Period: 27 February – 5 March 2021

Top news story: In addition to macroeconomics, there is also consumer psychology. And the state of consumer psychology is just as important as the state of the economy. Because consumer panic can both bring down the most resilient market and save the most volatile market from the seemingly imminent collapse. At least for a while.

Here, too, it is a matter of principle that American consumers (and that is where the most important speculative markets for the world financial system are located) are still more optimistic:

In fact, US stock market participants are actively raising their debt. And that shows that the understanding of the seriousness of the economic situation is still rather weak. Each can deduce independently, from the fact that the collapse is still far away (the blue curve has not yet reached a peak) to the fact that the decline will be much stronger than in previous cases. It is also true that economic agents oriented towards the old pre-crisis model can still find customers relatively easily.

Macroeconomics

Italy’s GDP returned to negative in the 4th quarter (-1,9% per quarter), so the annual recession rose from -5,2% to -6,6%.

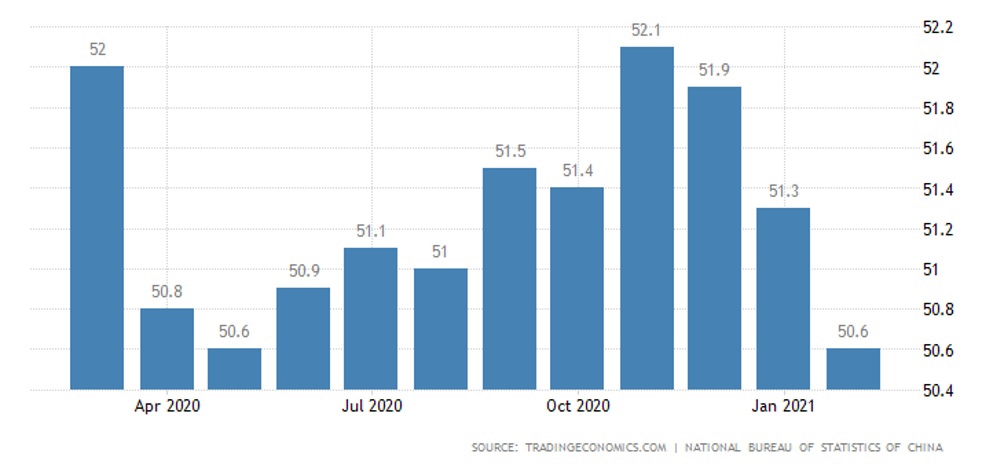

According to the official version, the PMI of the Chinese industry (recall, this is an index reflecting the opinion of experts on the situation in the industry) in February dropped to an annual trough:

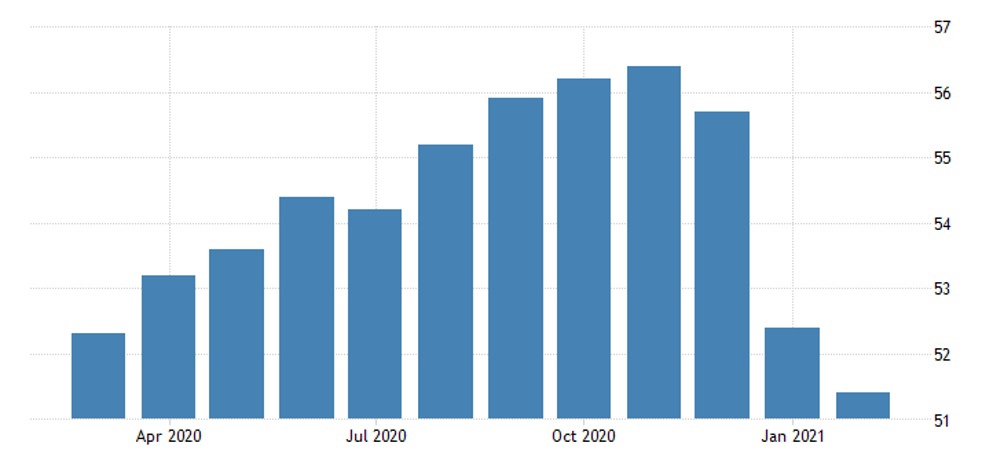

The same is true for the non-manufacturing sectors:

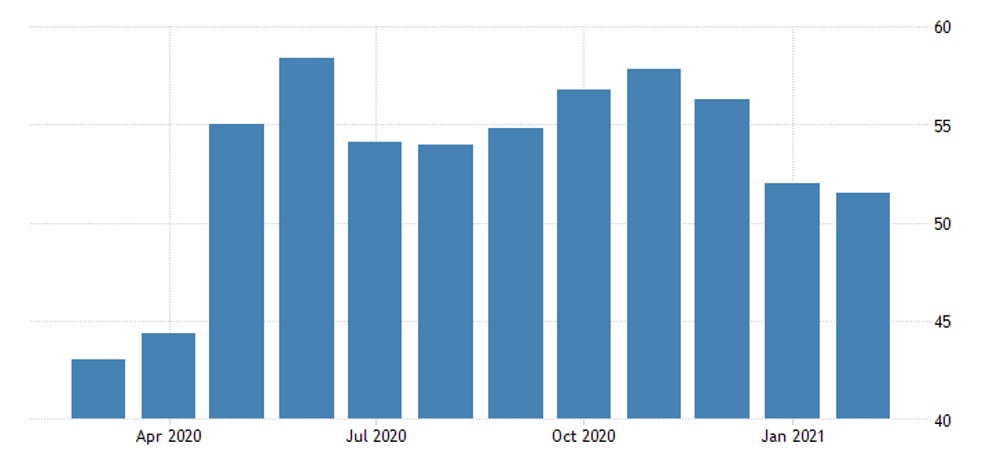

Private research yields a similar result, a 10-month minimum for all industries:

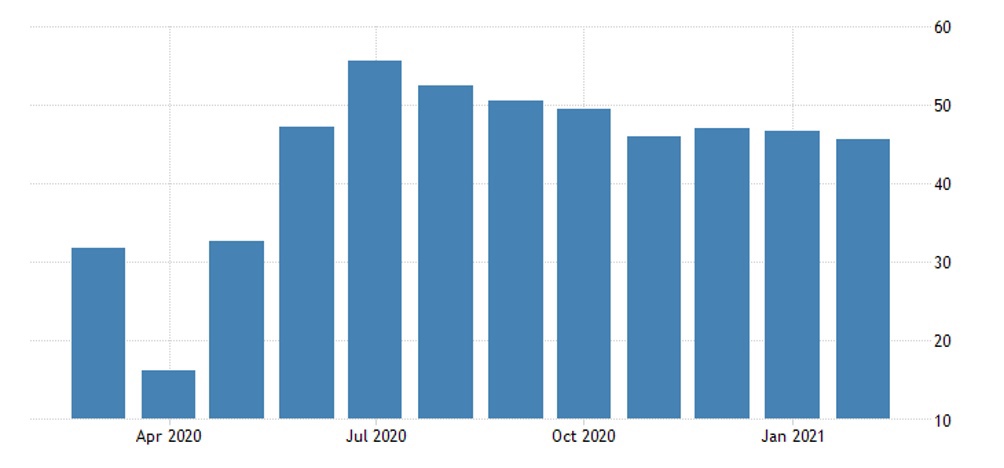

Germany has the lowest PMI for services since June 2020:

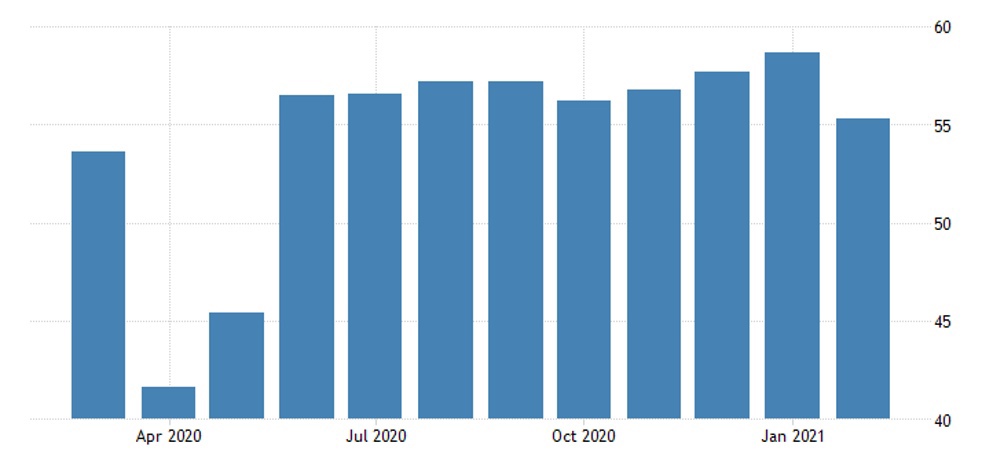

In the United States, the PMI service industry has been minimal since May 2020, but is firmly anchored in the expansion zone:

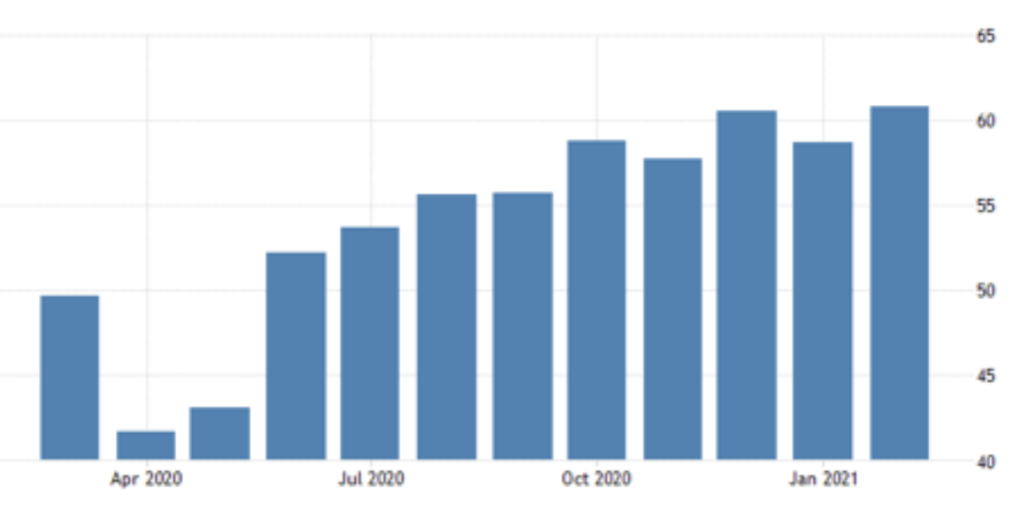

In the US, industry PMI is at a 3-year high, but entry prices are growing at their worst rate since July 2008:

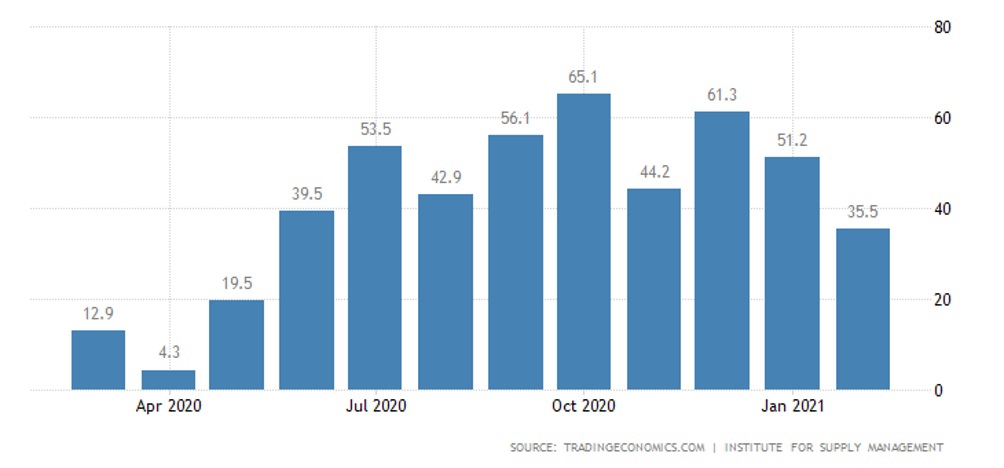

PMI in New York fell to its lowest since May 2020:

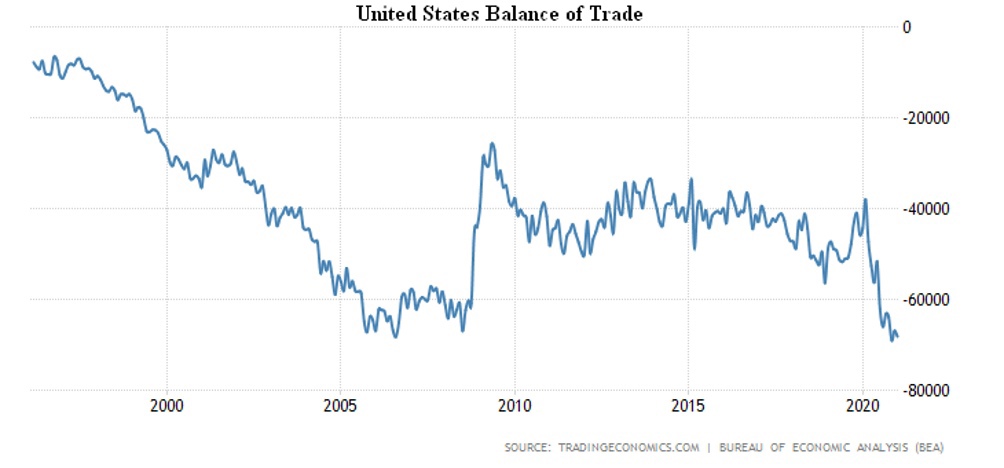

The US trade deficit in January is just a little less than the record high of November:

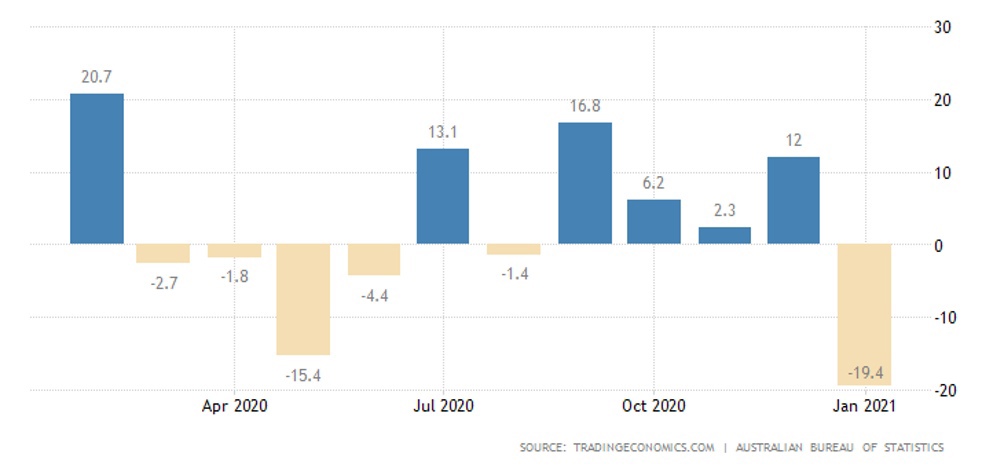

Australia dwelling approvals slumped by 19,4% per month in January (3-year trough), net of housing -39,5% to the lowest since 2012:

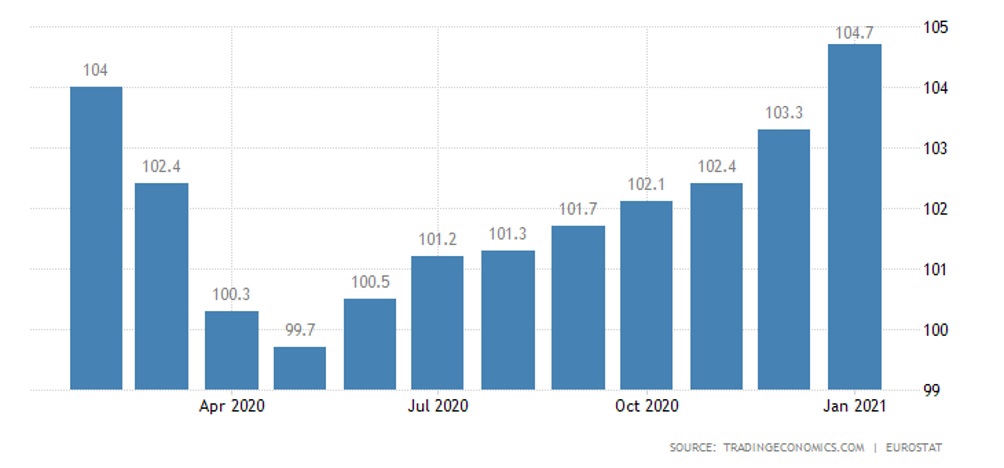

The PPI (Producer Price Index) of the Euro Area surged 1,4% per month in January – a record since January 2006:

Annual performance became zero after one and a half years of negative values:

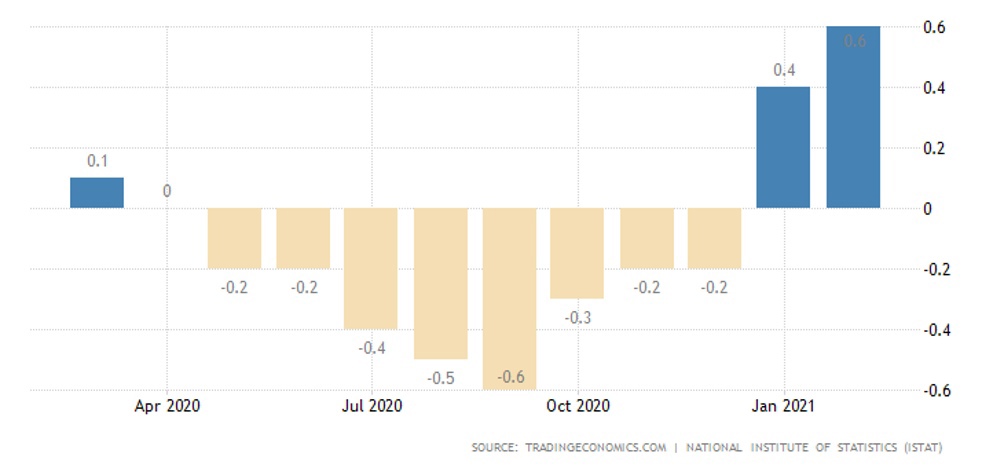

CPI (Consumer Price Index) in Italy in February is the highest since June 2019:

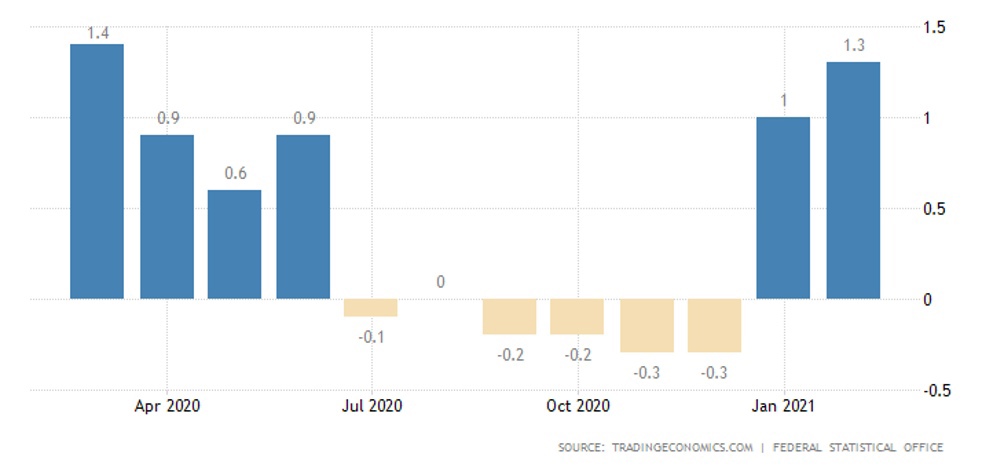

In Germany, the annual peak is:

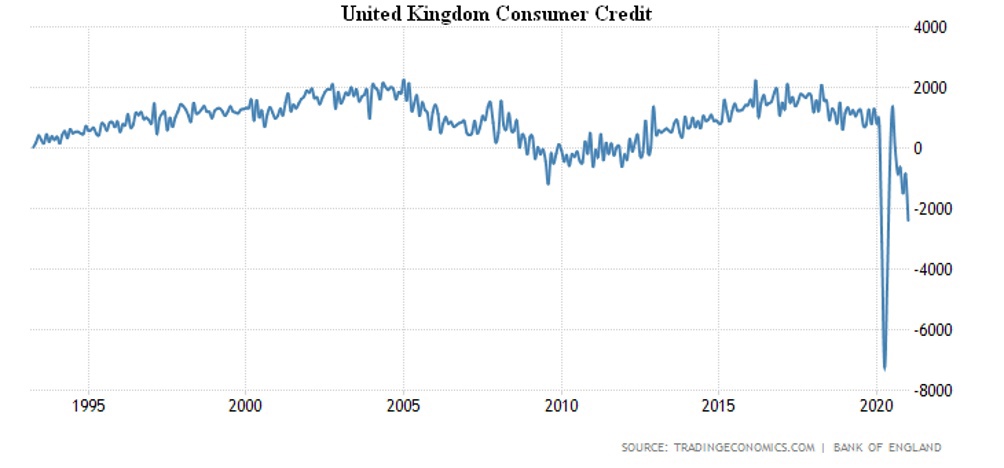

UK consumer credit has been declining at its worst rate since May 2020:

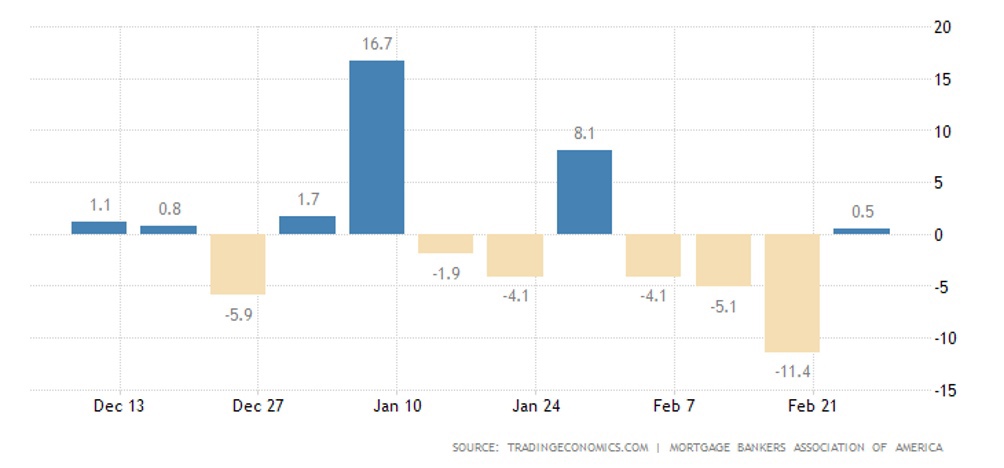

The US mortgage at the end of February was almost unable to recover from the downturns of the previous weeks:

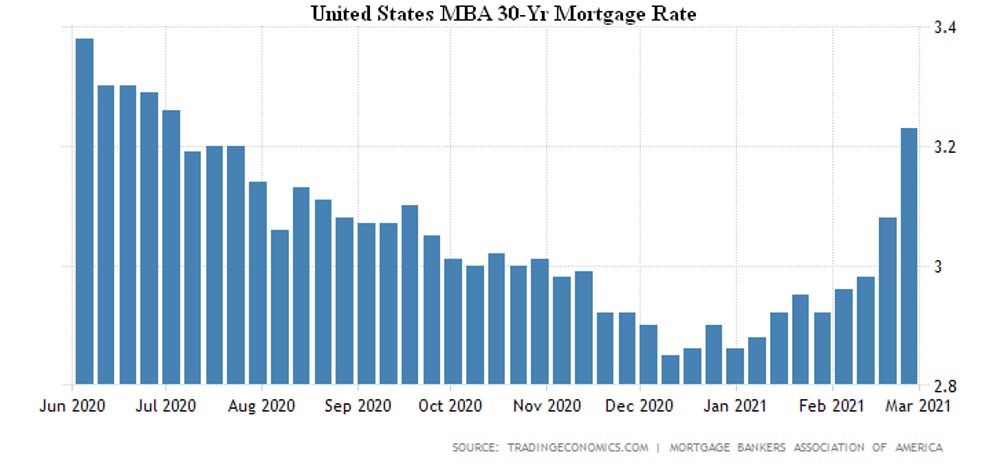

Because the 30-year mortgage rate surged to an 8-month peak of 3,23%:

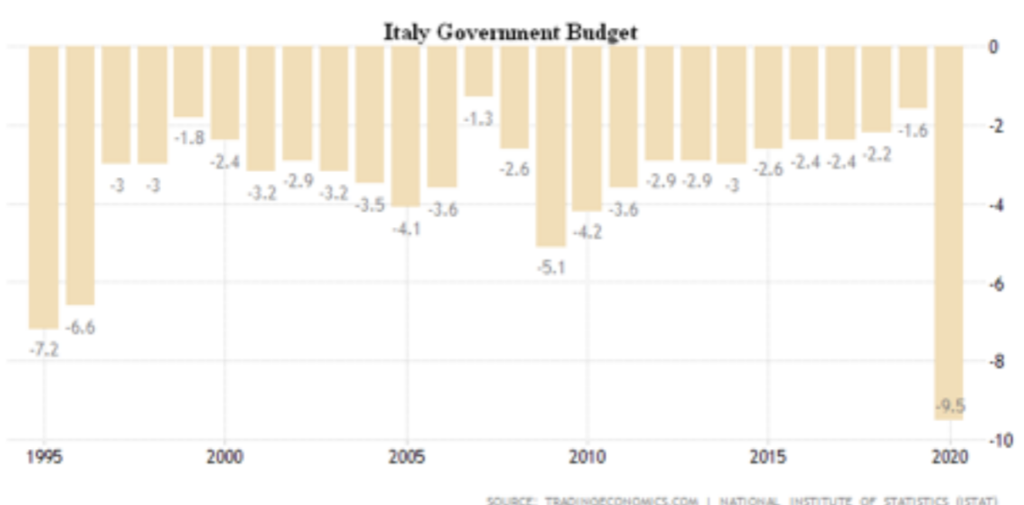

Italy’s Government budget deficit is the worst in all 26 years of observation (9,5% of GDP). Unlike the United States and the United Kingdom, Italy does not have a national currency, so the stimulus comes only from rising budget deficits:

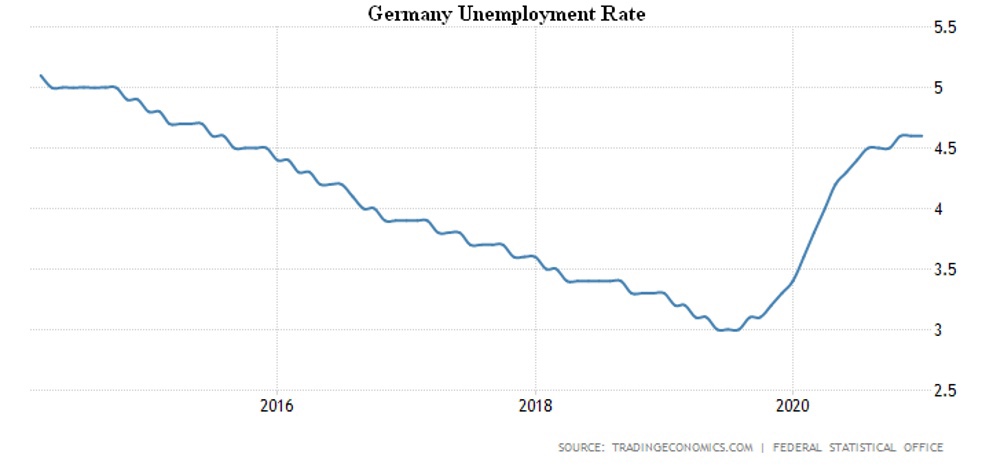

Unemployment in Germany remains at its highest in nearly six years:

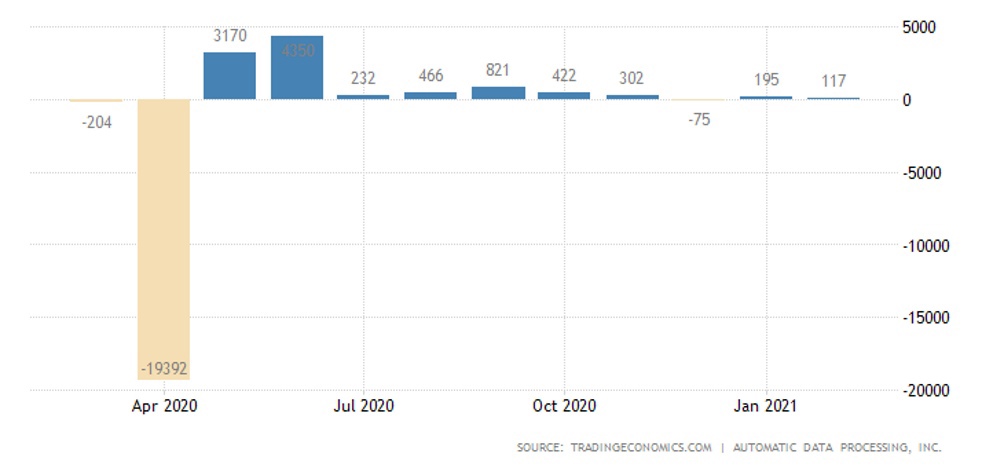

Private sector employment in the US is still quite low:

Retail trade in Germany slumped by 4,5% a month in January after -9,1% in December, making the annual decline the worst (-8,7%):

In France, the situation is not so sad, but also bad: -9,9% per month and -4,4% per year.

The same picture is in Italy: -3.0% per month and -6.8% per year.

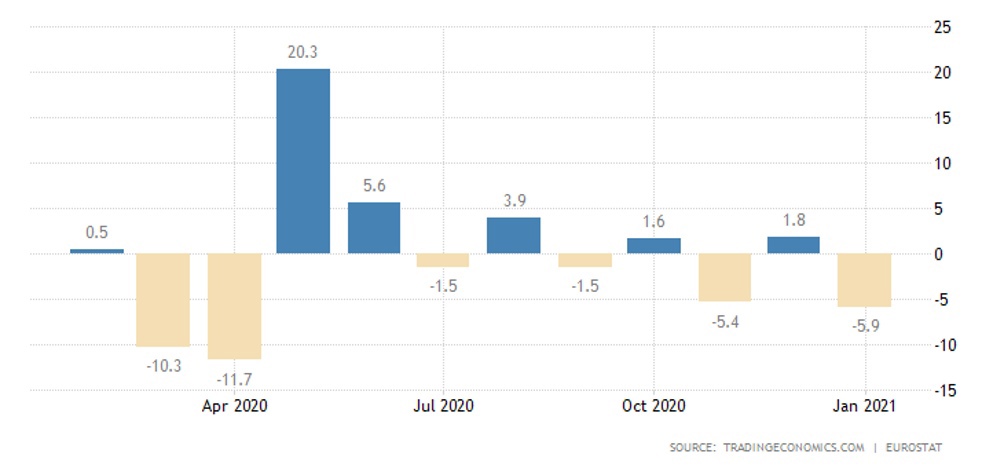

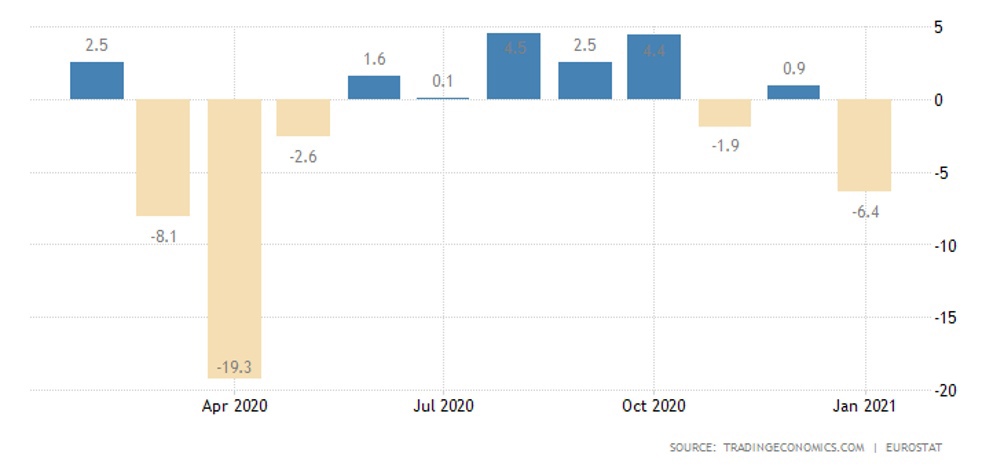

In the Euro Area as a whole, the situation is similar: -5.9% per month:

And -6,4% per year:

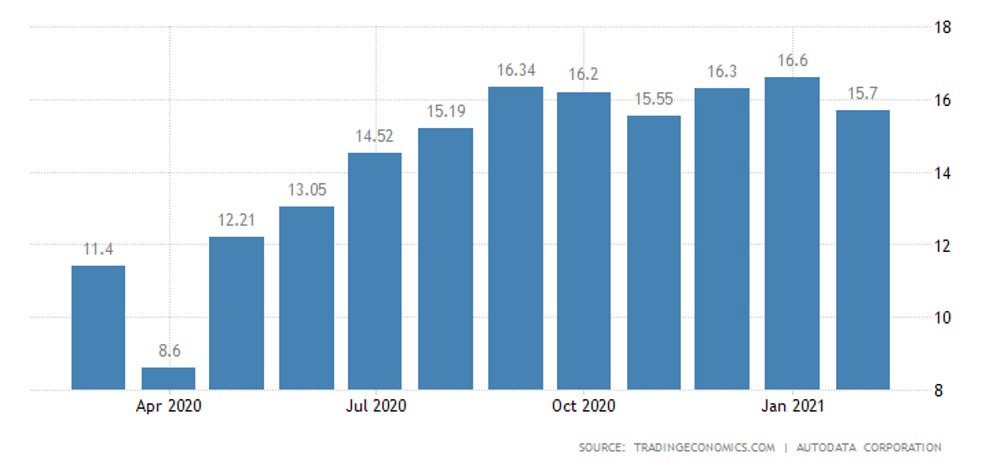

Car sales in the United States in February are the lowest in six months:

The Central Bank of Australia left rates in place, promises to buy a lot government bonds to keep market interest from rising.

Summary: Virtually all price indicators point to the beginning of inflationary processes in the world economy. Also, not only peripheral countries (like Turkey, see previous reviews) are already involved. The US is the exception, but it is also possible that satisfactory ISM figures are associated with under real inflation (and therefore with virtual sales growth). But, as it is clear, stimulus measures do not stop, why it is necessary to expect a substantial increase in inflationary processes. And, as a consequence, the actual decline in the real standard of living of the population in virtually all countries of the world.

This was to be expected and, judging by the fact that similar processes are under way throughout the world, the process has begun. Perhaps it was the failure of speculative markets to grow, so that their efficiency in sterilizing excess liquidity has fallen significantly. If nothing happens out of the ordinary, the process will only gain speed.

And that’s with the record activity of private investors in the US stock market! What happens when this optimism starts to wane? Indeed, against the backdrop of the inevitable adjustments of the speculative markets that we wrote about last week, this is almost inevitable. Accordingly, the recession may exceed general expectations, as it will be accompanied by an accelerating. And this factor could have a negative impact on the spinning of the flywheel referred to in the previous review.

In future reviews, we will follow the trend closely, and for the time being we wish all a good weekend and a successful work week! And to those celebrating international women’s day, we wish them a happy holiday! Women first!