Period: 21 – 27 November 2020

Top news story: Undeniably the highlight of the week was a new historical Dow Jones Industrial Average (DJI) record of over 30 000. It’s brought out a lot of new and interesting things.

- First, the ability to inflate financial bubbles is not yet exhausted (in every sense of the phenomenon).

- Second, the process of transition money of issuing origin to the financial sector continues.

As we will show below, overall economic stimulus has failed, and the improvement continues only in the manufacturing sector (which today is far from dominant, the share of production in US GDP is now below 20%).

- Third, we see price increases in some sectors (for example, in real estate in the US), while deflationary effects are observed in others, which are clearly depressive.

This means that the structural crisis is not only continuing, but is also becoming stronger and its consequences will be felt.

- Fourth, the rise of the speculative sector compared to the real sector only reduces investment in the latter.

This means that production capital is not being reproduced, that is, that the crisis will continue. Financial institutions in this situation will only reduce investment in the real sector, whereas even the current level is not sufficient for the global economic reproduction.

In fact, the most general figures show that the Bretton Woods model has reached a deep impasse. Indeed, that is what the heads of the institutions concerned are saying – IMF Chief Kristalina Ivanova Georgieva-Kinova and FED Head Jerome Hayden Powell. However, they continue to try to correct the situation by using monetary methods that are useless in the given situation (see M. Khazin, «Reminiscences of the Future», Ch. 21).

The aforementioned book by M. Khazin describes an alternative theory of the crisis of the modern world economy. According to this theory, the controllability of economic processes can be restored only after the «cut» of the credit overhang, the scale of which exceeds all permissible limits. Let us note that this process will be extremely painful for the world economy, and certainly will be accompanied by a serious decline in world GDP.

Macroeconomics

The Euro Area composite PMI in November is the worst in six months (45,1 points):

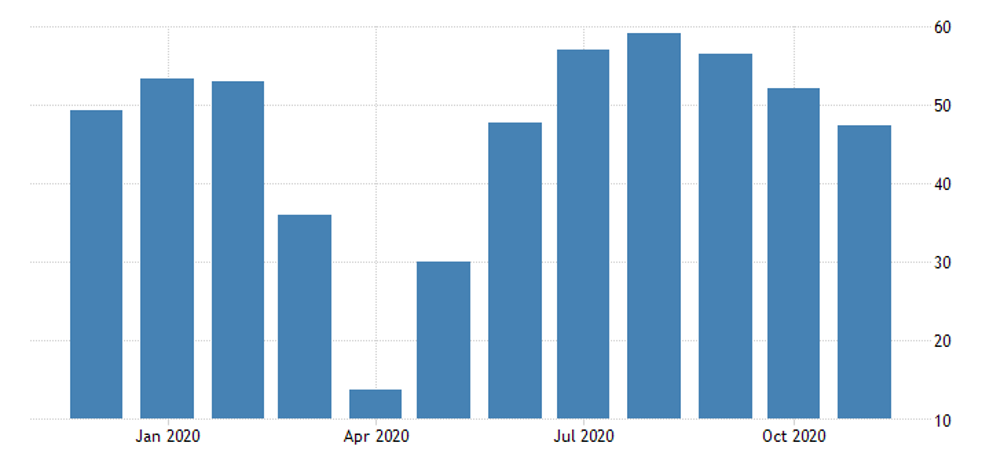

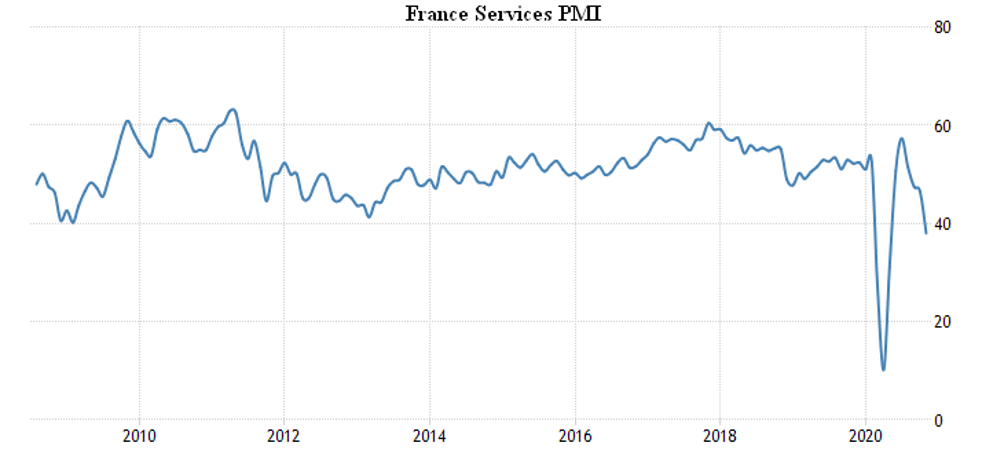

The manufacturing sector is in good shape (53,6 although it was 54,8 in October), but the services sector is in deep decline (41,3 after 46,9). The situation is worse in France, where 38,0:

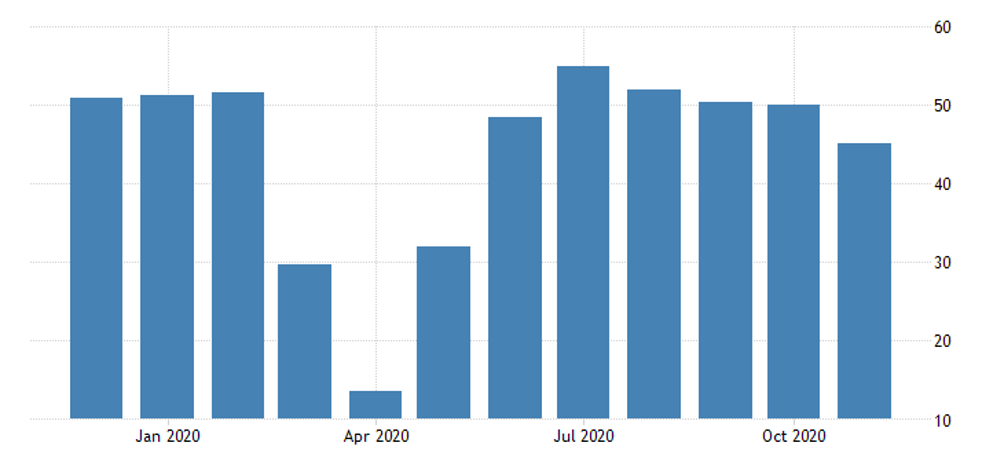

A similar picture in Britain is that production is even improving, but services have a six-month trough. As with the Composite Index:

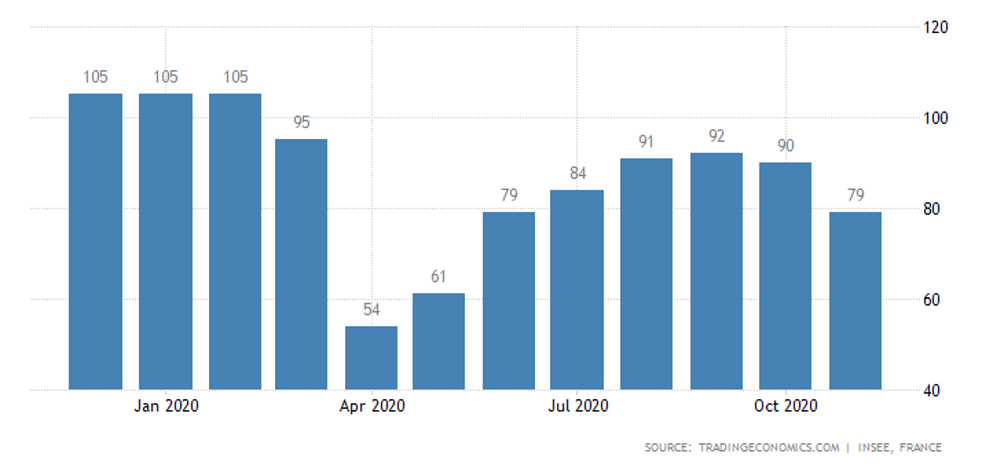

Business confidence in France is weakest in 4 months, and the business climate in half a year:

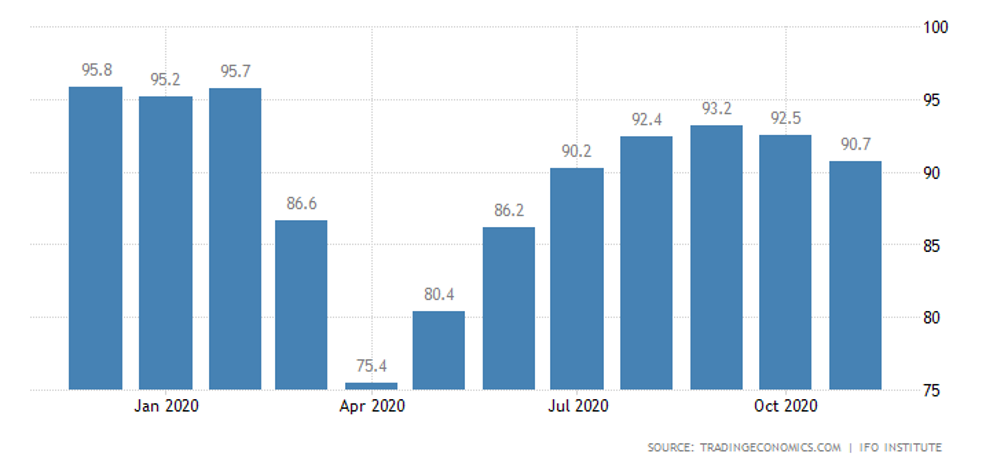

In Germany, the 4-month trough of the business climate according to IFO:

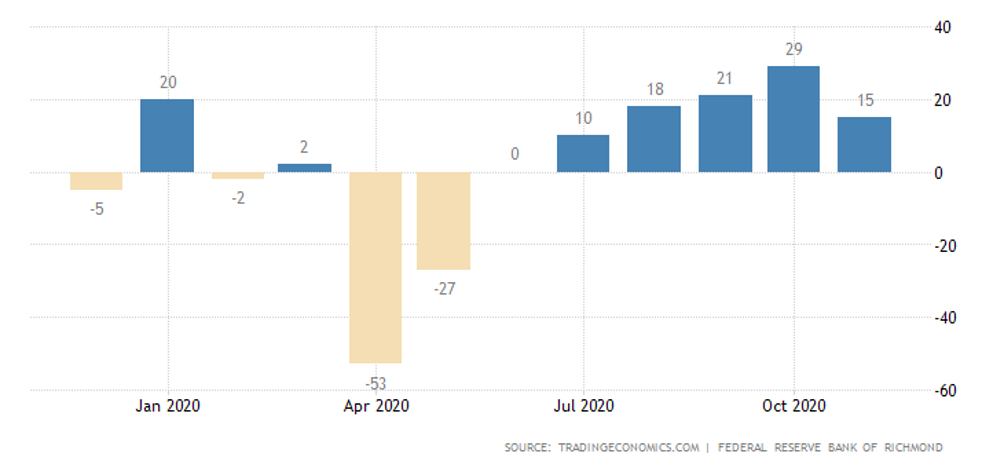

United States Richmond FED Manufacturing Index is the worst in 4 months:

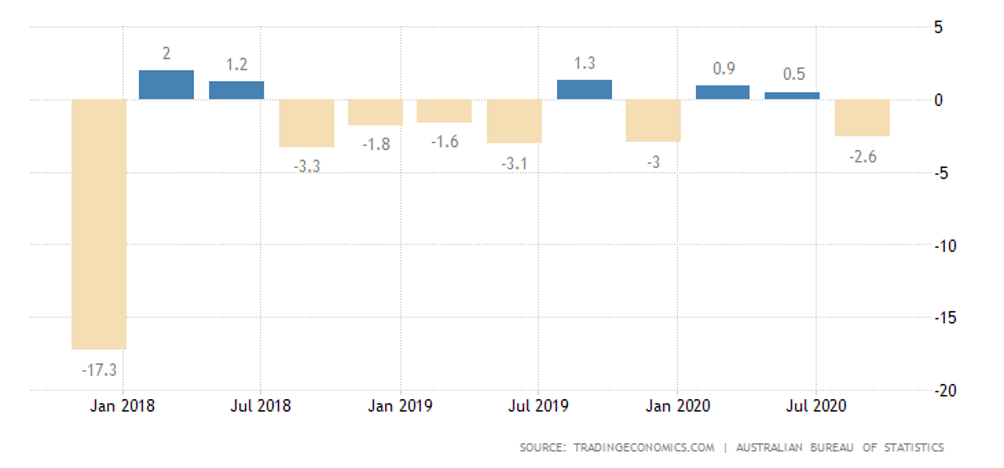

In Australia, construction output in the third quarter again went negative:

CPI in Tokyo -0,7% per year – the lowest since March 2013.

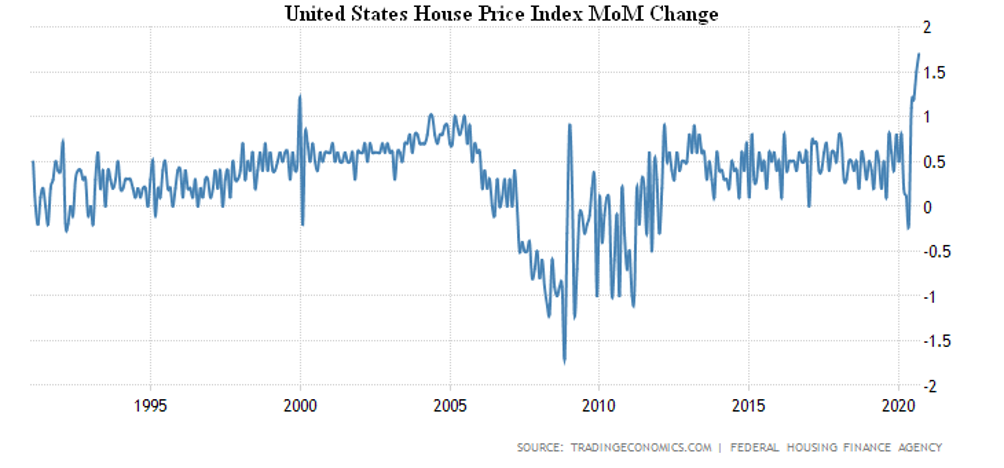

The S & P / Case-Shiller US National Home Price Index increased by 7,0% per year in September – the best growth since May 2014. Official figures also indicate a rapid increase: 1,7% per month (the record for 30 years of observation) and 9,1% per year; the «bubble» is there.

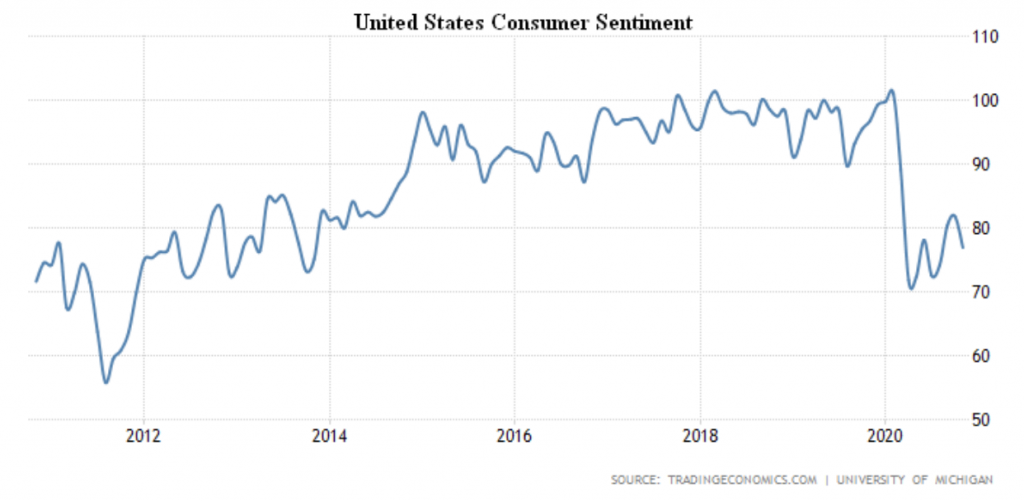

Market sentiment of Americans is the worst in 3 months, much closer to the low of spring-summer than to the peak of the beginning of the year:

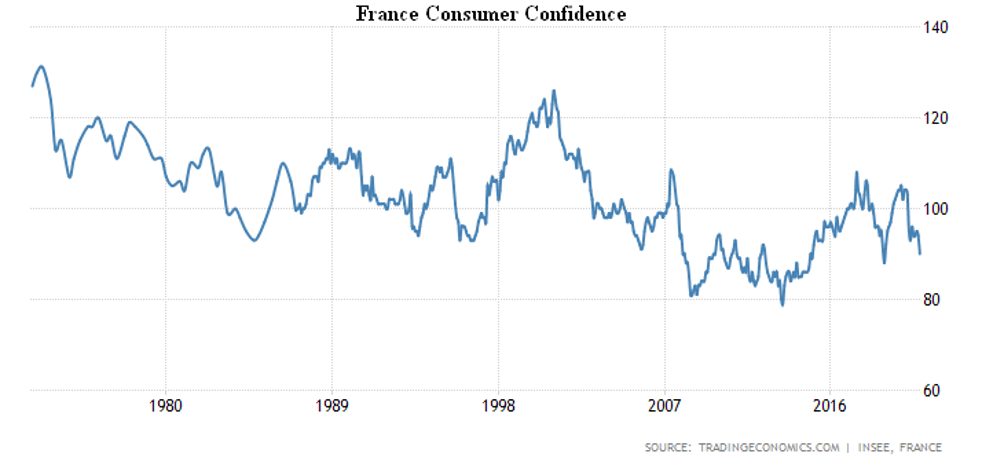

Market sentiment of Germans is the most gloomy in 5 months, Italians – in 6 months, as well as residents of the Euro Area in general. The French are record-holders, their consumer confidence is the lowest in two years, and the level of pessimism is higher than in the spring and summer:

Jobless claims in the US have peaked in five weeks, and Brazil’s unemployment rate is simply a record high.

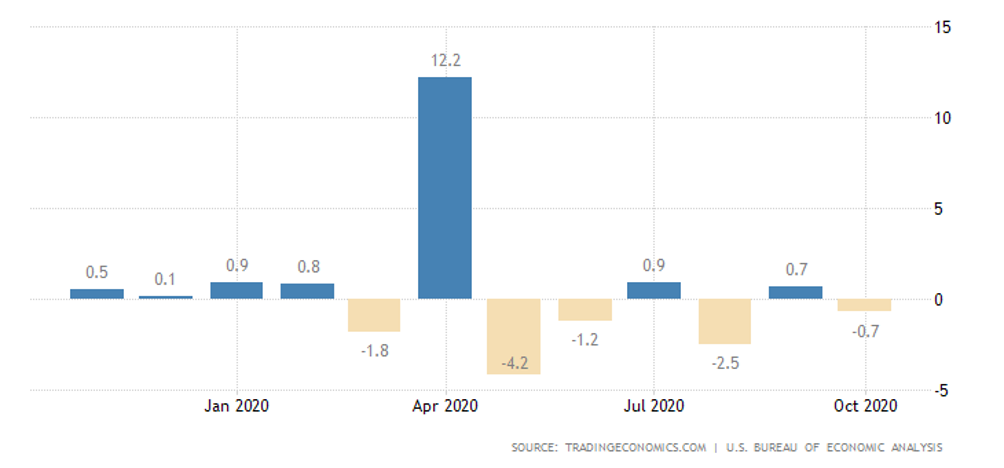

Monthly dynamics of personal income in the US is negative again:

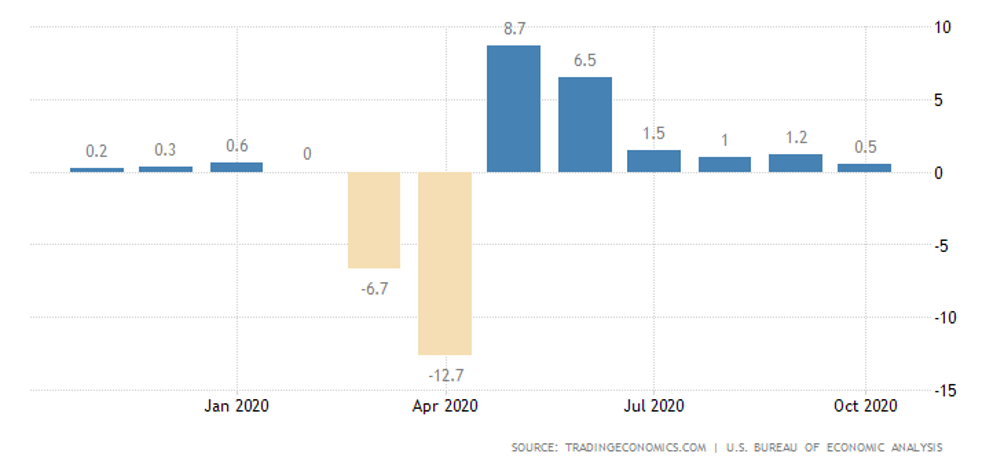

Personal spending is still positive, but minimal for six months:

The retail balance in Britain is the worst in 5 months, -25%.

The Central Bank of South Korea has left monetary policy unchanged, and expects GDP to fall by 1,1% this year.

Summary: The stimulus measures have lost their effectiveness and the economy has begun a steady recession. Recovery is still ongoing in some places, but the downturn is already prevalent. And the growth is constantly slowing down. Both consumers and producers react accordingly – market sentiment is deteriorating.

As already noted at the beginning of the review, these circumstances are coupled with the growth of financial markets, which in this situation is by no means a positive development. Very rough economics can be imagined as a human body, and the growth of muscles on one left hand while exhausting the rest of the body doesn’t look very pretty. And it testifies to serious problems, actually, a structural crisis.

The main question is, how long can this situation continue? Sooner or later, such a situation will inevitably trigger an explosion – either a financial bubble (financial collapse) or a social explosion triggered by economic problems. Which cannot but lead to additional economic problems.

Of course, it is not in our competence to analyse social and political processes in different countries of the world, it is not in our professional interest. We are modeling global economic processes, and we are reporting accordingly. The first one has already been published, and the next one, focusing on Germany’s economic outlook, will appear in the coming days. They are the ones that will explain how the situation will evolve in the medium term.