Time period: 23-29 October 2021

Top news story. As we know, in recent months, consumer inflation in the US has been by far behind industrial inflation. But this situation cannot last long: either the former will increase or the latter will decrease. It is not yet clear, but there are signs that consumer inflation is likely to increase.

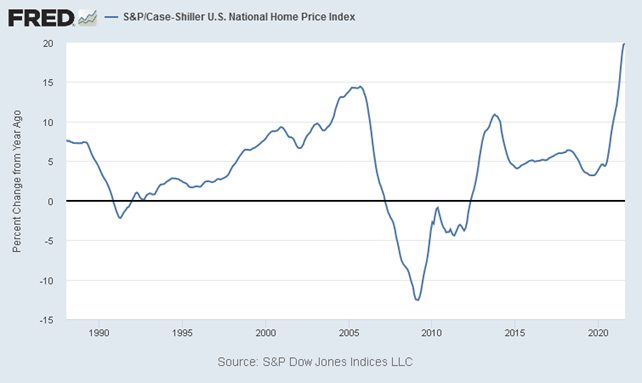

In particular, in our opinion, the highlight of the week was the rise in house prices. Of course, houses are not consumer goods, they have a completely different pricing mechanism, but they do play a very important role in the household economy. So that’s a very bad sign.

Note that the related indicators have not improved (see the following section), so it is a matter of stable pattern, not accidental discharge.

Macroeconomics

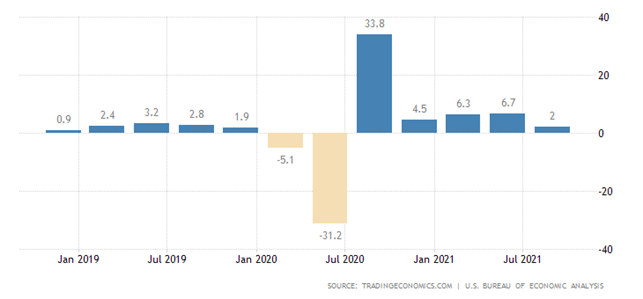

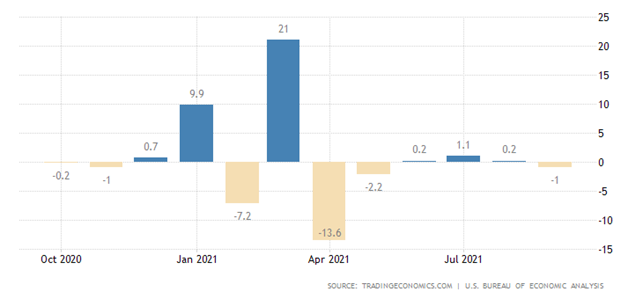

US GDP growth slowed to +0.5% QoQ in Q3. Given the figures provided by US statisticians a few months ago, the contrast is striking:

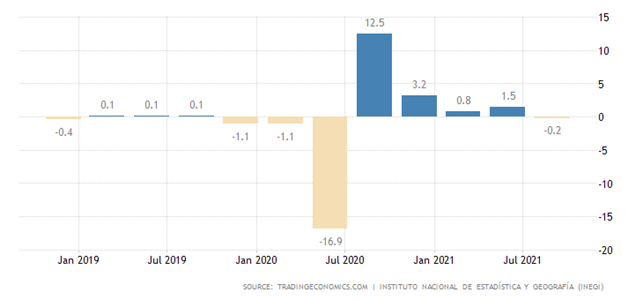

Mexico’s GDP (and its economy is very close to that of the US) has even gone into quarterly negative:

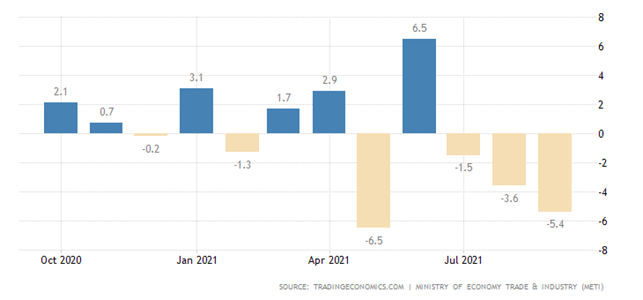

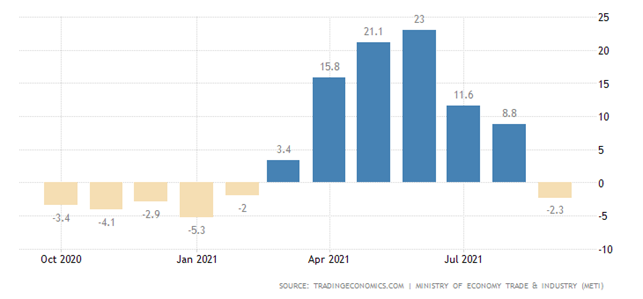

Industrial decline in Japan is accelerating – the 3rd consecutive monthly negative, this time -5.4%:

As a result, for the first time since March, the annual decline also returned (-2.3%):

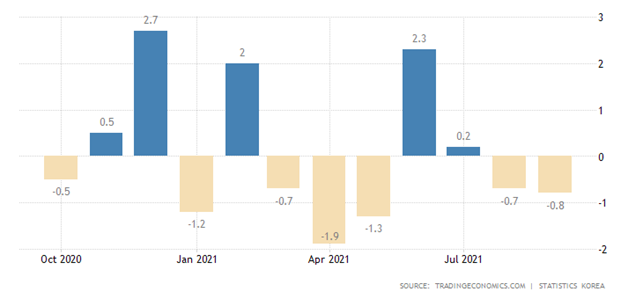

South Korea’s industrial production has been in decline for two consecutive months, of the last seven months five in the red zone:

This brought the annual performance back to negative for the first time in a year:

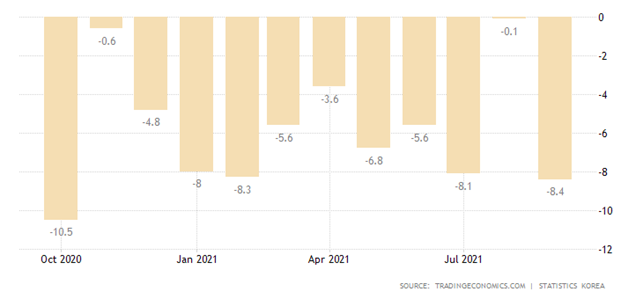

South Korea’s construction industry output has been stuck in negative YoY for a whole year:

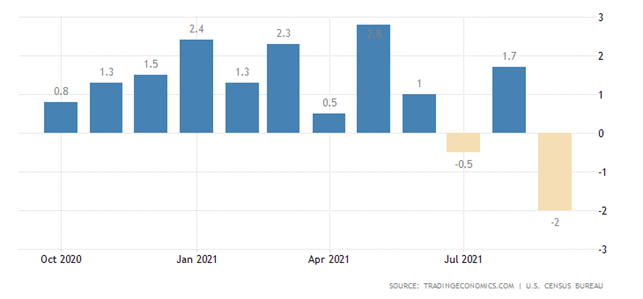

Orders for durable goods (excluding defense goods) in the US -2.0% per month, which is the lowest since April 2020:

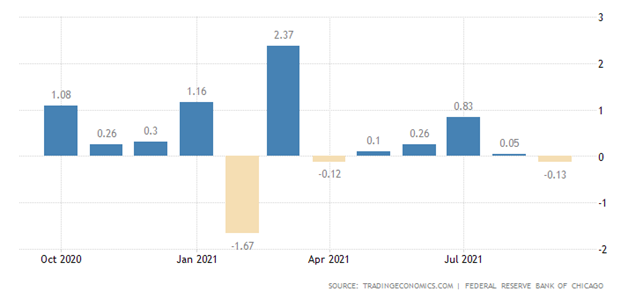

United States Chicago Fed National Activity Index went into a red zone right to its seven-month trough, with production economic component collapsing:

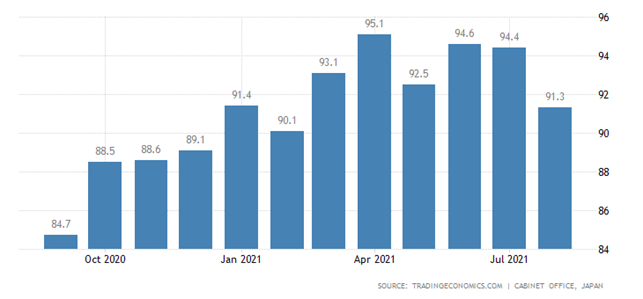

Leading and coincident indicators in Japan are at their lowest levels in half a year:

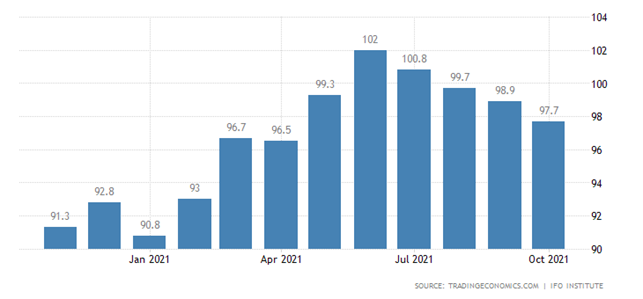

IFO Germany’s business climate is the least favorable in six months:

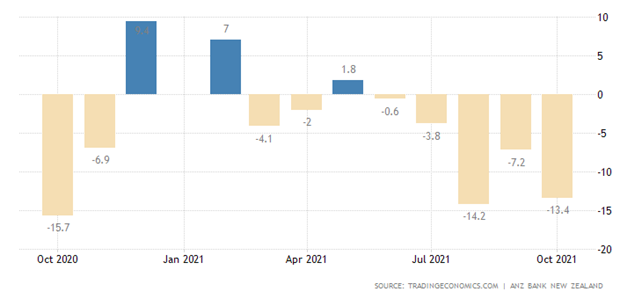

The Business Confidence Index is a macroeconomic indicator that shows the level of confidence of business elites in the stability of a country’s economy. One could conceivably accept its negative value as an indication that more than half of the representatives of the business community see the future of the economy as unfavorable.

In New Zealand, The Business Confidence Index shows the 5th consecutive negative:

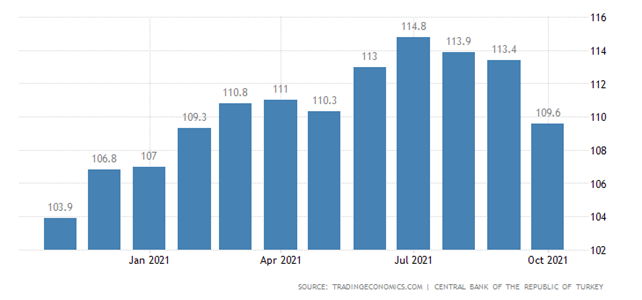

Business confidence in Turkey is the worst in eight months:

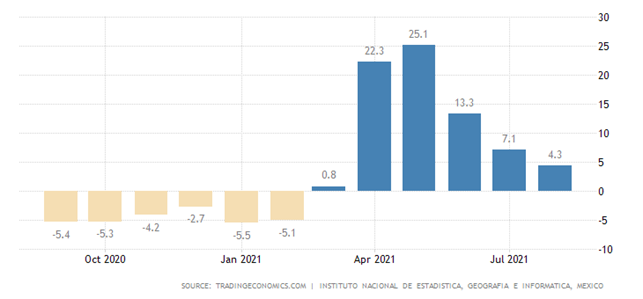

Economic activity in Mexico -1.6% per month and +4.3% per year (the lowest in 5 months):

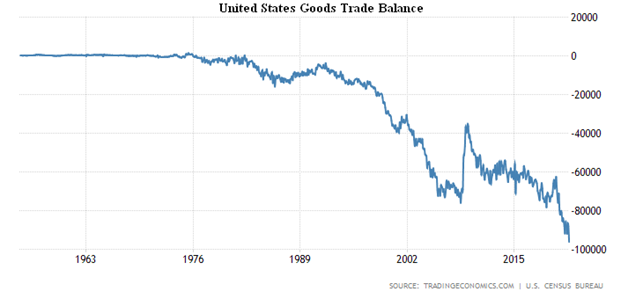

Against the backdrop of a collapse in exports, the US goods trade deficit set a record in 67 years of observation:

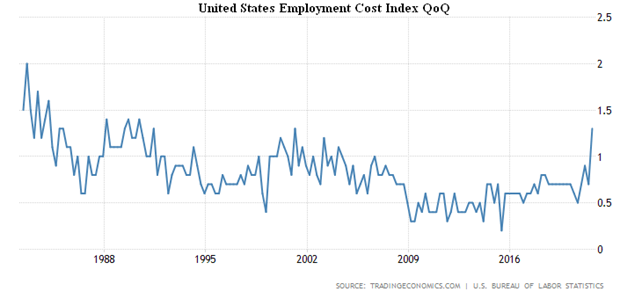

In Q3, employment cost in the US rose to its highest level in a quarter since 1991:

It should be noted that this is an indirect indication of rising consumer inflation.

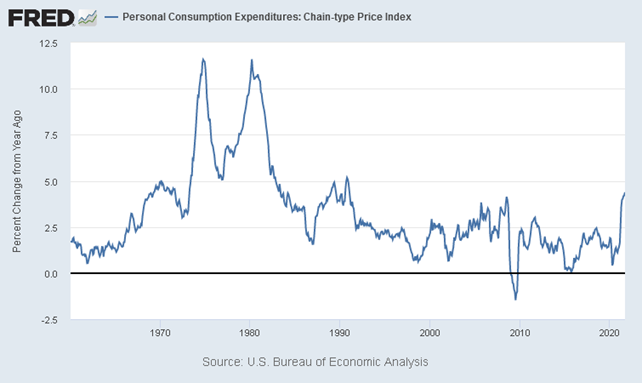

Chain-type index of personal consumer expenditures in the USA +4.4% per year, which is the highest since January 1991:

CPI (Consumer Price Index) of Italy +2.9% per year, at its peak since 2012:

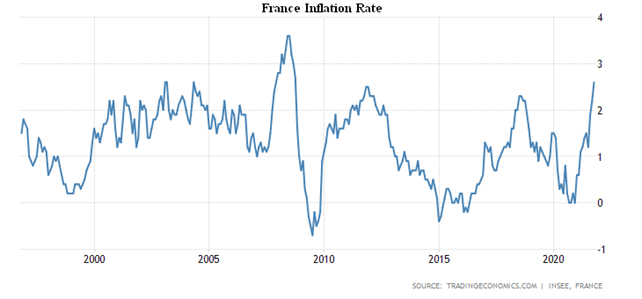

CPI of France + 2.6% per year, at the top since 2008:

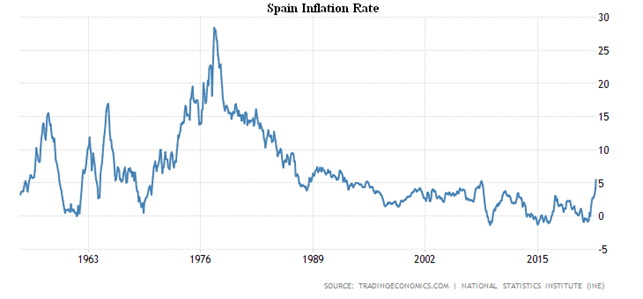

CPI Spain +5.5% per year, the highest since 1992; monthly surge (+2.0%); this has not been the case since 1986:

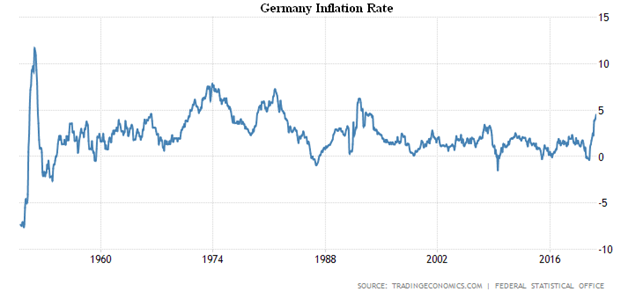

CPI in Germany + 4.5% per year, a record since 1994:

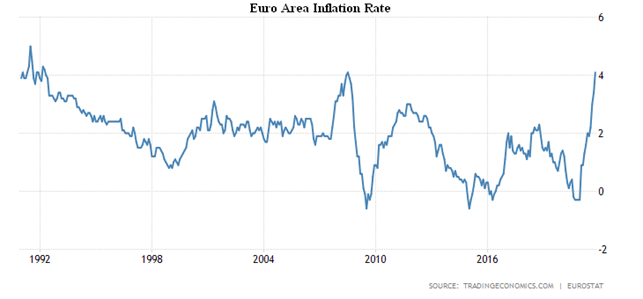

The Euro Area CPI +4.1% per year, which repeated the top since 2008, until then such values were in 1992:

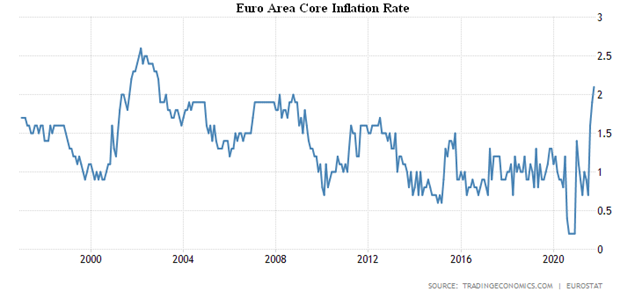

The Euro Area core inflation rate (excluding highly volatile components) +2.1% per year – the top since 2002:

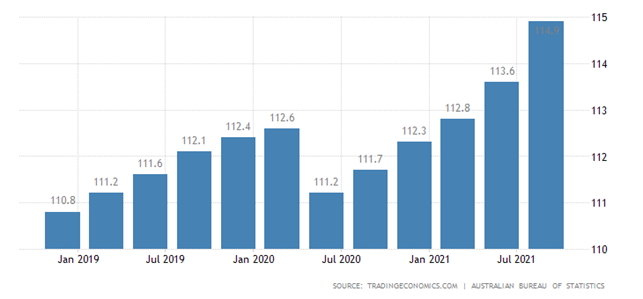

PPI (Producer Price Index) of Australia in Q3 + 1.1% QoQ – peak since 2013:

And +2.9% per year – the maximum since 2011:

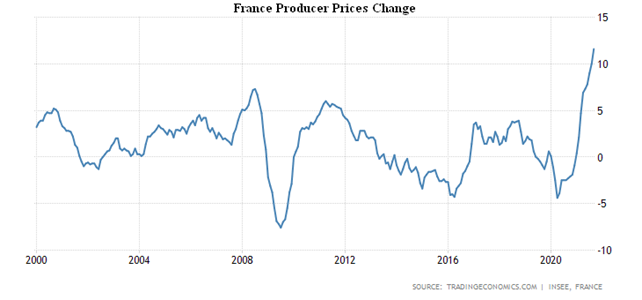

France PPI +11.6% per year – top 21-year observation:

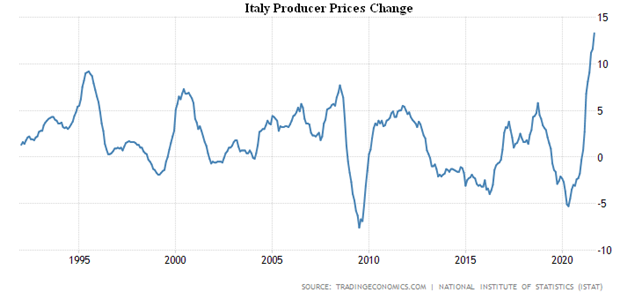

Italian PPI + 13.3% per annum – 31-year peak:

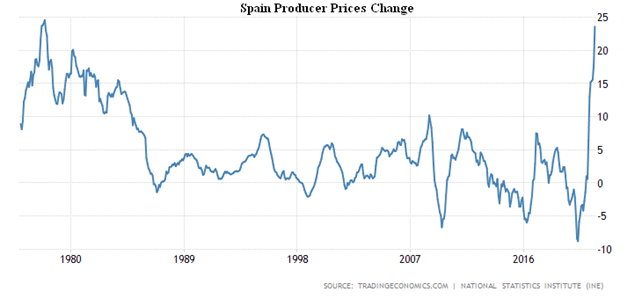

Spain PPI +23.6% per year, this is a 44-year-old peak and very close to the historical high:

Import prices in Germany +17.7% per year at their peak since 1981:

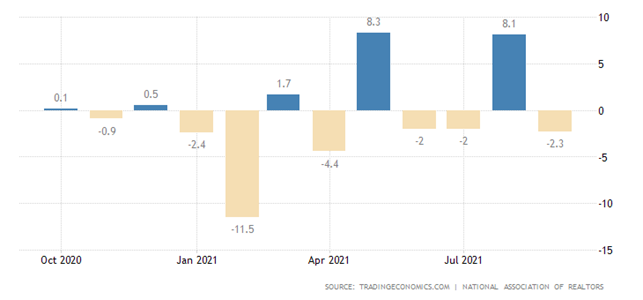

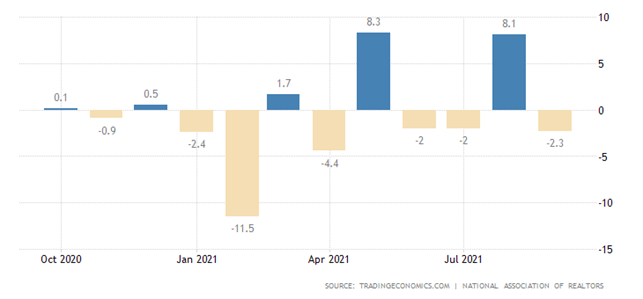

US pending home sales -2.3% per month:

And -8.0% per annum, this is the 4th consecutive annual negative:

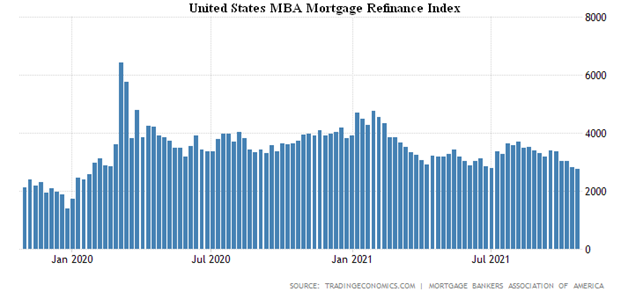

The growth in mortgage applications in the United States is almost non-existent after massive collapses. Refinancing at the trough from January 2020:

The French are as pessimistic as possible in five months:

And their expenditures are reduced:

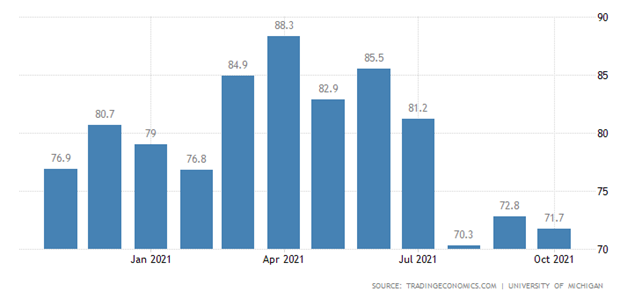

American sentiment is very close to a 10-year low:

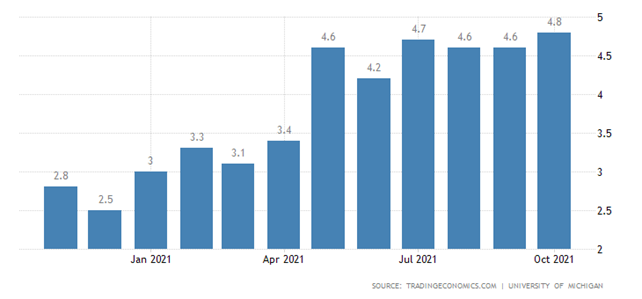

And their inflationary expectations have peaked since 2008:

Private income in the United States is -1.0% per month, and this is with underestimated inflation!

The Central Bank of Canada completed QE, promising to hold current rates until mid-2022 instead of 2023 earlier.

Brazilian Central Bank rates skyrocketed by 1.50% to 7.75%.

The ECB left everything unchanged, as did the Bank of Japan.

Summary. The crisis is intensifying and gaining power – that is obvious even to a completely unsophisticated observer. It is clear that this will drastically reduce consumer demand, which in turn will inevitably have a detrimental effect on industry.

In other words, the crisis is entering a new round. It should come as no surprise that structural imbalances are becoming more pronounced (see the previous week’s Review of logistics in international trade). In particular, costs of energy carriers are constantly rising. The Eurasian Forum in Verona paid close attention to these issues: the discussion was detailed and without ideological and propagandistic clichés. You can, for example, note the very systematic report of the head of Rosneft I. Sechin, so you can omit this topic here.

In sum, it is with some sadness that we anticipate further major setbacks in the world economy, for there is as yet no evidence of what could halt the structural downturn. Well, we wish the readers of our Reviews not to lose heart and to do business successfully!