Time period: April 30–May 6, 2022

Top news story. Undoubtedly, the main news of the week was the decision of the US Federal Reserve to raise the interest rate by 0.5 points. We have written in the previous review about how the US was put in trouble with this decision, but for now, what did the head of the Fed, J.H. Powell, say as a result:

- A rate hike to 0.75% will not be considered by the Fed;

- According to the Fed, the neutral rate is about 3%;

- The 0.5% rate increase may be realized at the next two meetings, further on 0.25%, bringing to 2.75% by the end of 2022 (the next meetings are 15 June, 27 July, 21 September, 2 November and 14 December);

- Balance-sheet reduction plan: start from 47.5 billion on June 1, 2022, then 63.5 billion from July 1, 79.5 billion from August 1 and 95 billion from September 1;

- There is no certainty about the timing of the rebalancing after September 1 — all this can be quickly closed if there are risks to the system, which, in the Fed’s view, represent a fall in markets, a threat to financial stability (credit spreads, demand for debt instruments, economic recession).

Herewith:

- The Fed is determined to combat inflation, maintaining price stability is the Fed’s top priority;

- The Fed has a fully staffed arsenal to fight inflation;

- We see no recessionary risks. There is a strong possibility that we can reduce inflation without causing serious job losses;

- The Fed does not expect the economy’s confidence in the Fed to weaken and does not expect a spiral of inflation, but expects inflation to decline from the second quarter (this is exactly what the Fed repeats at every meeting, a year ago they too thought that inflation would start slowing down at the end of 2021, it turned out the other way around);

- If the need to raise rates continues, we will continue to do so.

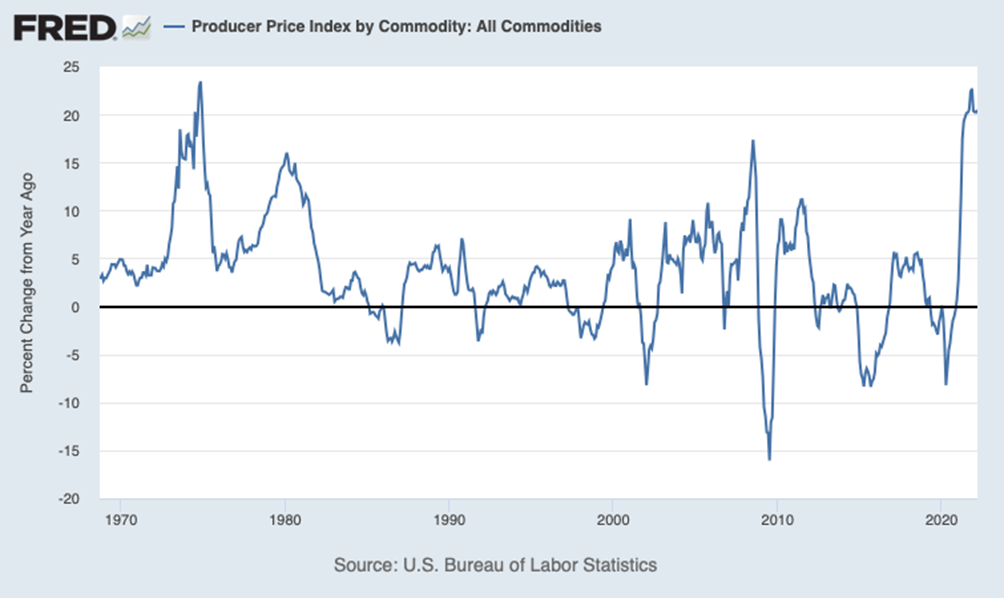

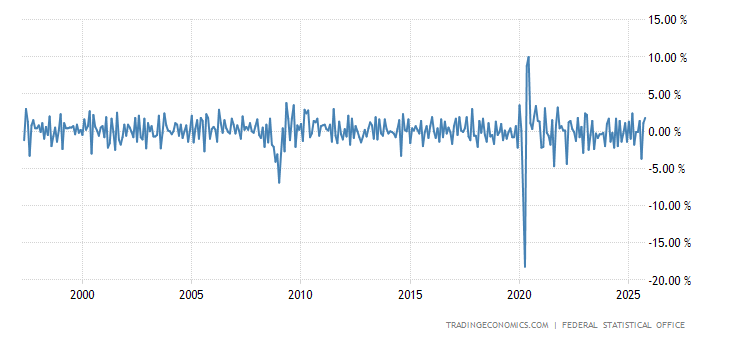

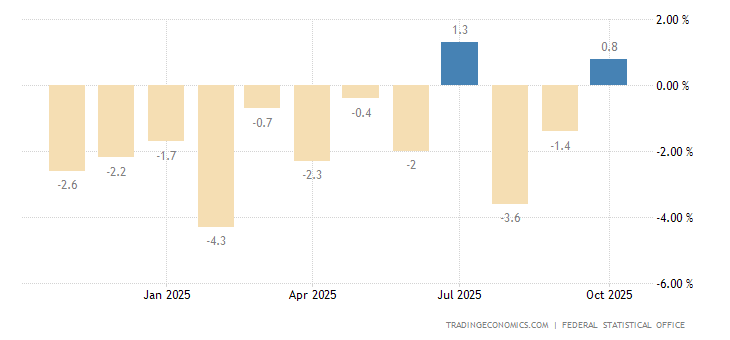

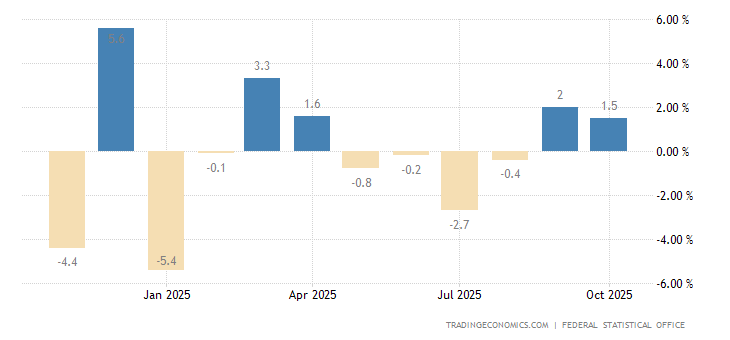

It is difficult to comment on this. If the Fed is armed to the teeth (and in our opinion it is long gone, as we noted in the last review), how did it allow inflation to reach a 40-year high and real debt rates to be record negative? What have they been doing in the last two years? The US economy has been in decline since at least the fourth quarter of last year, if we are honest about inflation, see the chart:

In this regard, the “neutral” rate level (that is, providing at least zero real yield on debt instruments) is at least 12-15 percent! Okay, let’s say 8%. But this is two and a half times more than the claimed 3%. And who, with such a real return (very negative) will be ready to invest in debt instruments? With real assets growing?

- Real rates for 10 years

- Real federal funds rates

And we will not even mention here the classic spells that the economy is strong, demand is strong, supply is strong, the Fed is strong, markets are strong, everything is stabilized, everything will settle down and life will be fun and well-being.

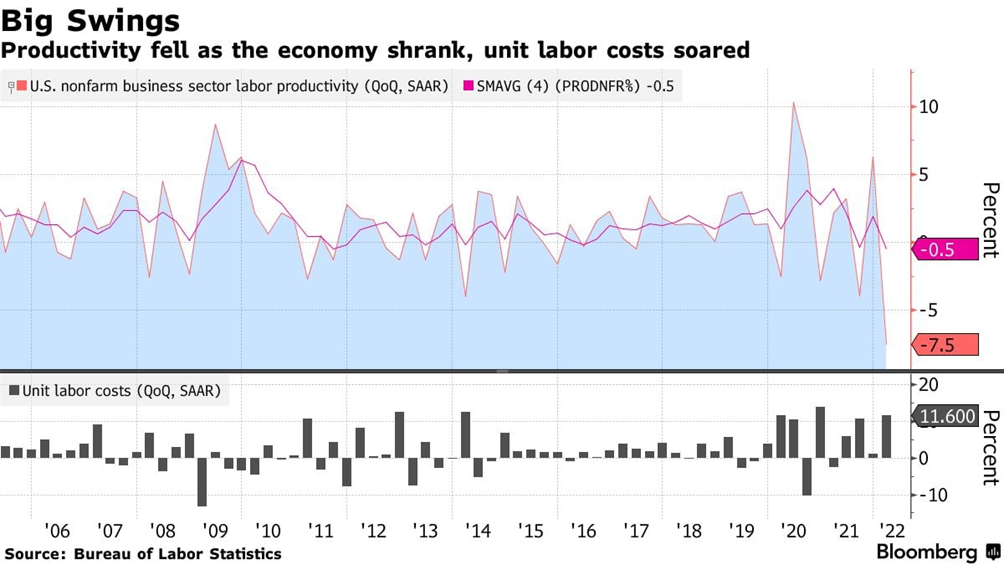

By the way, the markets also did not believe — the labor market collapsed (see the next section), labor productivity decreased in the first quarter to the lowest values since 1947 (on expectations of this particular decision, +0.5%):

The stock market collapsed, Bitcoin collapsed, what to do with household spending (the basics of the economy) — it is completely unclear. Asset buybacks will inevitably lead to even higher debt service costs, reducing household spending. In general, there are no features of a positive scenario (and we recall that the US economy has reached a steady downward trajectory of about 8-10% per year), and US monetary authorities look terrible.

Macroeconomics

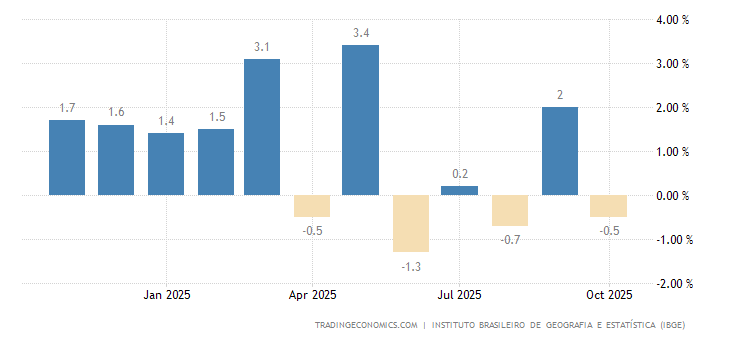

Brazilian industrial production -2.1% y/y, 8th consecutive negative:

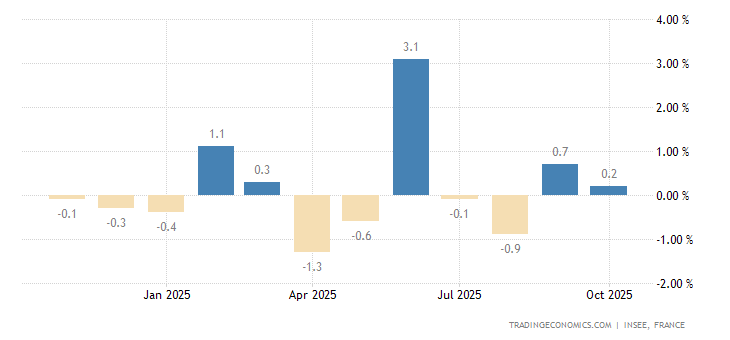

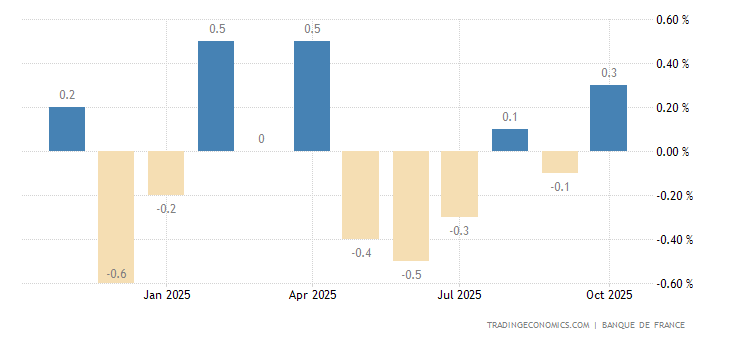

Output in French industry -0.5% per month (2nd consecutive negative):

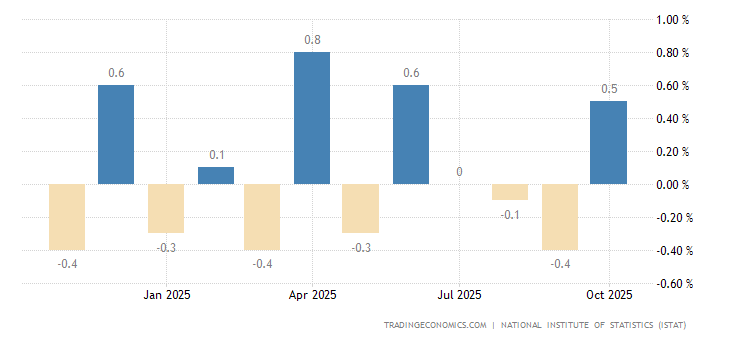

Industrial production in Germany is -3.9% per month, except for two drops in 2020, which is the worst performance since 2008:

And -3.5% per year, the lowest in 13 months:

Industrial orders in Germany -4.7% m/m (2nd consecutive time in red) and -3.1% y/y (annual low):

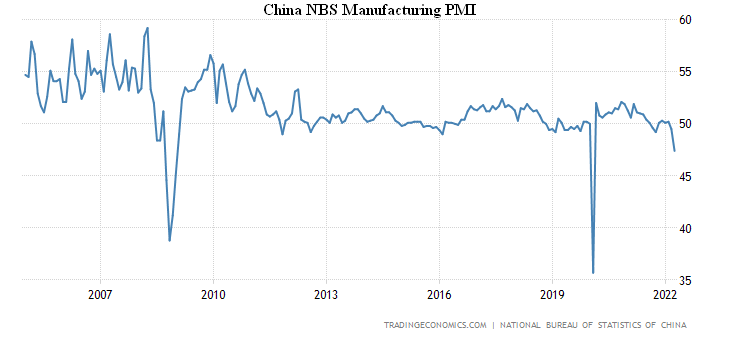

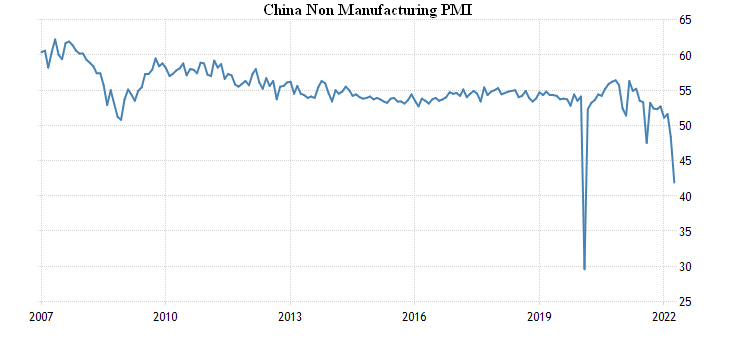

Purchasing Managers’ Index (PMI, the expert index, which shows the conditions in the industry; its value below 50 means stagnation and decline) of the Chinese industry according to official data 47.4 — for all its history was only worse in February 2020 and for four months in 2008:

In non-manufacturing sectors, it’s 41.9 at all — much lower than the 2008-trough and only better than 1 month of 2020:

Independent study confirms the figure, in production 46.0:

In the service industry, there are 36.3:

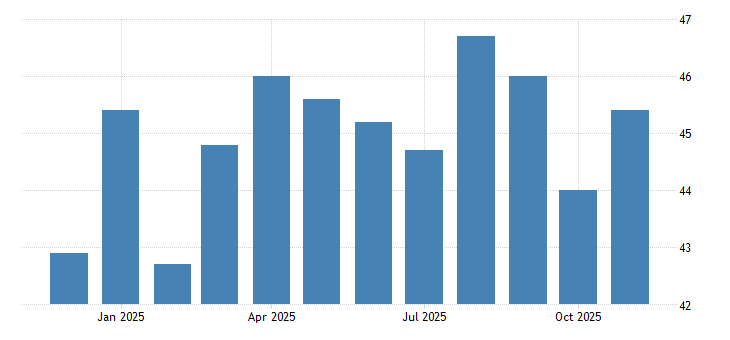

US industry PMI is at its lowest in 9 months:

United States ISM Purchasing Managers Index

The Euro Area manufacturing PMI is the weakest in 15 months, and the output is the weakest in 22 months:

The Euro Area construction PMI is at the 7-months trough and stays in the stagnation zone (50.4 points):

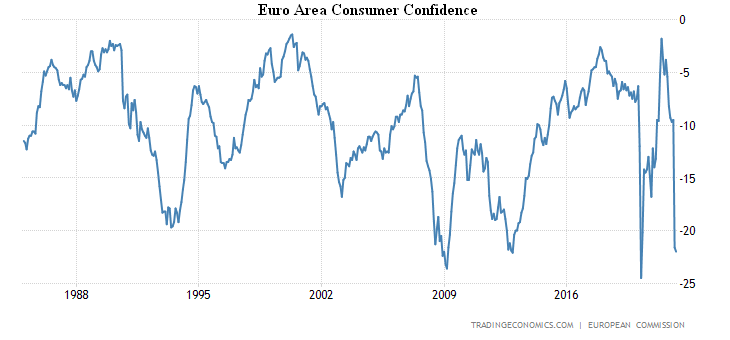

Economic sentiment in the Euro Area hit a 13-month low:

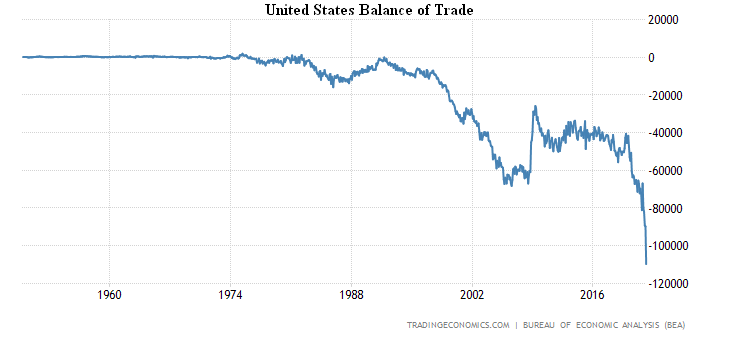

US balance of trade hits record as imports skyrocket:

This situation means that domestic production has become so expensive that it is no longer able to compete with imports in the face of falling household incomes.

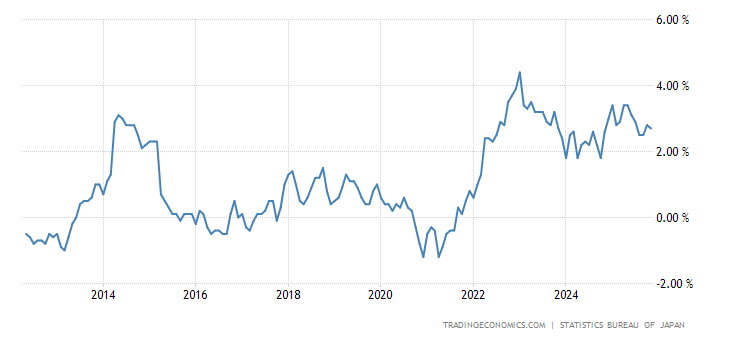

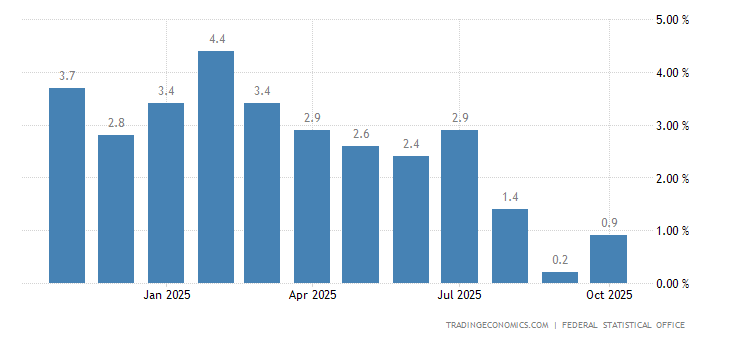

CPI (Consumer Price Index) Tokyo area +2.5% per year, peak since 2014:

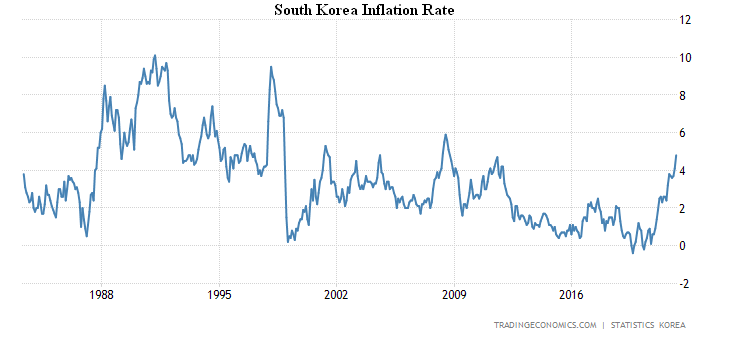

CPI South Korea +4.8% per year, at it’s most since 2008:

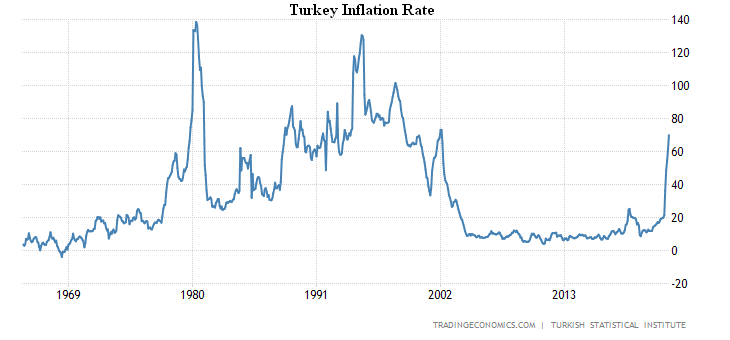

The CPI of Turkey was 70.0% per year and reached a 20-year high:

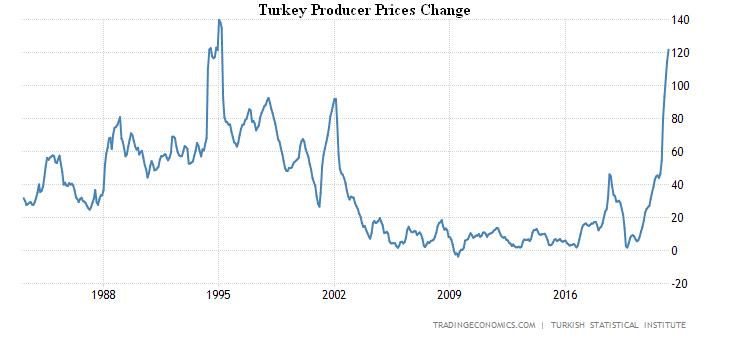

Turkey’s PPI (Producer Price Index) +121.8% per year at its peak since 1995:

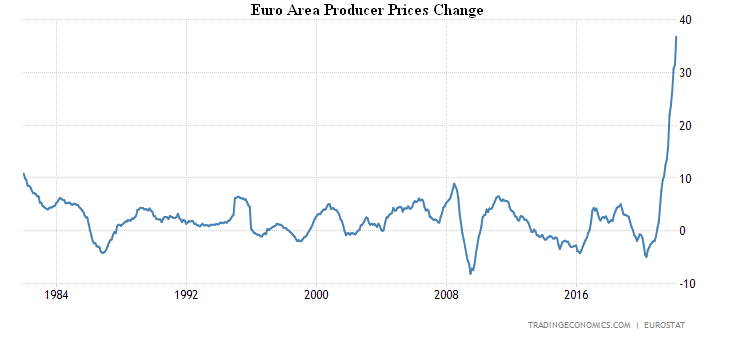

The Euro Area PPI +36.8% per year, this is a record for 40 years of survey:

Unsurprisingly, The Euro Area consumers are extremely pessimistic for the year, and pessimism is almost record —

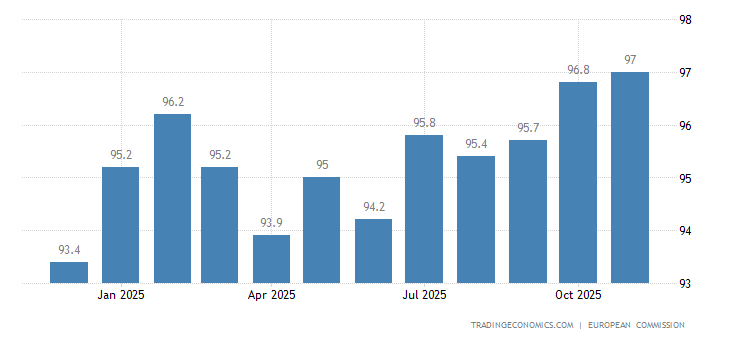

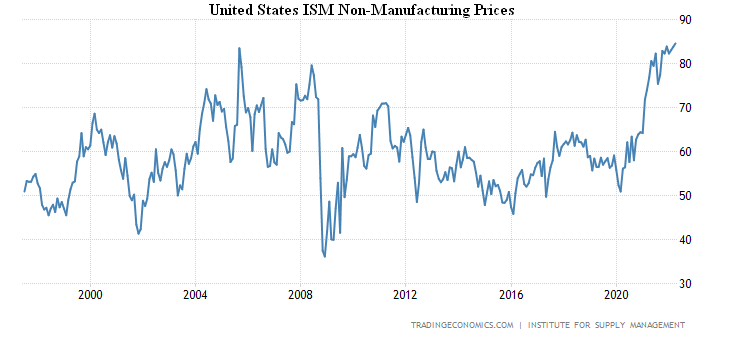

The US non-manufacturing prices are the highest in 25 years of data acceptance (84.6 points):

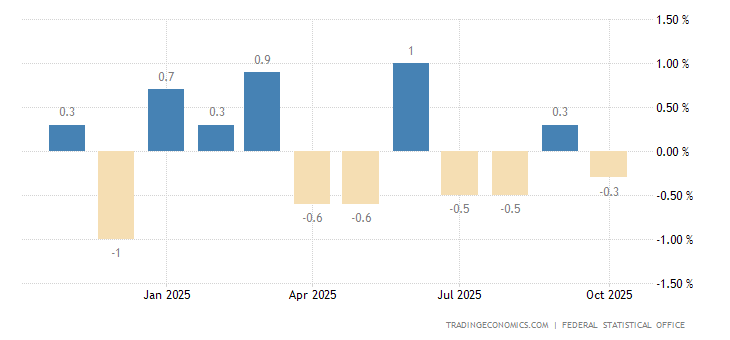

Retail sales in Germany -0.1% per month — the 3rd negative in the last 4 months:

And -2.7% per year, which is the worst performance in 14 months:

In retail sales in France, also the 3rd monthly loss in 4 months (-1.9%):

In Italy -0.5% per month — the 2nd negative in 3 months:

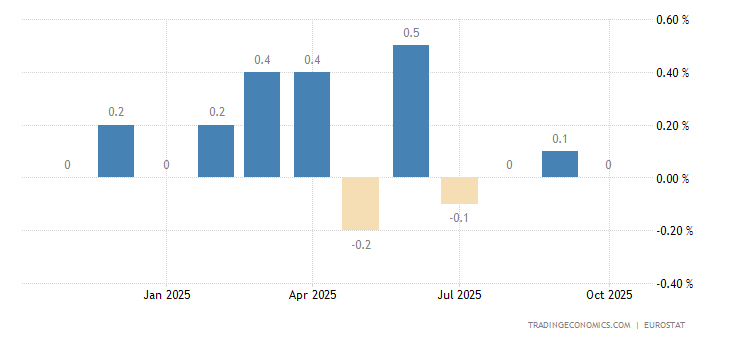

Retail sales throughout the Euro Area as a whole also went into the red (-0.4% per month) —

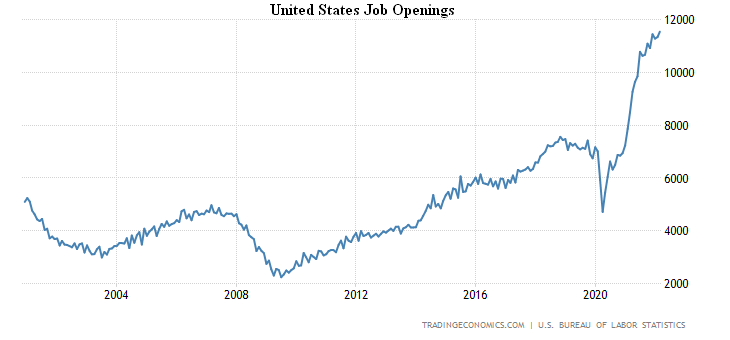

The number of job openings in the United States is record, as is the number of employees who quit:

Companies’ annual staff reduction plans are extreme —

And initial jobless claims — for 2.5 months:

Employment in the private sector in the United States (ADP survey) is only +247 thousand, this is a 2-year low:

For the first time since 2000, the Fed hiked the rate by 0.5% at once, from June 1 it will begin to reduce the balance.

The Central Bank of Australia raised the interest rate for the first time since 2010 — by 0.25% to 0.35%.

And the Central Bank of India did this for the first time since 2018, by 0.4% to 4.4%.

At the same time, the Central Bank of Brazil increased the interest rate for the 10th consecutive time, by 1.00% to 12.75%.

The Bank of England did it for the fourth time, 0.25% to 1.00%; 3 out of 9 members voted for 0.50%.

The Saudi Arabian Central Bank increased the rate by 0.50% to 1.75%.

Summary. Macroeconomic data indicate a rapid deterioration of the situation, both in the European Union and the US, and worldwide (China). This is despite the fact that most of the data on industries are obtained in price terms, which, given the undervaluation of inflation, significantly improves the overall picture.

At the same time, the growth of Chinese exports to the US was supposed to support China’s economy. But since the money from these exports is not directly available to China, and China’s economy is already overheated, in fact, we are likely to see a policy of a managed decline in the Chinese state’s investment activity. This means that the leadership of that country is waiting for the US to step up sanctions against itself, perhaps given the need to speed up the resolution of Taiwan’s problem.

No positive action is seen in this situation. The Fed’s proposals cause nothing but serious pessimism — no real problem has been discussed, all the reasoning is rather general and impossible. In the EU, the situation is even worse, and there is no doubt that, given the Fed’s decision on the rate, next week’s data will be awful.

Most likely, the Fed will try until the next meeting not to raise issues of deterioration of the situation, and then, raising the rate by another 0.25% in June, to postpone the situation for the summer. But it is possible that this simply will not work, because the negative processes are too fast. In fact, this is the main intrigue of the next two months: will the US monetary authorities be forced to take any additional measures, and if so, what will be their nature? We will try to answer this question in the coming weeks, and in the meantime we congratulate our readers on the upcoming Victory Day and wish them a warm spring weekend and a productive working week!