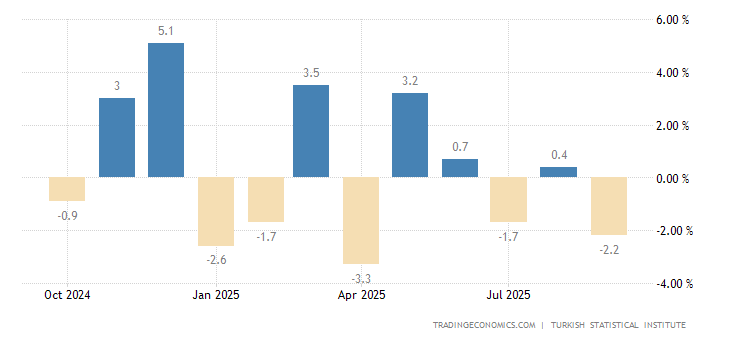

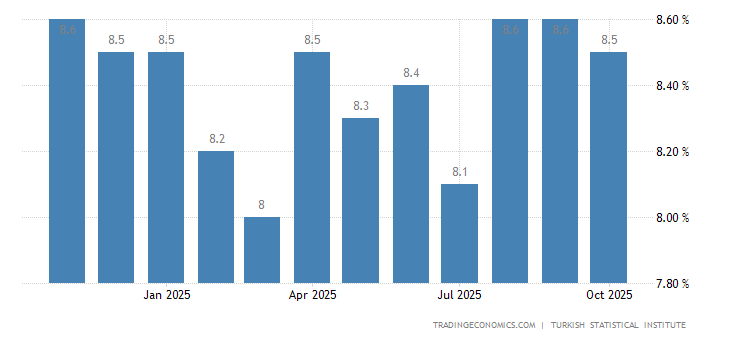

In Turkey, the 2nd negative in 3 months:

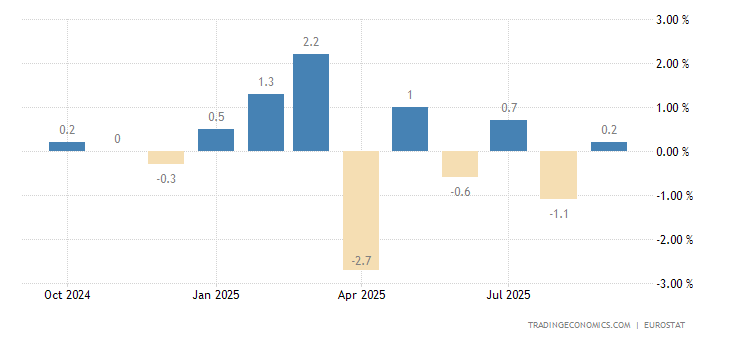

The Euro Area industrial output -1.8% m/m. it’s a 2-year low:

Why the annual performance returned to decline (-0.8%):

We recall, and this comment applies to some of the following indicators, that these data are calculated with under-inflation, so that in reality the situation is worse. Maybe a lot worse.

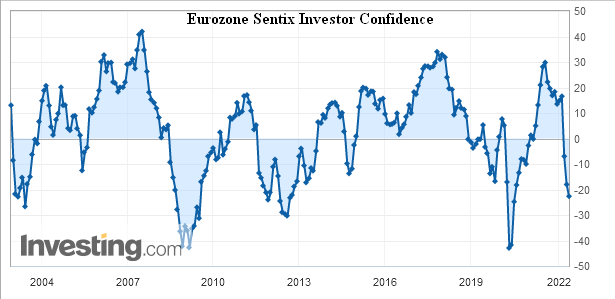

Investor confidence in the eurozone (Sentix survey) is the lowest in 2 years, and to put aside the coronavirus panic, the worst was in the early 10s:

Economic sentiment in Germany from ZEW has improved, but the assessment of the current conditions is the worst for the year:

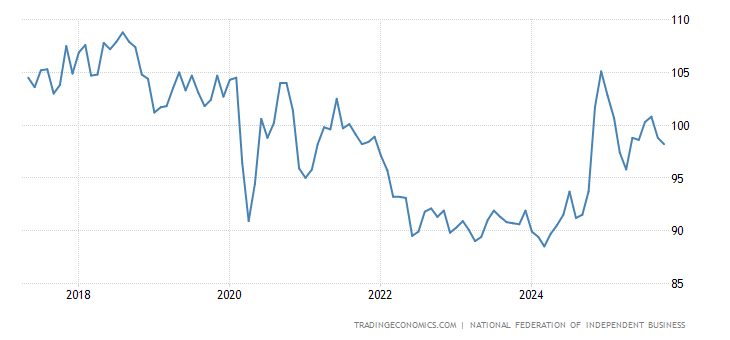

US small business optimism remains at 2-year trough:

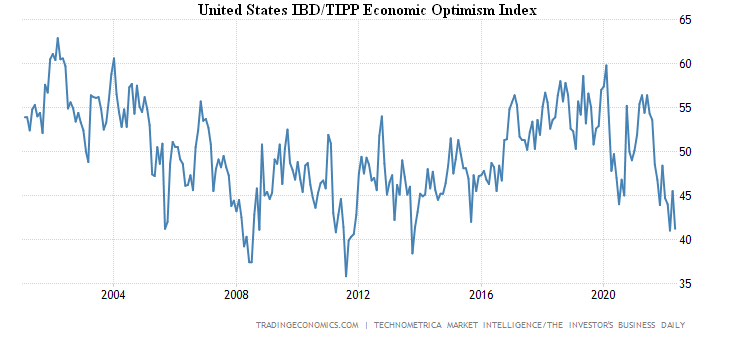

And the overall index of economic optimism (IBD/TIPP survey) is back to an 8-year low:

PMI (Purchasing Managers’ Index, industry peer review, below 50 means stagnation and decline) New Zealand’s industry is the weakest in 8 months:

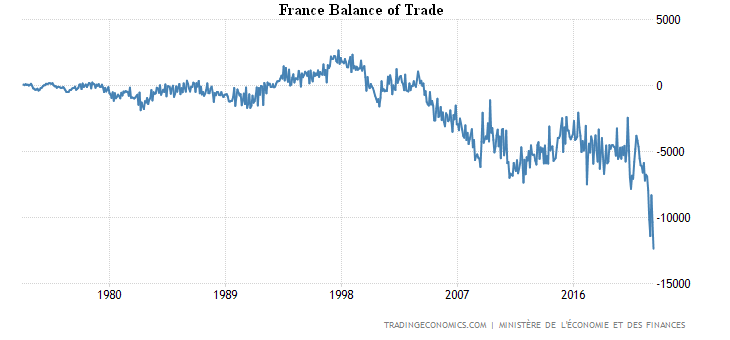

France’s trade deficit is record:

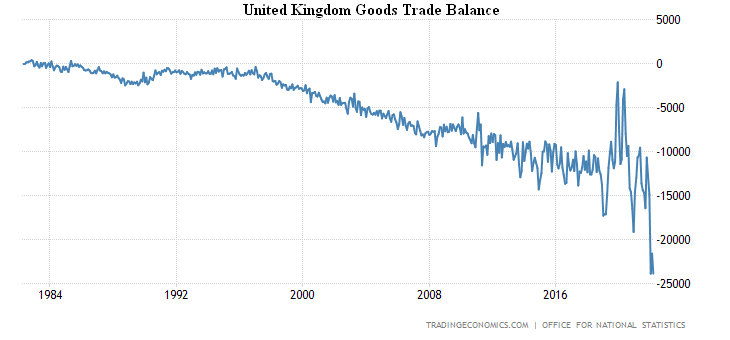

As well as the balance of trade in goods in Britain:

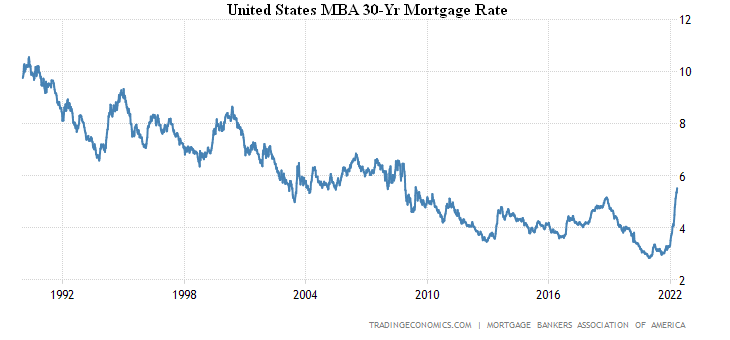

The US 30-year mortgage rate of 5.53% is the highest since 2008:

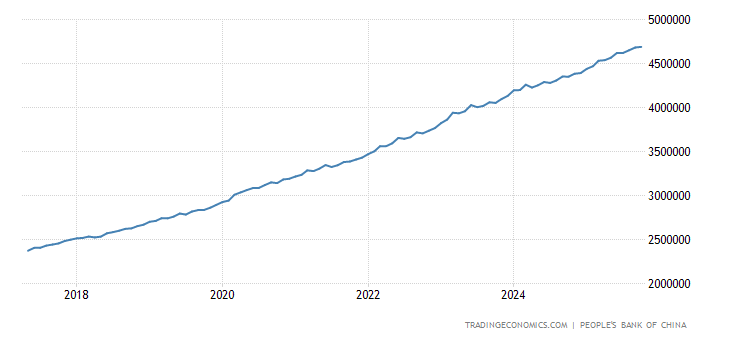

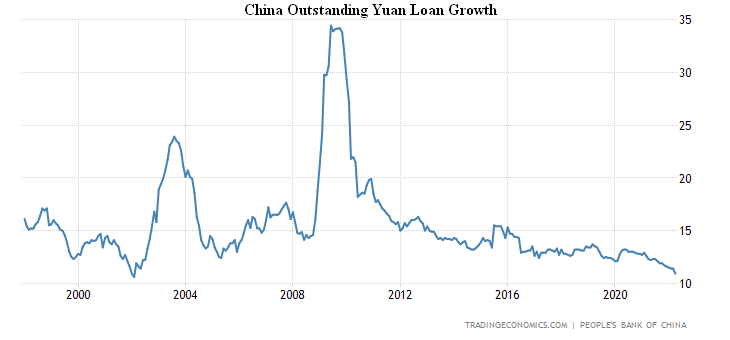

New yuan loans in China are at their lowest since 2017:

As a result, the annual growth in debt on these loans (+10.9%) came close to the record trough of 20 years ago (+10.6%):

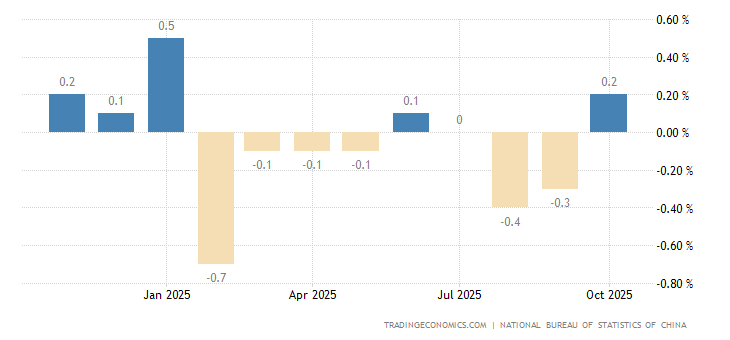

Chinese inflation is accelerating:

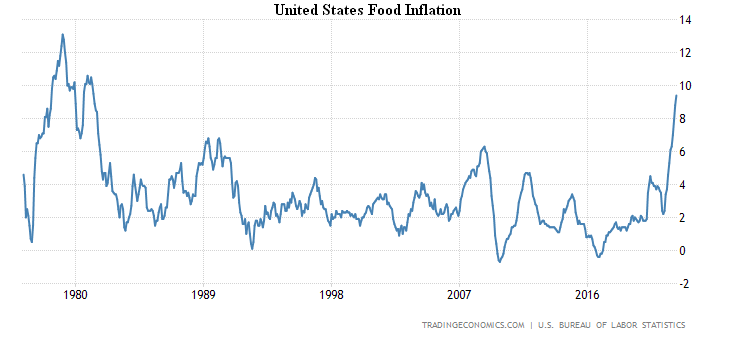

And in the US, inflation is slowing down, but weaker than expected (see the first section of this Review), although the cost of food is growing at the highest level since 1981:

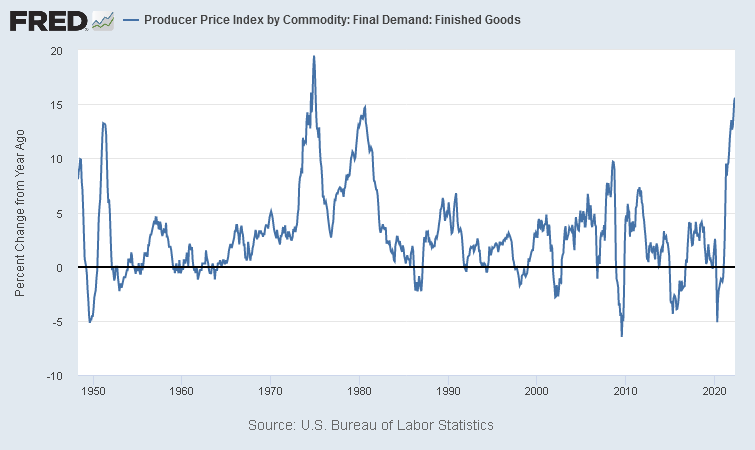

The same with the PPI (Producer Price Index) of the US — in general, braking, but for final goods it’s a peak since 1974 (+15.6% per year):

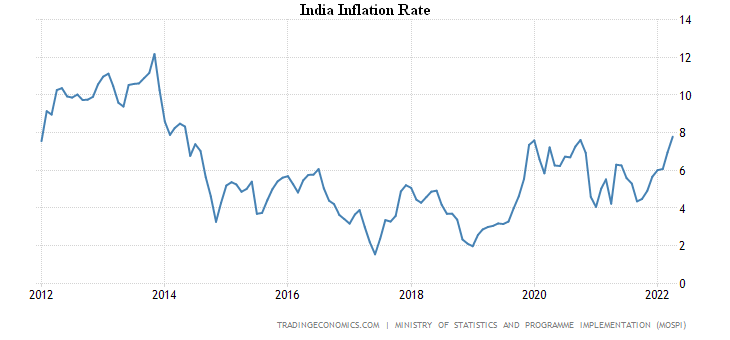

India’s CPI (Consumer Price Index) +7.8% y/y has risen to the top since 2014:

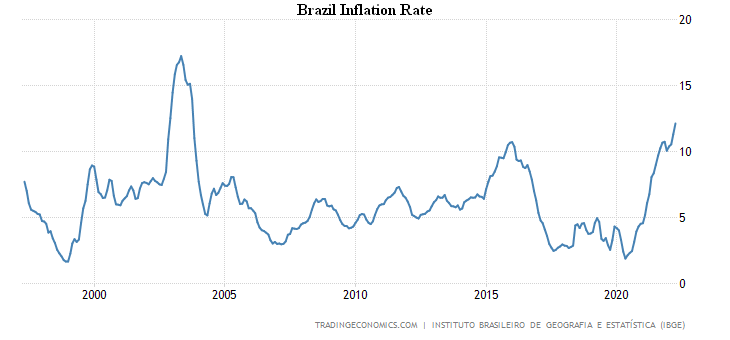

CPI of Brazil +12.1% per year, this is the peak since 2003:

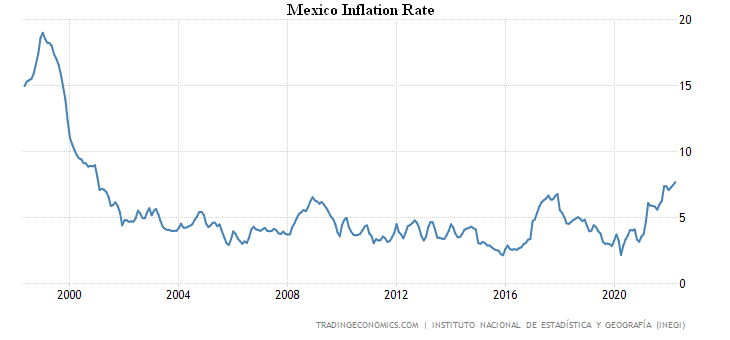

CPI Mexico +7.7% per year, the highest since January 2001:

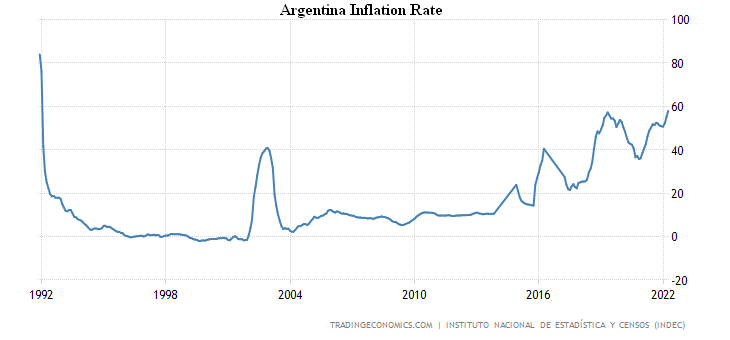

CPI Argentina +58.0% per year, that is the peak since January 1992:

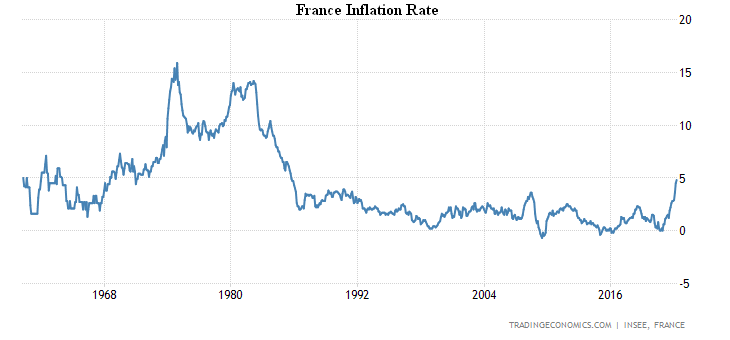

French CPI +4.8% per year, the highest since 1985:

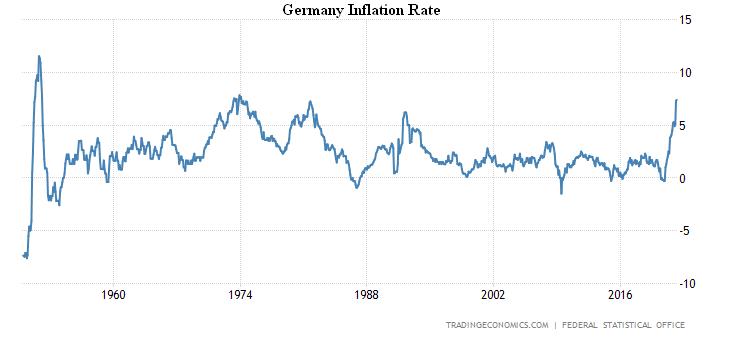

Germany’s CPI +7.4% y/y hit 1974 peak:

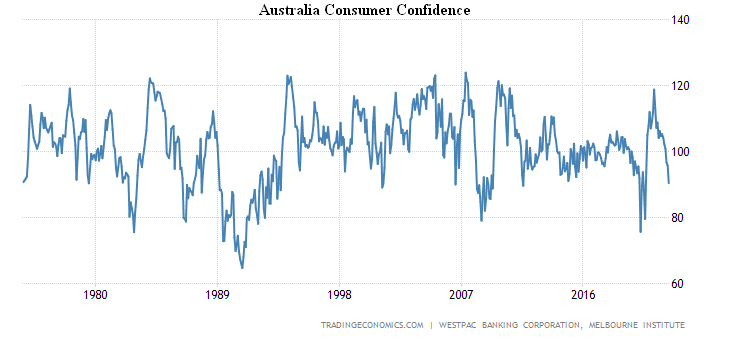

Australian consumer sentiment has plummeted in 7 years at a pace to levels during the pandemic:

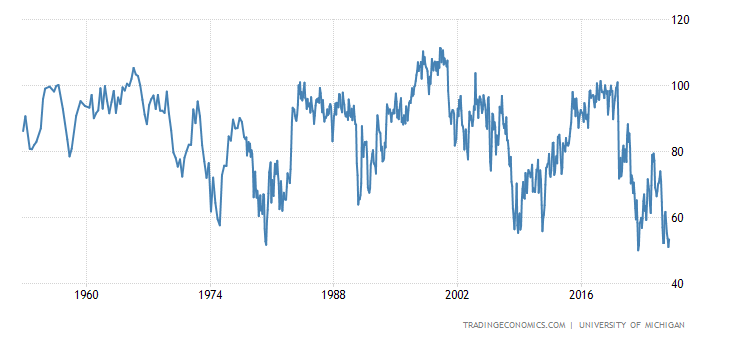

US Consumer Confidence revisited 11-Year trough:

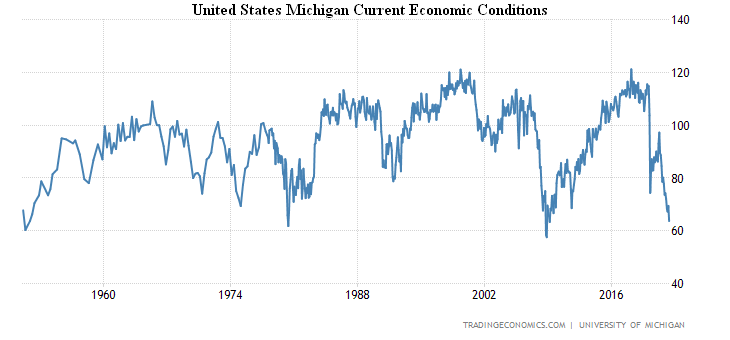

The assessment of the current conditions is the worst since 2008 and is close to the record lows of 1952, 1980 and 2008:

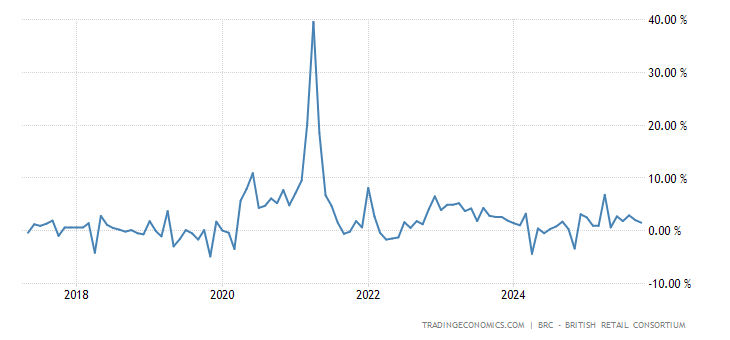

British retail monitor from BRC -1.7% per year, the lowest since March 2020:

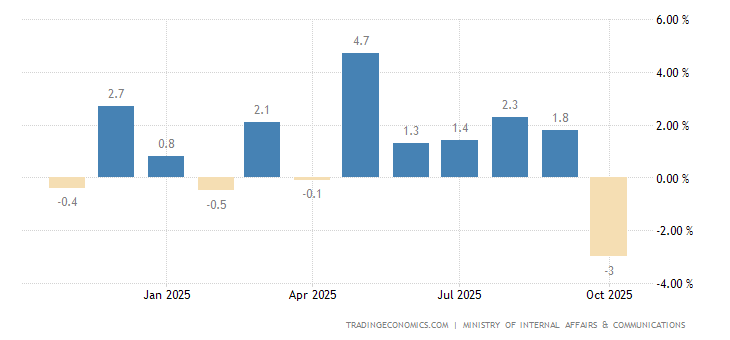

Japanese household spending is back in decline (-2.3% y/y: worst performance in 7 months):

Unemployment in Turkey is the highest in 7 months:

The Central Bank of Mexico raised the rate for the 8th consecutive time, by 0.5% to 7.0%.

Summary. As we have warned in previous reviews, the economy has stopped responding to monetary policy. The reason is described in the first section of this Review: the structural component of inflation responds to the effect in a reversed phase with the monetary component. At the same time, the resources to support private demand are no longer available — money is rapidly depreciating because of the same inflation.

As mentioned earlier, it is possible to postpone the problems until the autumn, because in the summer the discussion of economic troubles usually wanes.

Of course, it cannot be excluded that the decline in living standards in some countries will be so severe that people will be on the streets in the summer, but most likely this does not apply to the G7 countries. This means that the authorities will return to the inflation issue as early as September, when the situation will seriously worsen.

The only exception is the US, which is on the verge of campaigning, where critical views about the current government are gaining ground despite the colossal liberal (that is, pro-Democratic Party) censorship, but the trouble is that the Republican Party has no positive agenda either. It cannot exist, at least until the end of the structural crisis. Accordingly, there are no proposals for concrete action, and for this reason, the current policy of the Fed is likely to continue, especially since the reappointment of Fed Chairman Powell this week has given him confidence.

The US may ease sanctions activity against Russia somewhat, but the rate will continue to rise, and as a result, people’s living standards (aggregate demand) will fall sharply. Similar processes will continue in the world, except that euro emissions are likely to continue with rising inflation in the EU. This will somewhat restrain the decline in people’s living standards, but catalyze degenerative processes in the economy. In general, it is already possible to say with a high probability that the forecast of the future of the European Union is unfavorable in the medium term.

We wish our readers a trouble-free working week!