Time period: 30 October – 05 November 2021

Top news story. We have two major news today. The first is the absolute failure of the G20 summit and the environmental summit that followed in Glasgow. At first glance, the news is purely political, but we recall that the very idea of bringing together the world’s 20 largest economies emerged after the 2008 crisis in order to respond to the economic policy challenges. And the Glasgow Environmental Summit was seen by its organizers as an instrument of new economic policy. As a result, Putin and Xi Jinping never arrived, R. T. Erdogan left after the G20, and even J. Biden expressed his disappointment.

Indeed, Putin’s claim that the mechanism of economic development has ceased to exist has been proven in practice: participants in both forums have been unable to come up with any real ideas for reviving growth. For the readers of our reviews, there is nothing new about this – it has been said time and again that the economic theory on which we rely excludes the possibility of restoring growth on the old basis. But if they were words before, they have now become a fact. And even more important is our (Mikhail Khazin Foundation for Economic Research) work on launching alternative models of economic development.

Well, to conclude this section, the price chart for an important resource:

Wheat prices continue to rise, which means that the crisis will be marked not only by economic but also by serious social consequences – wheat is one of the main elements of nutrition.

Macroeconomics

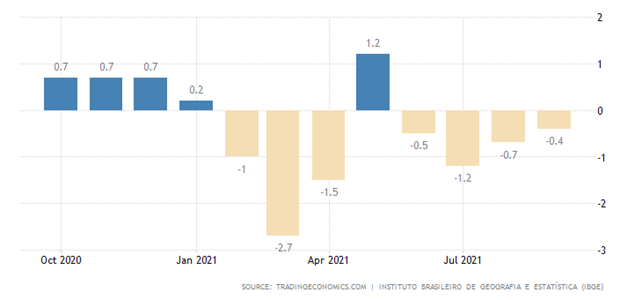

Industrial production in Brazil is -0.4% m/m, the fourth negative in a row and the seventh in the last eight months:

Why the annual performance is also in the red (-3.9%), the worst since June 2020:

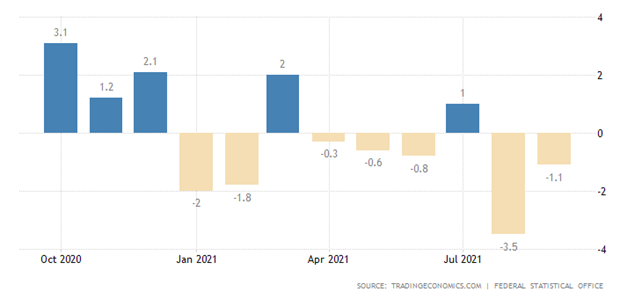

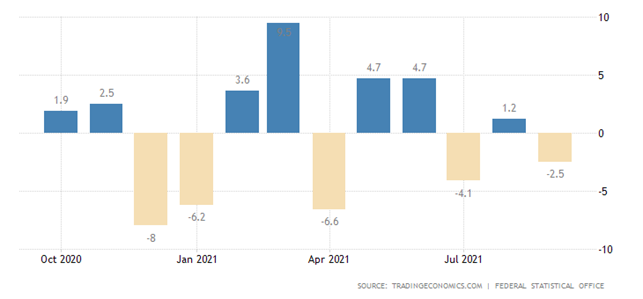

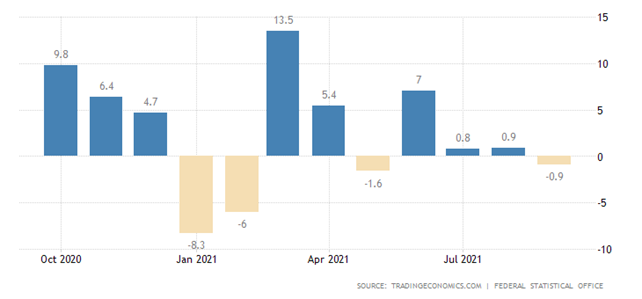

In Germany, -1.1% per month, this is the fifth minus in the last 6 months:

The annual performance is also now in the red (-1.0%), and by the pre-pandemic February 2020, it’s still -9.5%:

This means that there is no need to talk about any recovery, especially given the fact that, as always, inflation rates are underestimated.

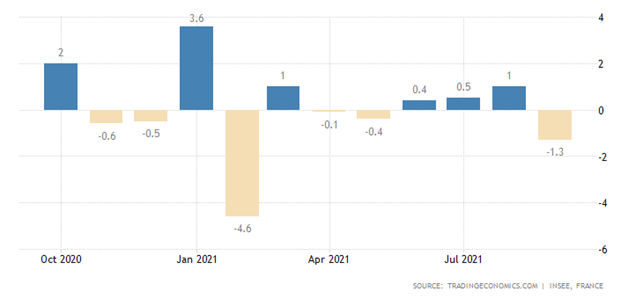

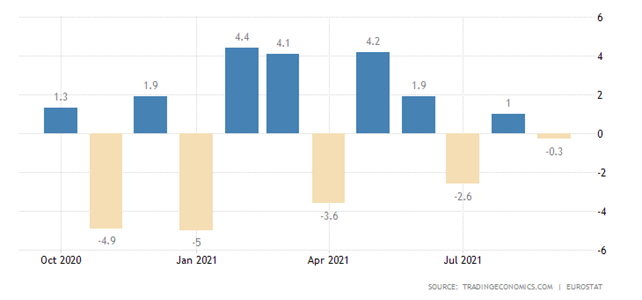

In France, there is also a monthly negative (-1.3%):

Annual growth is still here, but it is the weakest in seven months (+0.8%):

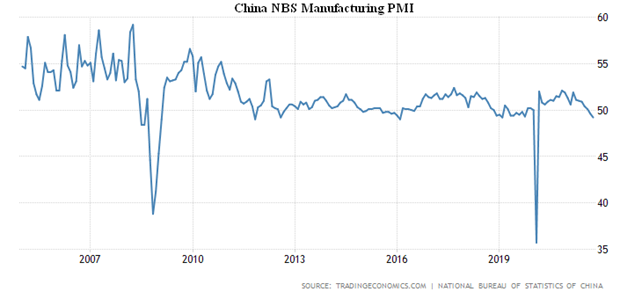

The official PMI (index of expert assessment of the state of the industry. Its value less than 50 means stagnation and recession) of the Chinese industry went into the recession zone (49.2), not counting February 2020, the lowest since 2009:

I recall that we projected this situation weeks ago.

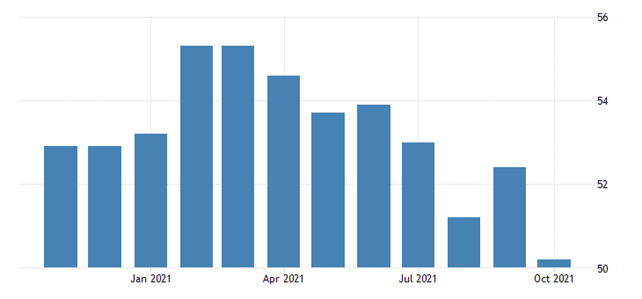

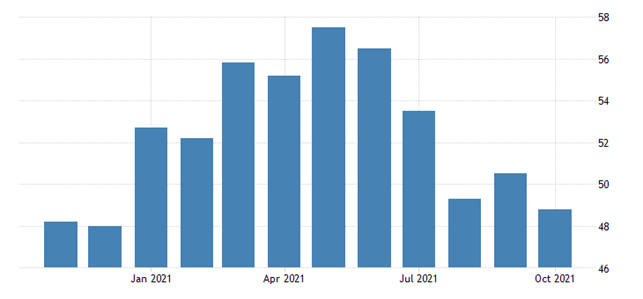

South Korea has a 13-month low (50.2):

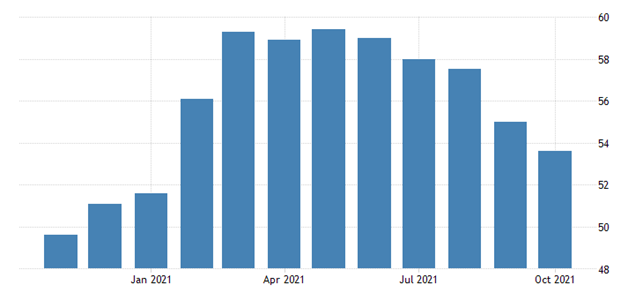

In France, the trough since January (53.6):

Here we will remind that one of the main factors of the industry is the volume of sales.

And if inflation is underestimated, then sales increase – so we can’t rule out that here, too, negative figures have already been achieved.

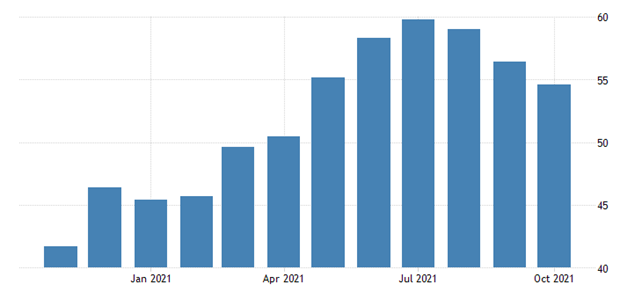

PMI of the Russian services sector is the worst since December 2020 and is in the recession zone (48.8):

The Euro Area has a semi-annual low (54.6) against the backdrop of record inflation for 21 years of observation:

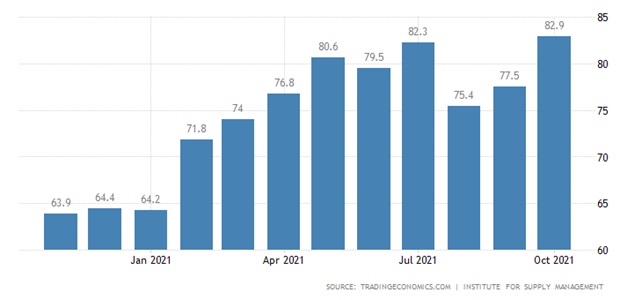

But the United States has a record high, but prices have been at the top since 2005:

Of course, all of the above about inflation applies to the US. Even to a greater extent, this applies specifically to the United States, since there the difference between real indicators of inflation and official ones is especially significant.

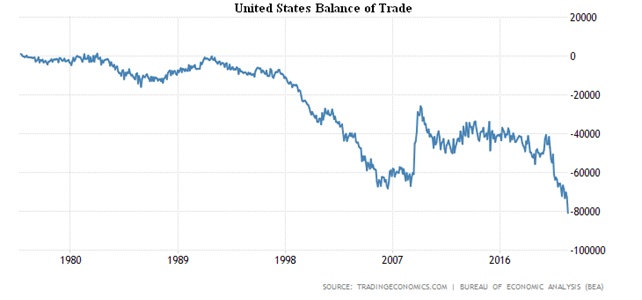

The US trade deficit has renewed the record high, which is also a proxy for high prices:

Against the backdrop of another historical peak in imports:

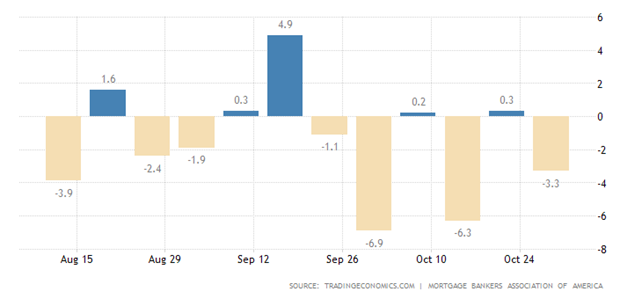

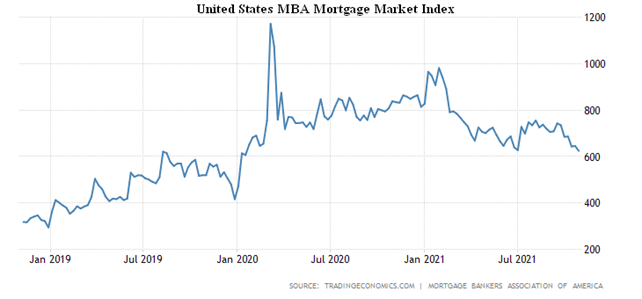

Mortgage applications in the US are falling again:

Their number is the smallest since the beginning of 2020:

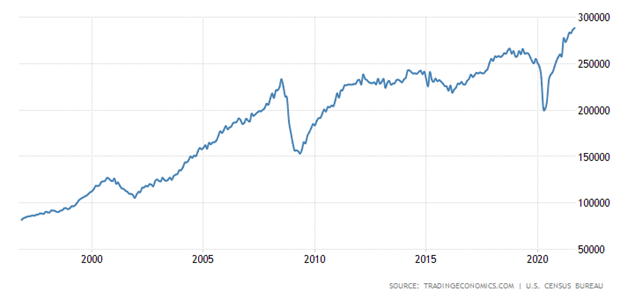

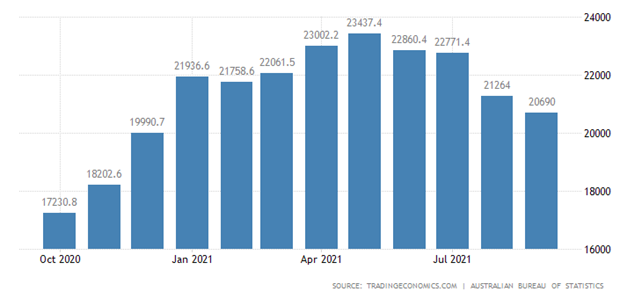

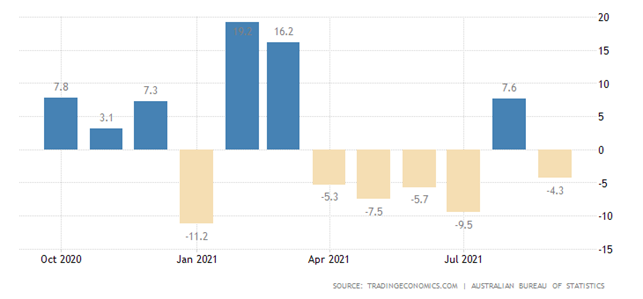

Home loans in Australia have been decreasing for 4 months in a row:

Dwelling approvals in Australia, after a brief respite, have again gone into a month-to-month negative:

And, for months now, inflation rates around the world are breaking new records. CPI (Consumer Price Index) of Switzerland 1.2% per year – top repetition since 2010:

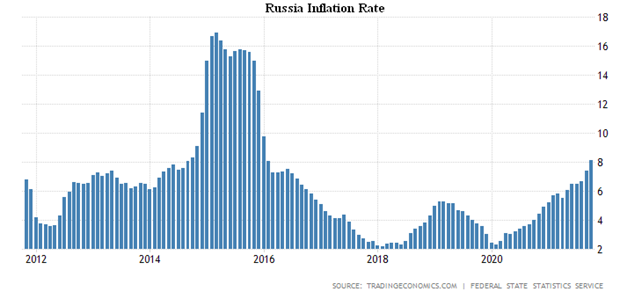

CPI of Russia +8.1% YoY, the highest since January 2016:

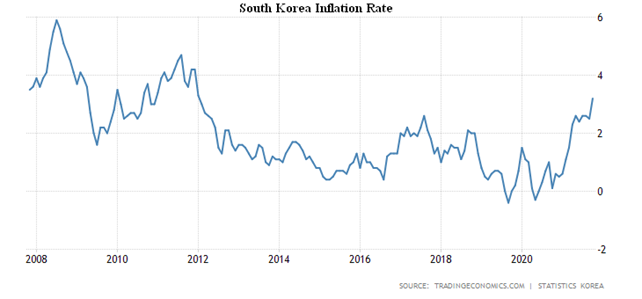

CPI of South Korea +3.2% per year, maximum since 2012:

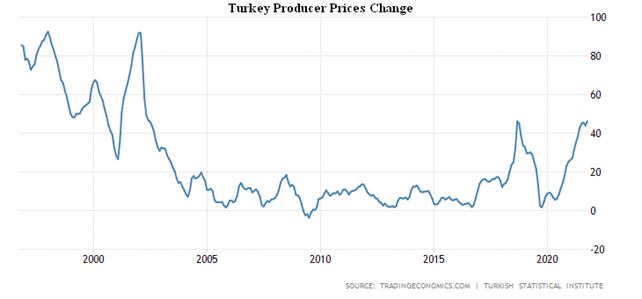

PPI (Producer Price Index) Turkey broke through the top of 2018 and peaks in almost 20 years (+46.3% per year):

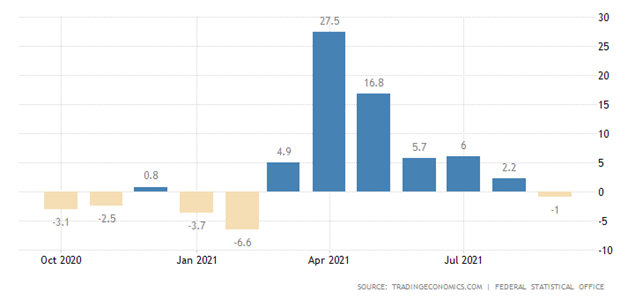

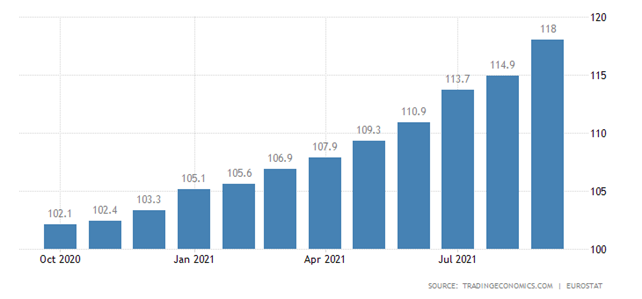

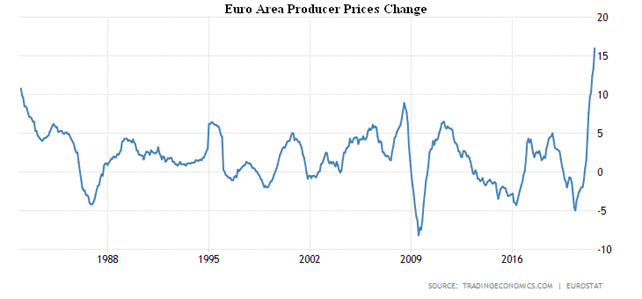

The Euro Area PPI + 2.7% m/m, a record for 27 years of observation:

And +16.0% per year is also a record, but for 40 years of conducting the survey:

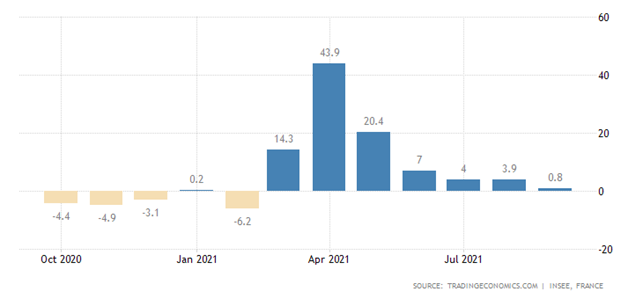

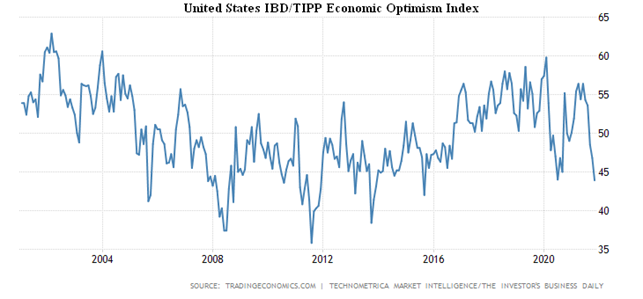

Economic optimism in the United States from IBD/TIPP has broken through the coronavirus trough of 2020 and slipped to the lowest since 2015 (43.9):

Retail sales in Germany -2.5% per month:

and -0.9% per year:

In the Euro Area as a whole, there is also a monthly decline in retail sales:

The U.S. Federal Reserve began to reduce its asset purchases by $15 billion a month; at that rate, the QE would end by mid-2022. The Bank of England is keeping things as they are, but promises to hike the rates soon, with part of the board already voting for tightening.

The Central Bank of Australia abandoned the policy, withdrew its promise not to raise rates until 2024.

Summary. A year ago, everyone felt that the pandemic menace was over and the economic recovery began. The real results, for example, of the German industry (see the previous section) show that no recovery has taken place. Moreover, the downturn has reached a new level. This is the normal situation in a structural crisis, so it is safe to say that when the new recession is over, recovery growth (and it always is) will be limited and will not win back. In other words, the graph of the world economy is beginning to look like a downward staircase. The details, duration and scope of the recession as a result of this process should be found in Mikhail Khazin’s book “Reminiscences about the Future”.

Estimates of economic optimism in the US are also not very correlated with official growth figures imposed. Statistics are complicated, too. Thus, in the U.S. a lot of jobs were created last week (571,000 with a forecast of 400,000), but data from previous weeks (523,000 with an initial estimate of 568,000) show that these data can be significantly revised downwards. In other words, assessing the economic situation on the basis of official data is becoming increasingly problematic, making our work much more difficult. Nevertheless, we try to provide our readers as adequate a picture as possible of what is happening, given our understanding of real economic processes.

We wish our readers a productive and quiet work week!