Period: 9 – 15 January 2021

Top news story: The hero of the week was the Alibaba Group, which introduced a new electric car. The trick here lies not only in the fact that this car surpasses Teslas electric car in all respects, but there are two other things. The first was Teslas record capitalization in recent weeks. The second was that the Chinese explained that they have a vast domestic market, and it is impossible to supply everyone with batteries. Therefore, in the line for batteries, all other manufacturers are placed strictly under Chinese manufacturers.

Obviously, this is, to a large extent, a response to US pressure, which, as it became clear, J. Biden can do a little less, while generally staying the course of D. Trump. But it perfectly illustrates the continuing chaos in the US stock market, which is about to end. Chaos must end with all its consequences, including the beginning of an adequate valuation of all companies. This estimate may be somewhat pessimistic.

Macroeconomics

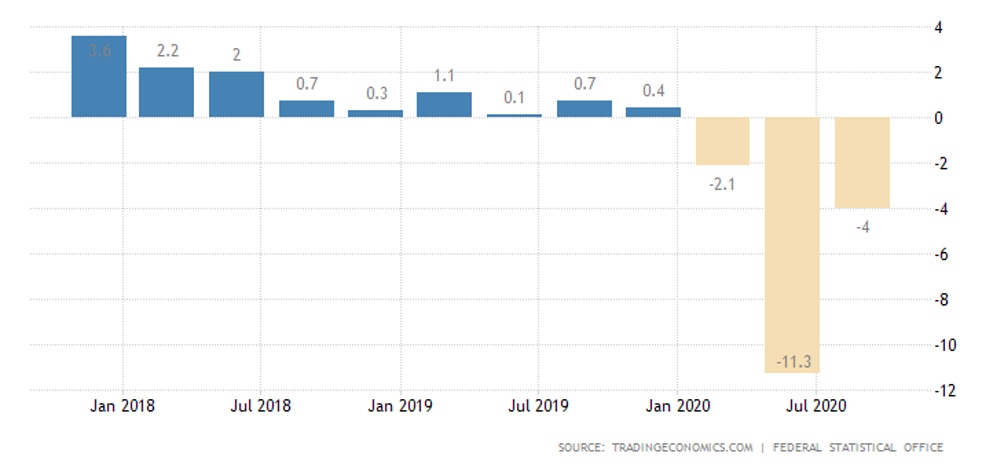

The statistical authorities started issuing the final results of the previous year. Germanys GDP slumped by 5,0% in 2020:

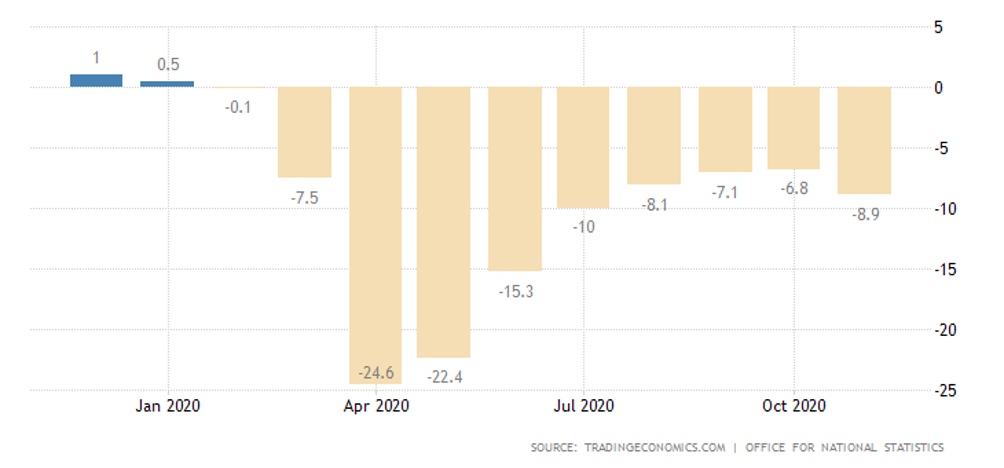

Britains aggregate GDP is not yet in place, with a 2,6% monthly fall in November, the annual recession the strongest in four months (-8,9%):

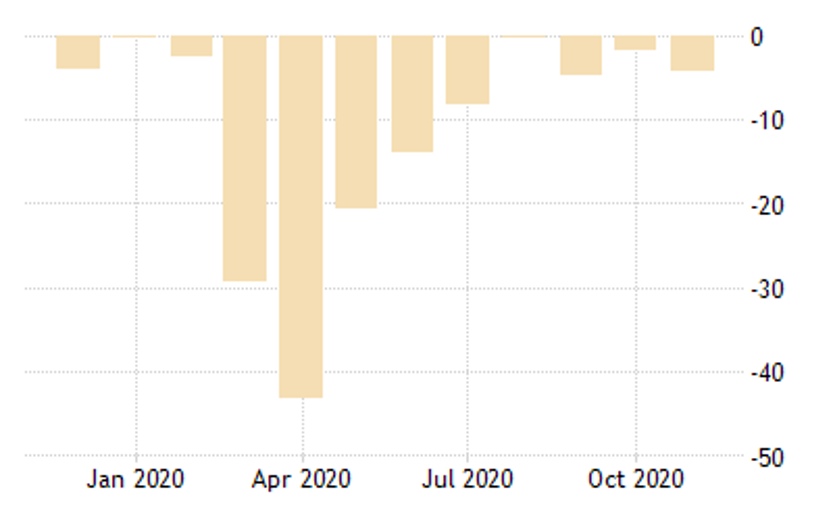

Industrial production in Spain is the weakest in three months (-3,8% per year). Italy is also experiencing a deterioration:

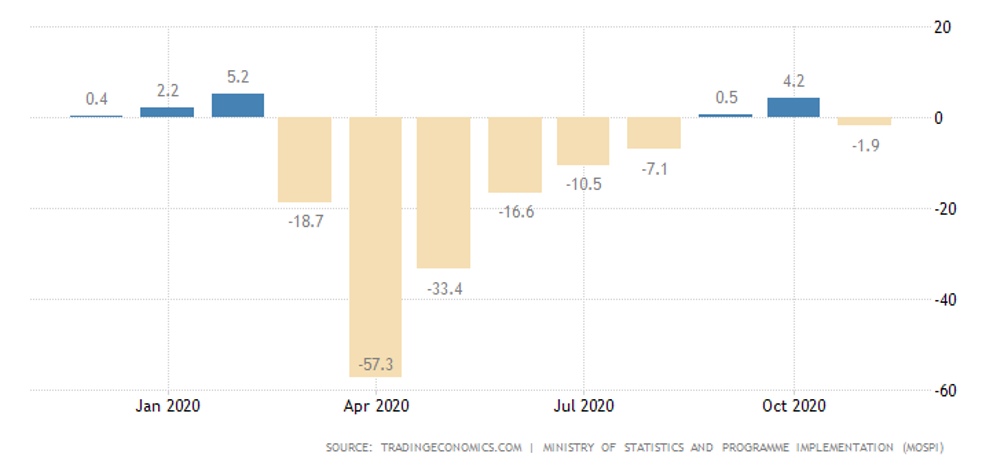

In India, output has gone down a year again:

Some setbacks in Mexico as well.

United States NY Empire State Manufacturing Index worst since June:

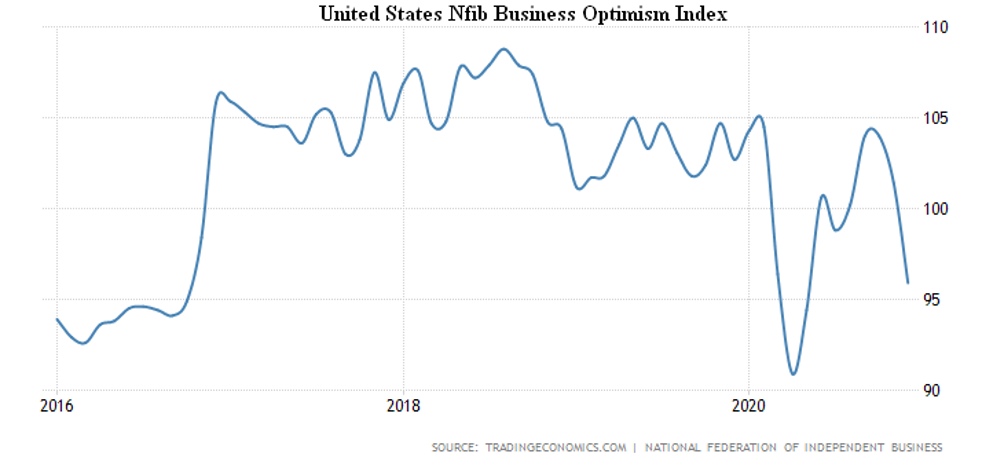

The US Small Business Optimism Index is at the since May:

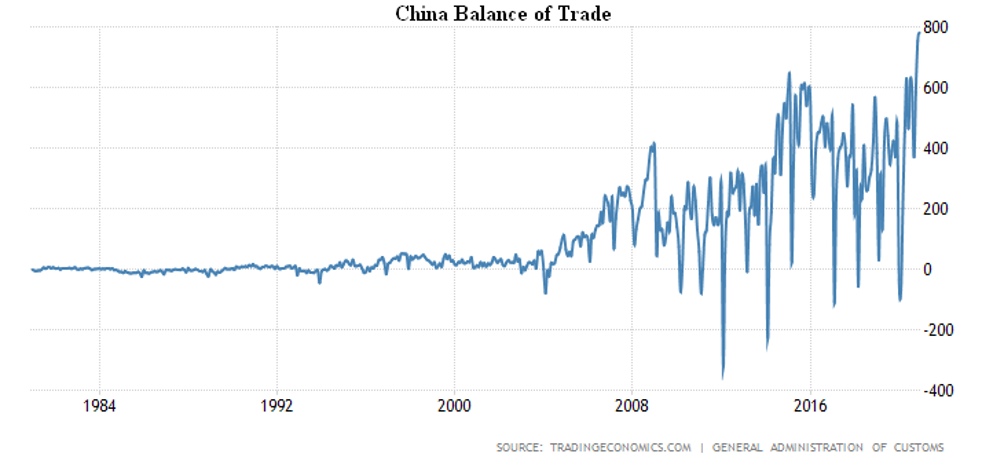

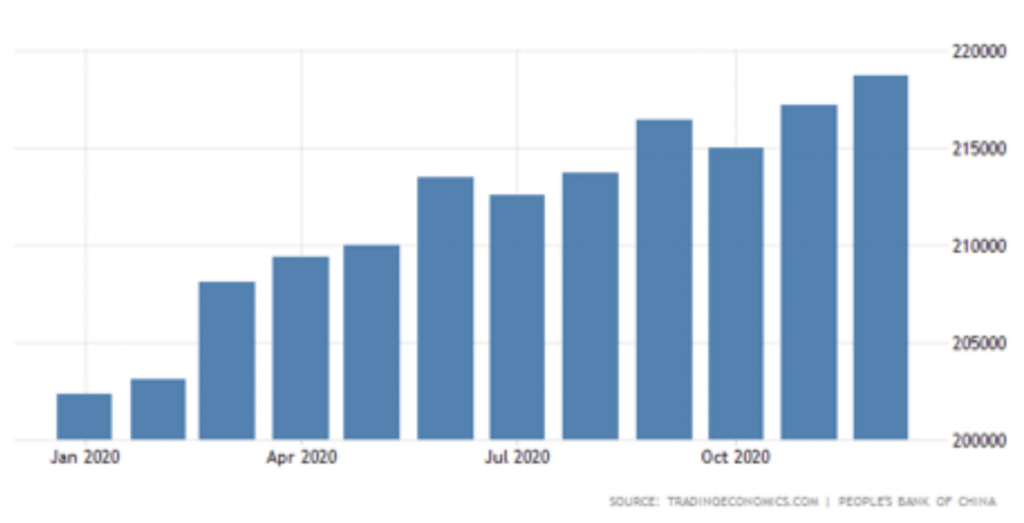

Chinas trade surplus is record:

One wonders why? We expect that, against the backdrop of quarantine and other problems, local products are being replaced by cheap Chinese counterparts. This, of course, does not improve Chinas image in the US, the EU, and many other countries. Given rising social tensions, mainly in the United States, no leadership can ignore this fact. Accordingly, attacks on China will intensify, as we noted in the first section of our review.

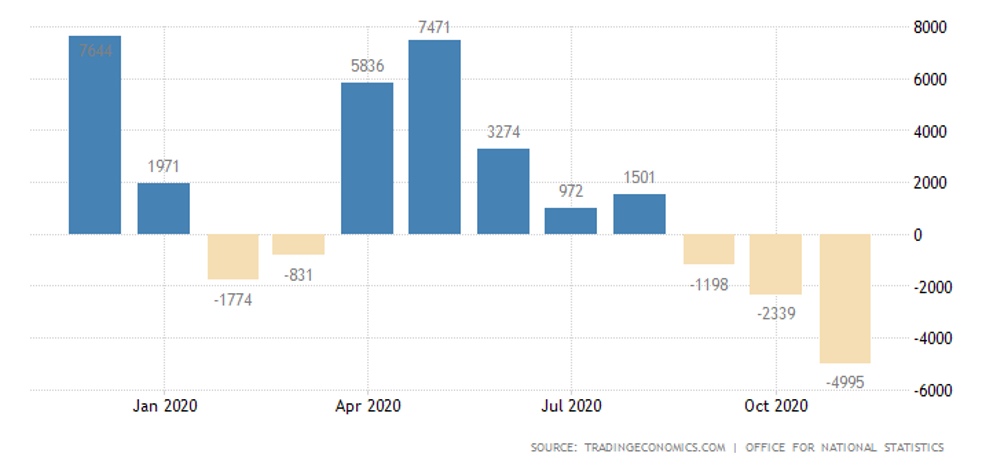

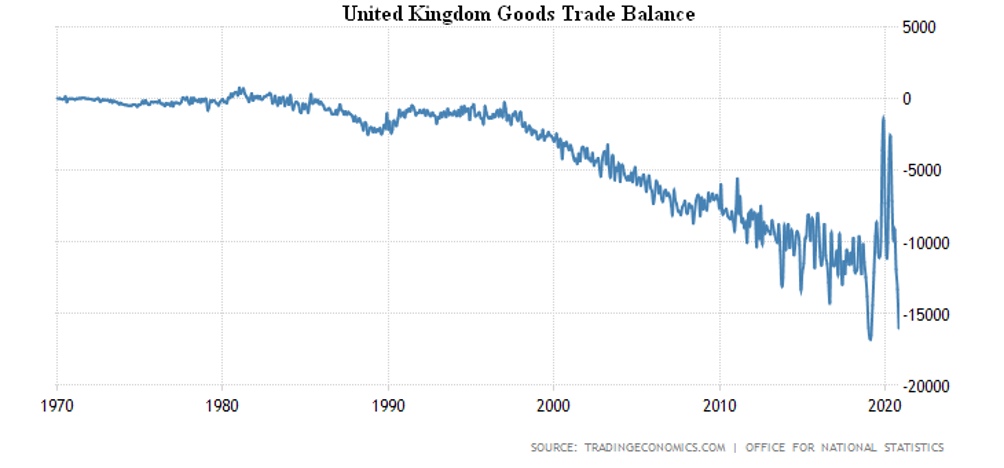

Britains trade deficit has peaked since April 2019:

In particular, the trade deficit is approaching a record for 50 years of observations:

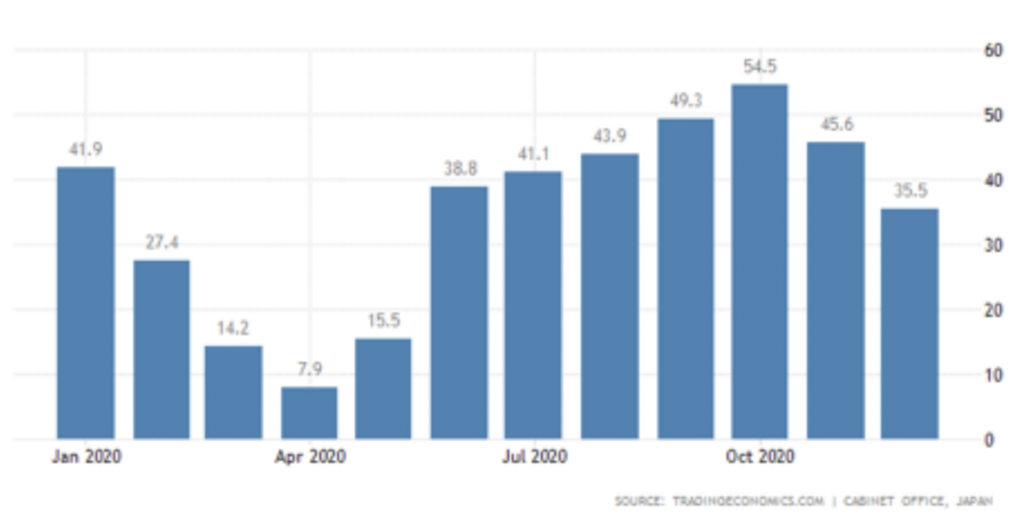

The lowest Economy Watchers Survey in Japan in 7 months:

The growth of the M2 money supply in China slows down more than expected:

As well as housing prices, + 3,8% per year – a 5-year low. Since the M2 is an expanded money supply that reflects the activity of the banking system, it can be concluded that credit exposure in China has declined. The reasons for this are not yet clear. This may be the policy of the Party and the Government, or perhaps it is the lack of entities and facilities for lending. Well deal with it, but the symptom is not the most auspicious.

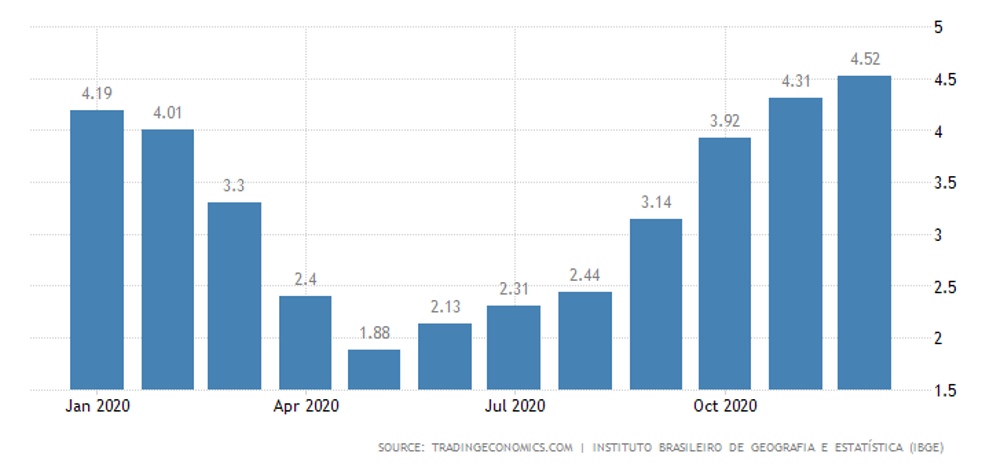

Brazils inflation has peaked since April 2019:

In contrast, in India it is minimal in 15 months. In France, inflation has been minimal for almost five years (0,0% per year), but here it is clear that these are deflation trends, the result of a recession. And central banks are far less active than other countries.

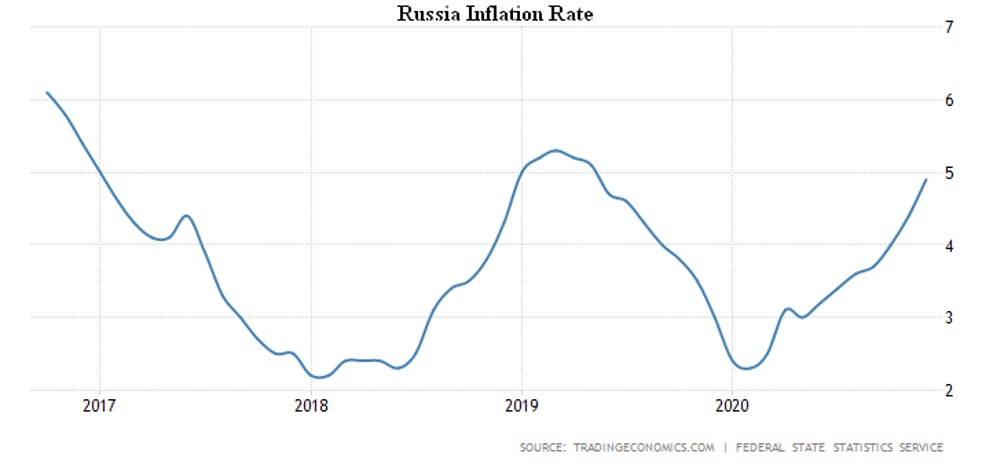

In Russia, the CPI is 0,8% per month (2-year peak) and 4,9% per year (1,5-year and next to 4-year-old):

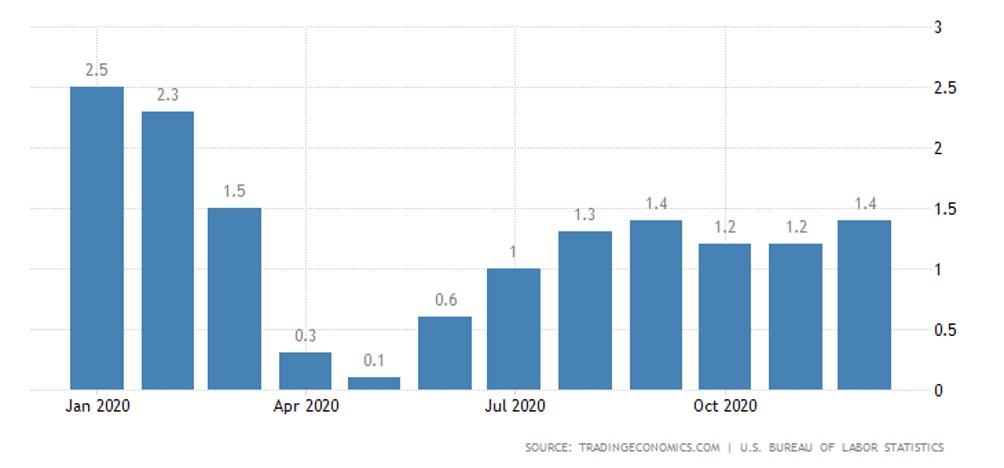

In the United States, the CPI is 0,4% per month (peak from summer) and 1,4% per year (spring):

Unemployment in South Korea has peaked since January 2010 and is near its peak since 2000.

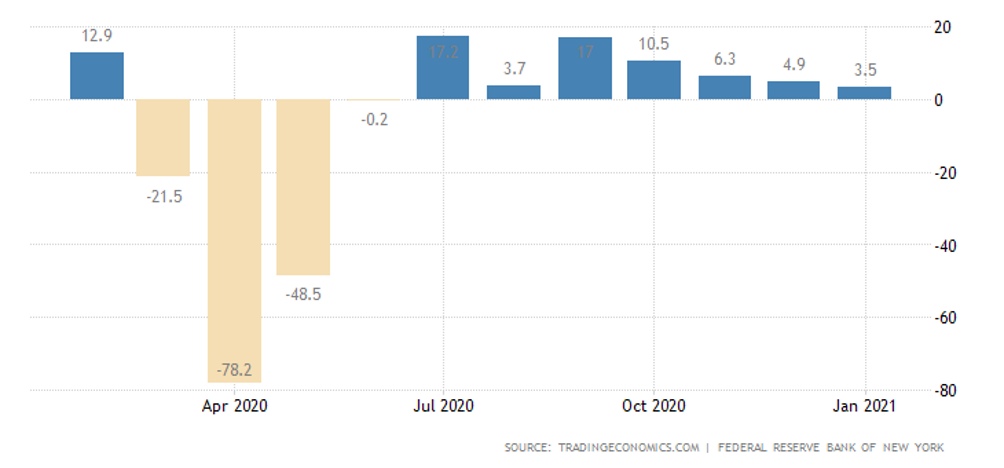

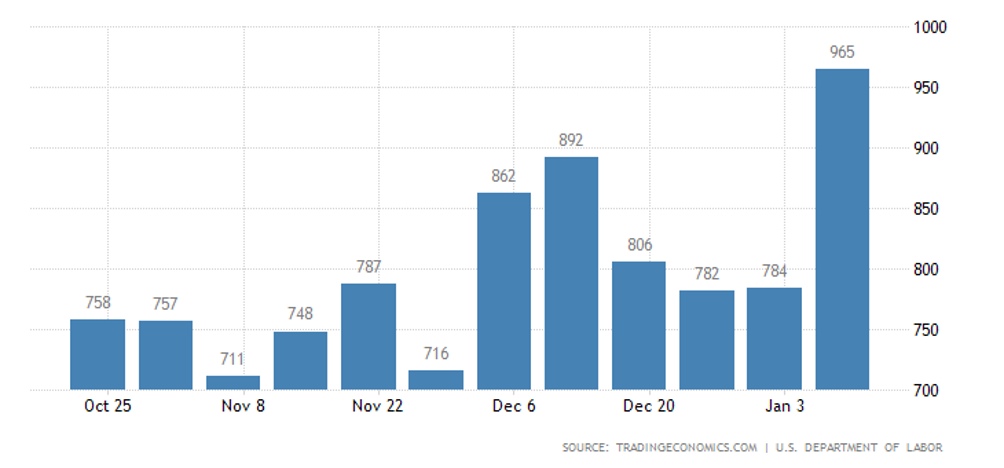

US initial jobless claims at their peak since summer:

Of course, spring peaks are far away – but, in theory, we got a cumulative downturn in a few years in the spring. And now, natural structural decline has begun. So lets see how this plays out.

The retail trade in Indonesia is the weakest in five months and the spring lows are near:

In Italy, sales -6,9% per month and -8,1% per year are the worst since spring.

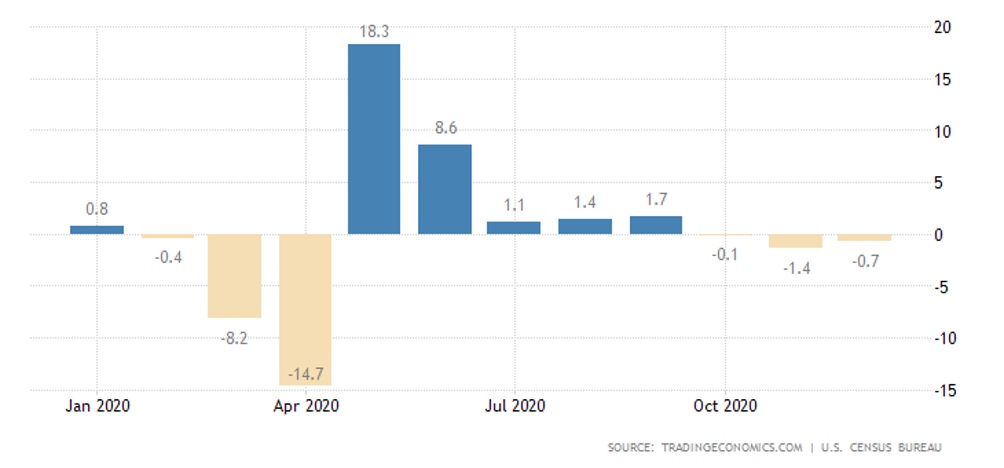

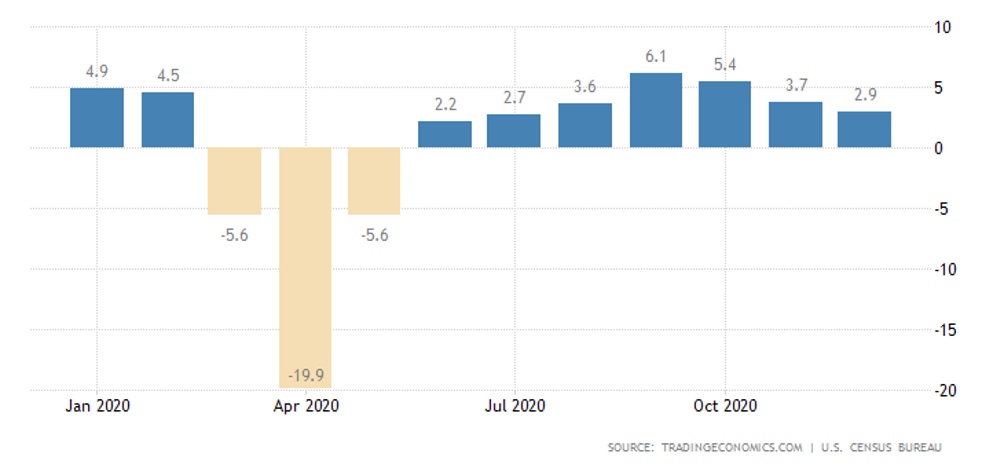

In the U.S., retail sales are in the red for the third month in a row:

Annual growth lowest in 5 months (2,9%):

The Central Bank of South Korea has left monetary policy unchanged.

Summary: The crisis continues unabated, and nothing suggests an end to it. True, in the EU strict quarantine measures, but unlike in the autumn, there is no such pressure on trade, so putting the blame on the epidemic is not enough. At the same time, due to huge support measures, capitalization of companies grows and sales are difficult for them.

In this situation, there is bound to be a sharp increase in competition, primarily between countries. In fact, all of this was fully demonstrated to us by China. But in the future, the situation will only worsen, and, moreover, as the middle class erodes, so will the structure of demand. In particular, demand for cheap products will increase and fall on expensive and high-quality products. Something similar happened in the fall of 2008, when all segments of the restaurant business were in recession, except for the lowest, like Mcdonalds.

The modern economy is not adapted to this, because the cost of innovation is an important part of capitalization. This means that the stock market downturn will be accompanied by a change in the capitalization methodology. This will make the financial sector of the world economy much more complex. In particular, the methodology of the investment process will have to be radically revised.