Period: 3 – 9 October 2020

Top news story: Given the incredible political instability (from Donald Trump’s disease to the conflict in Armenia and Azerbaijan), it is difficult to identify the main economic events. However, the cause of political instability lies in the economy, and for that reason, important economic news is certainly breaking through.

In particular, this week’s Goldman Sachs warns of the risks of a significant downturn in the stock market in the run-up to the US presidential election.

Goldman Sachs senior investment strategist Abby Joseph Cohen warns: due to political and economic uncertainty, there may be risks of increased volatility and a substantial decline in the stock market in the run-up to the US President’s election.

Aside from the specifics, this warning will actually legalize the stock market collapse before the election. And if in addition to this another discussion between Democrats and Republicans about the scale of the necessary support for the economy (and we are talking about trillions of dollars), it becomes clear that until the relative destruction of the «status quo» is left not months, but weeks.

As a matter of fact, some gold experts are already saying that hyperinflation may soon bring the value of gold to $20,000 per troy ounce.

This is fully in line with the strategy scenario described in our 2003 book «Sunset dollar empire and the end of the «Pax Americana», but recently, this scenario was still being postponed. As we can see, the situation is changing rapidly.

In general, it seems that the background of the news is no longer just about describing economic reality, but about trying to offer some alternatives to the long-term mainstream scenario.

Macroeconomics

Britain’s GDP recovery slowed: in August, 2,1% per month and -9,3% per year.

Industrial production in Germany suddenly turned negative in August at 0,2% per month.

From this, the annual decline almost did not decrease (-9,6%):

In Spain, output grew by only 0,4% per month, and the annual decline narrowed (-5,7%). In Britain, industry output is 0,3% per month and -6,4% per year.

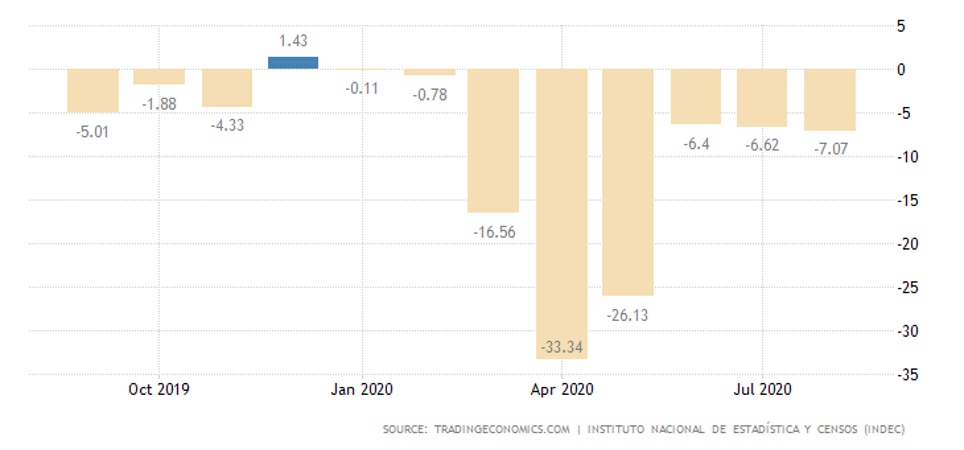

In Argentina, the annual decline has been increasing for two consecutive months:

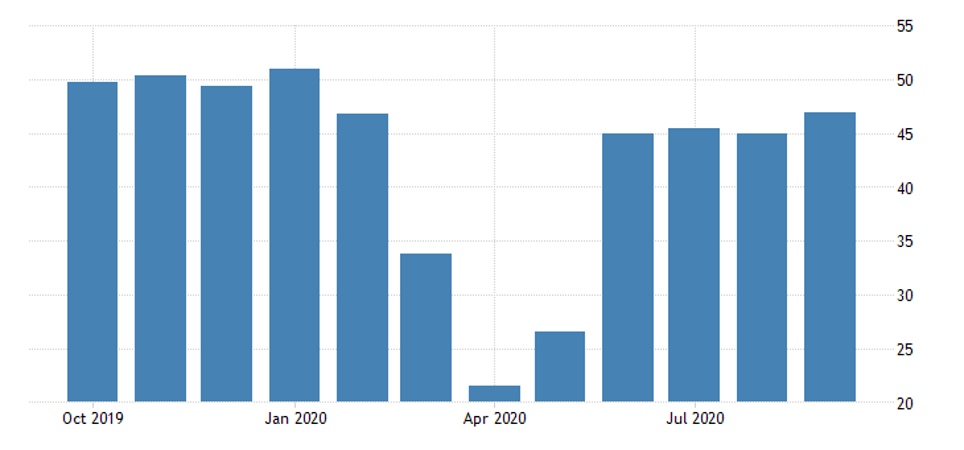

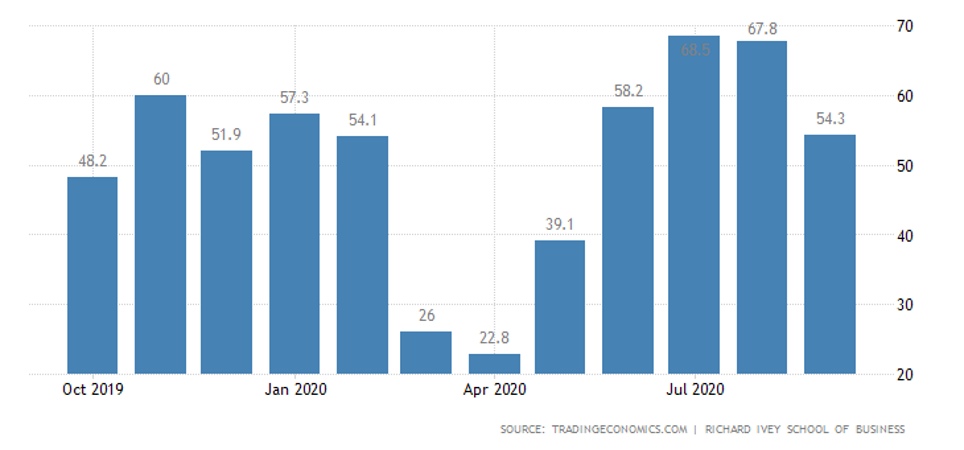

Japan’s PMI Service Index continues to recover slowly but is still in recession:

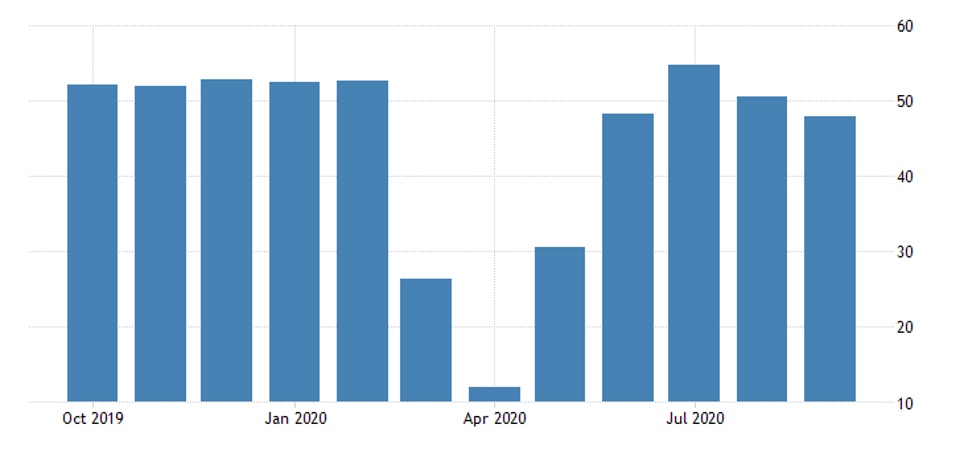

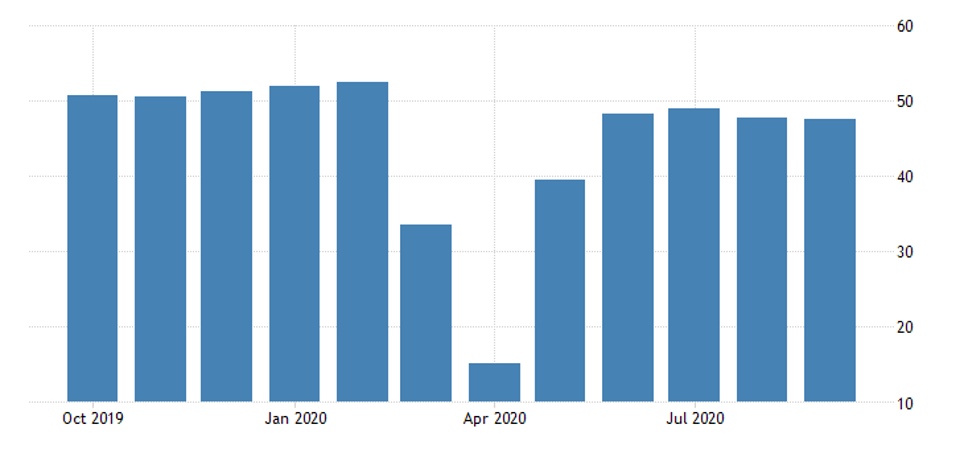

The rest suffered a setback in September, with The Euro Area falling below 50 points:

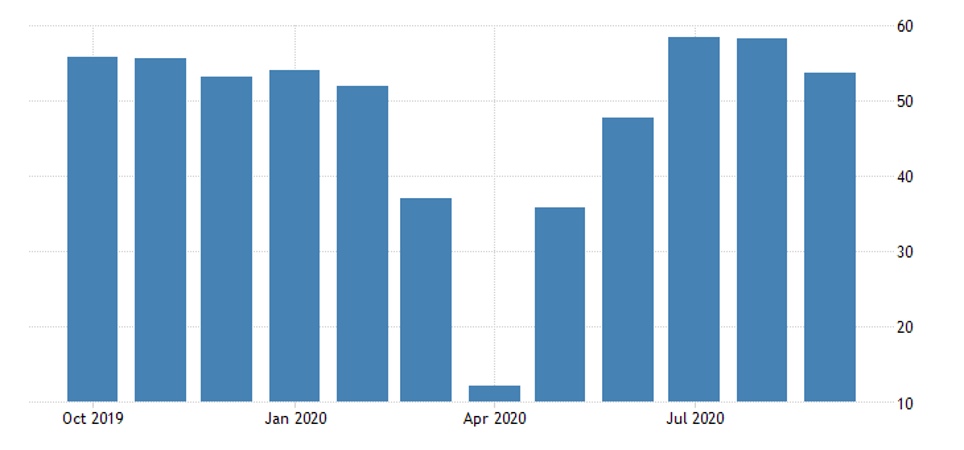

Britain remained above 50, as did the United States:

And Russia, although there is a significant decline:

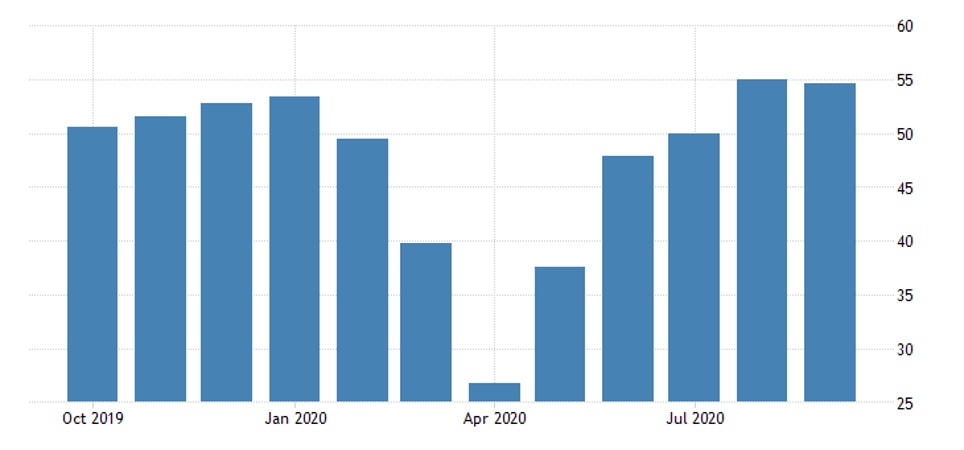

The Euro Area’s construction sector’s PMI remains in recession because of Germany’s and France’s problems:

Canada’s overall economic PMI has suddenly weakened to a four-month low:

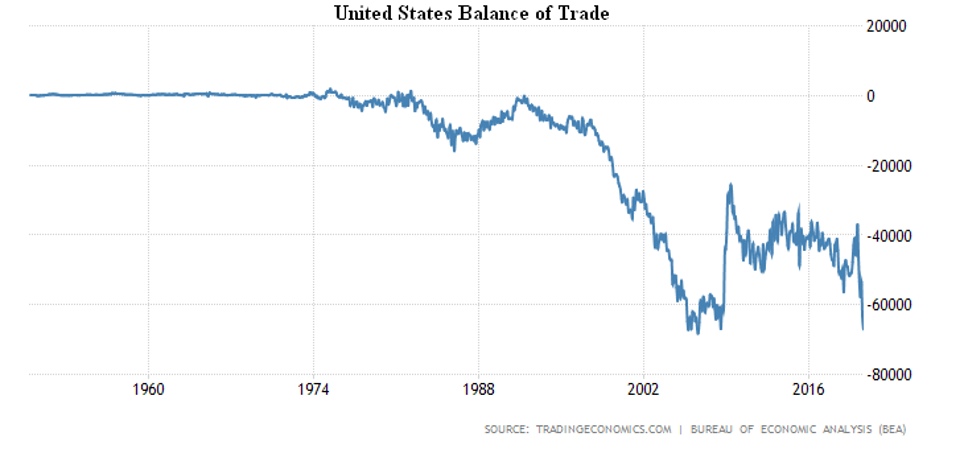

The US trade deficit in August is the worst in 14 years and close to its historic peak: imports recovered, exports did not:

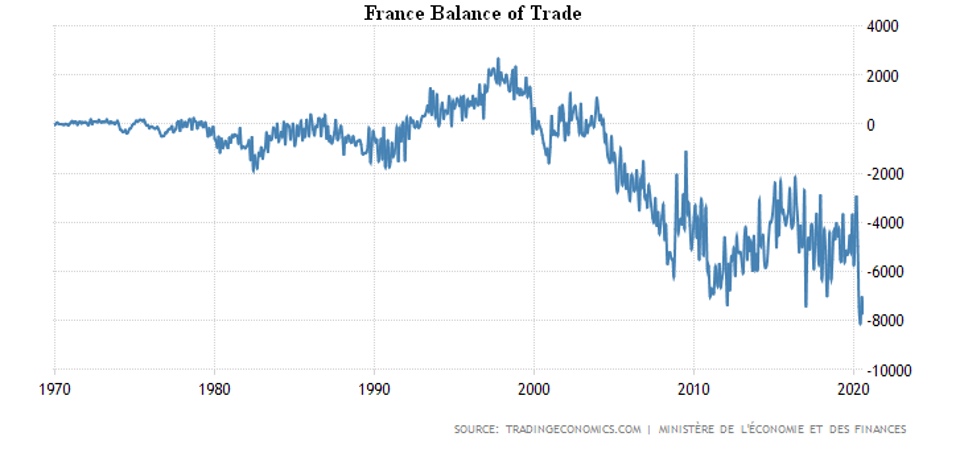

A similar story in France:

And Britain’s deficit is growing.

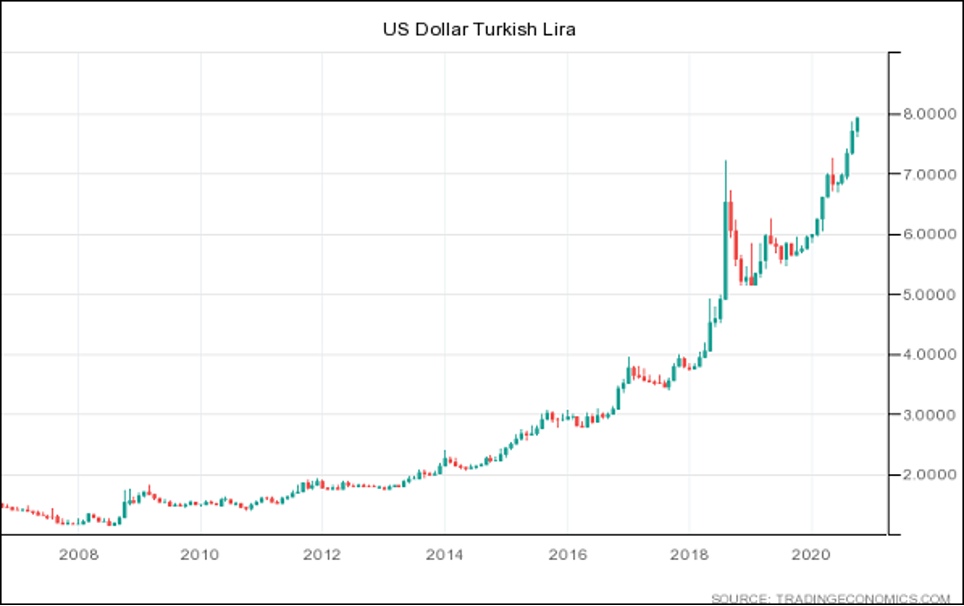

Turkey’s PPI at a 14-month peak, the CPI is also high. The reason for this is, among other things, the continued fall of the Turkish Lira:

Spanish market sentiment is deteriorating for three consecutive months.

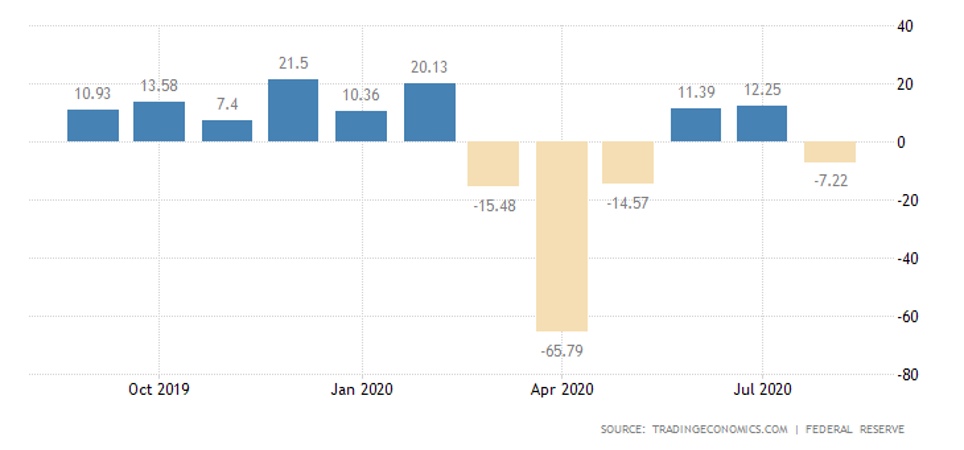

Consumer credit in the United States suddenly went into decline in August (especially weak credit cards):

Japanese salaries fell 1,3% per year nominally and 1,4% in reality. And their spending is much lower: -6,9% per year in August; a month-long increase of 1,7% did not offset the fall of July (-6,7%).

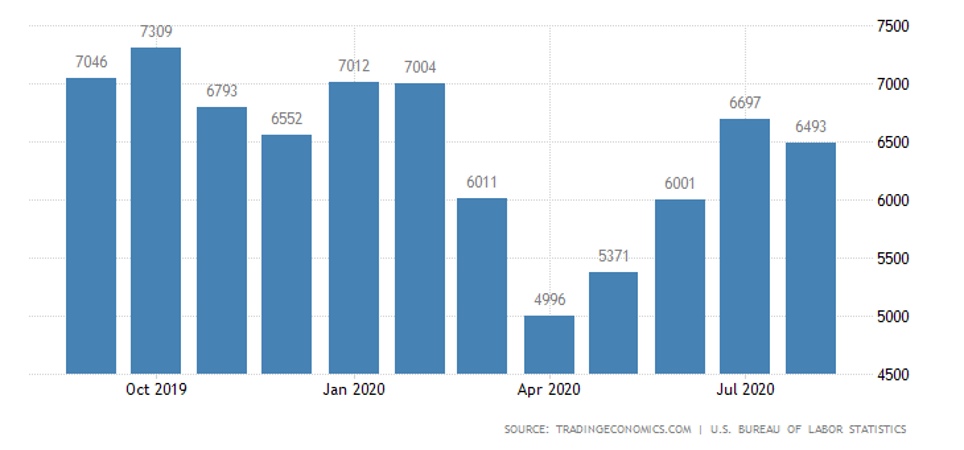

The number of vacancies in the United States decreased unexpectedly in August:

Claims for unemployment benefits are declining very slowly and are still higher than the 2009 peak:

The Central Bank of Australia and the Central Bank of India maintained the rates unchanged.

The ECB protocol has shown a willingness to increase monetary stimulus in any way.

The FED’s protocol notes «uncertainty» and requires fiscal stimulus in addition to monetary stimulus.

Summary. Given the scale of the monetary stimulus of recent months (and in the summer all possible records have been broken and even after some decline of the monetary authorities’ activity the amounts of injections are still higher than all previous years), it is not possible to talk about some «recovery» of. If emissions are excluded (which no one is going to do), it should be a colossal decline, not nominal growth. However, even this nominal growth does not occur.

So, the question is not so much whether there will be a collapse, but rather when it will begin. Indeed, it is the headline news that people are already beginning to prepare for a potential collapse. We believe that the collapse will continue for a long time, because the structural crisis has already begun and will be protracted (GDP for the major developed countries will fall at a rate of 10 per cent of GDP per year and will have to fall at least twice). In full accord with economic theory.